My working hypothesis is that the US economy cant take real rates above the regression channel and that the average (or fair value) of 5 year real rates is around -1% (150bps lower) due to debt and demographics. 1/

5 year breakevens look like they have topped out and a break of 250bps will lead to mean reverse back to 150bps maybe (I understand and take on board the complexity of de-globalisation and tight commodity markets).

The big question is whether this pattern in yields is a potential H&S top or a correction before higher rates. The balance of probability for me is a break lower.

The two things that affect this the most are the dollar (the higher it goes the more deflationary pressure it exerts for now). There is a risk of a spike before respite... we probably need to complete the weekly DeMark 9 count first.

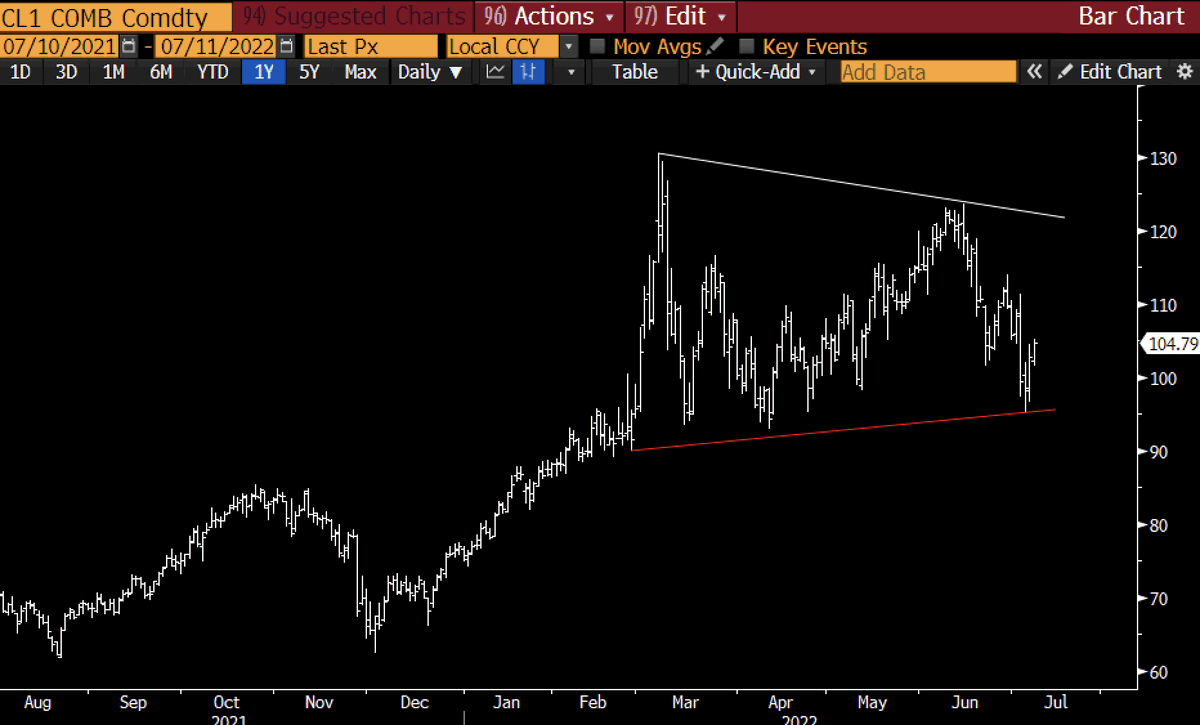

And then its oil...the range break will tell us everything and settle for the next 6 to 9 months whether demand trumps supply or supply trumps demand. This is the key battleground.

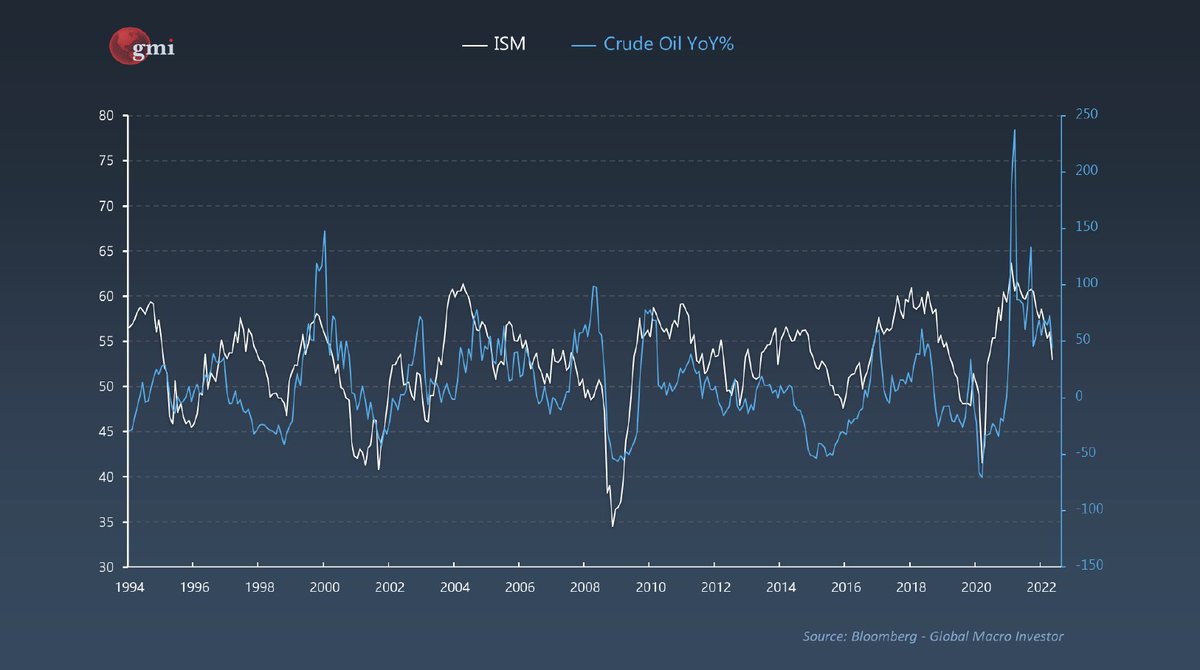

Oil is trading roughly in line with ISM as it always does...and thus should fall as ISM falls.

My forward-ISM indicator suggest that we need to brace ourselves for economic data collapsing fast in the coming months...as the tightest monetary conditions (based on rates, dollar and commodities) take hold and destroy demand.

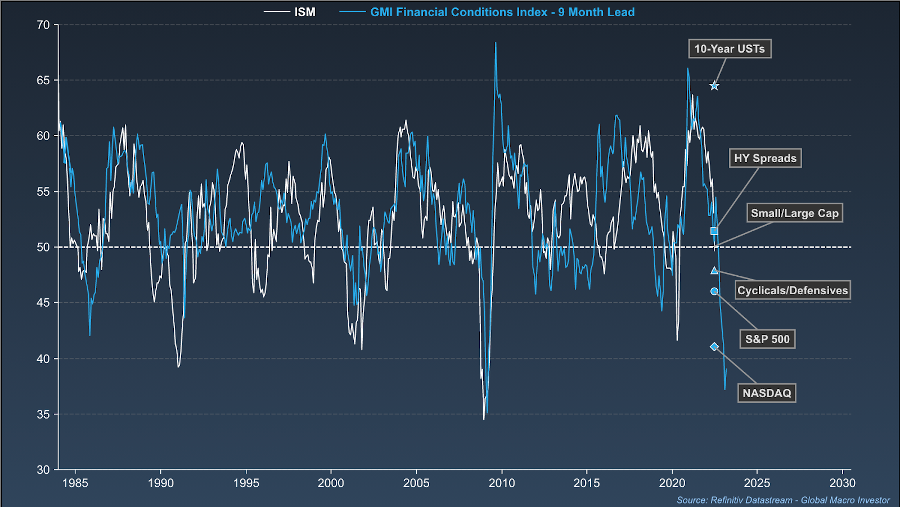

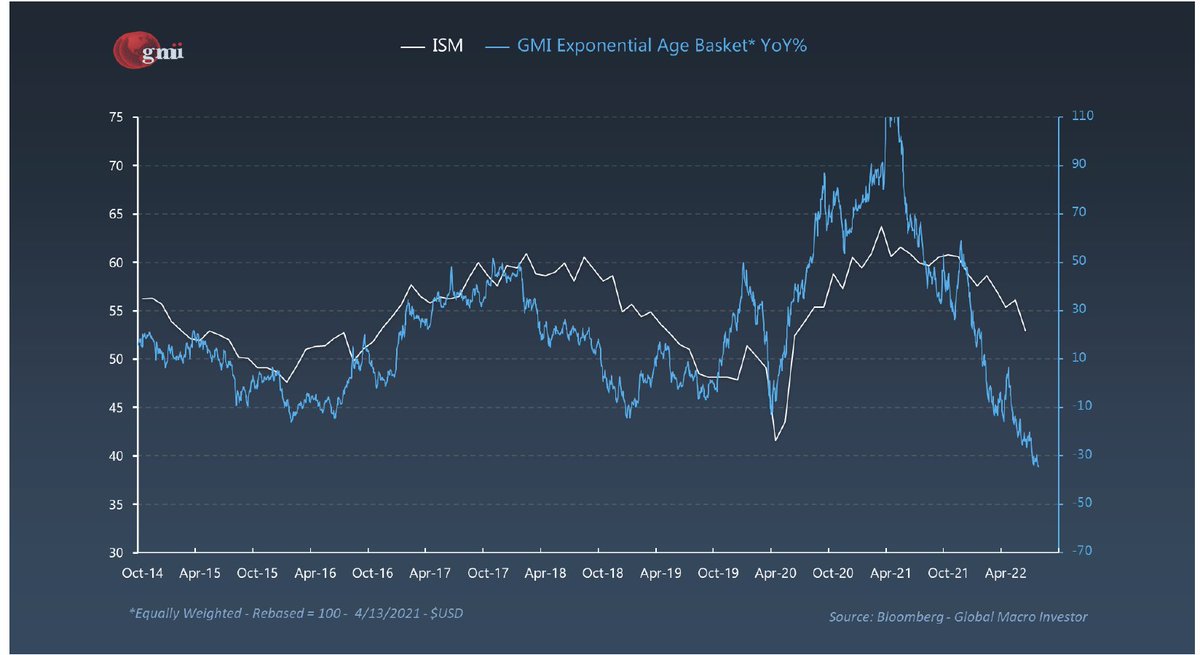

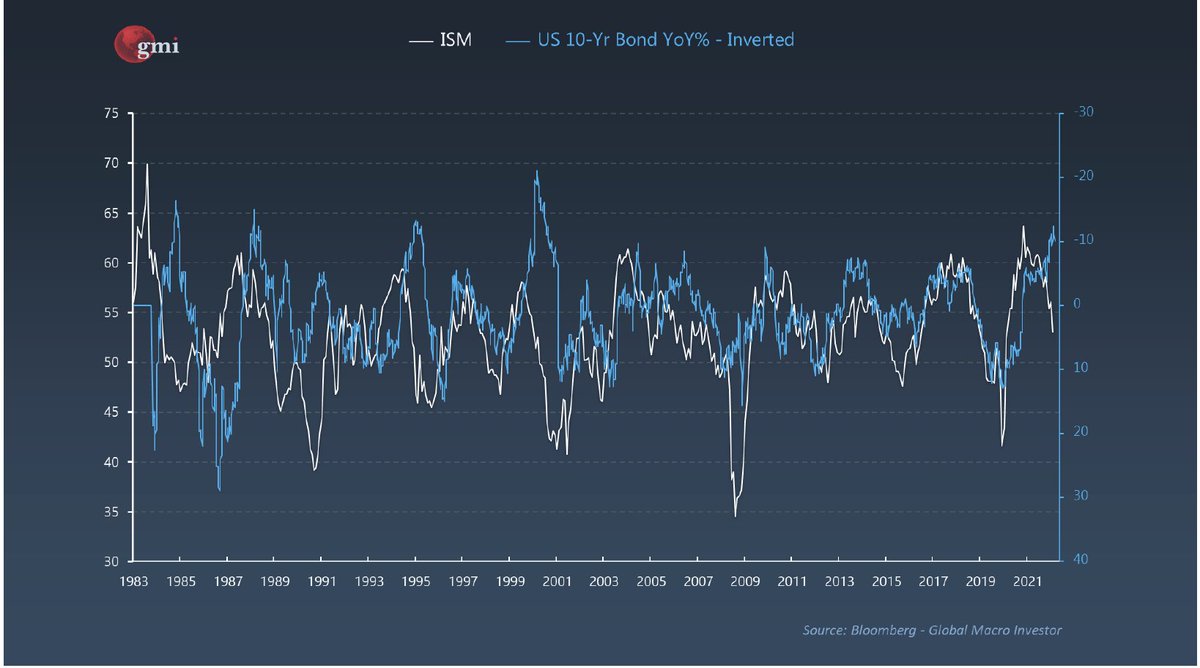

And when we plot asset prices against this, bonds are the standout (they trade above ISM) and tech is the area that has priced in most economic risk.

My basket of Exponential Age growth tech stocks and ETF's which I have start accumulating into this weakness is the most reflective of the future economic reality and thus should outperformed as yields come lower..

And bonds are diverging which it a repeat of 2000. Yields and oil collapsed eventually. We also saw a similar mismatch in 1994 and yields fell.

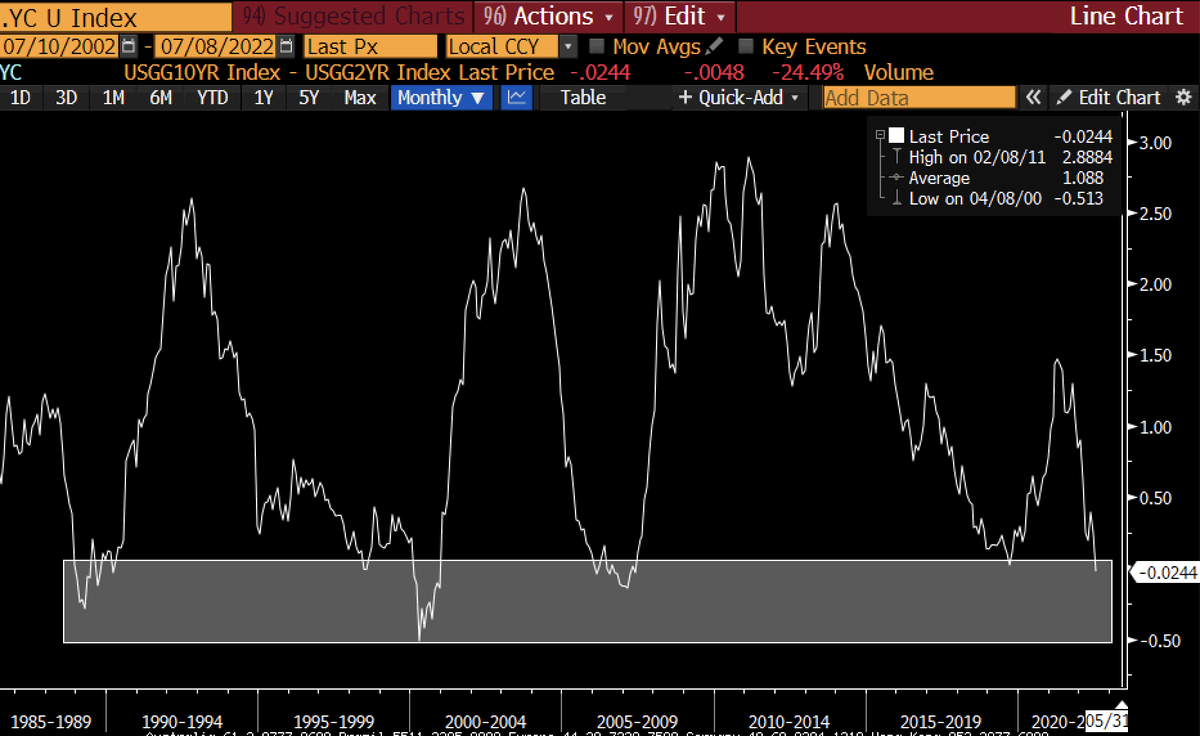

As Soros writes in his trading notes in the Alchemy of Finance, the best time to buy bonds is when the yield curve is inverted as the future expected returns are very high...

So, I like growth tech but love bonds but clearly there are always risks to this view. This is how I see the balance of probabilities. What about digital assets?

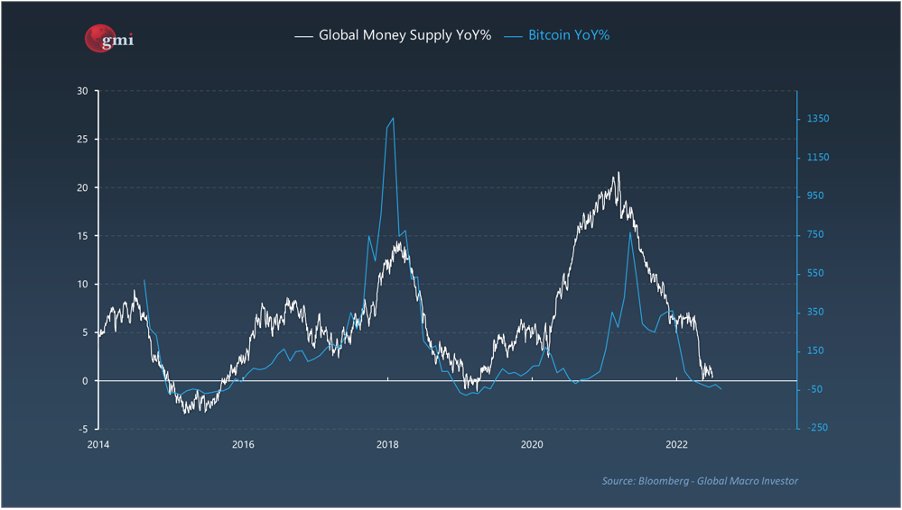

From a macro perspective, the big driver is global M2 growth.

From a macro perspective, the big driver is global M2 growth.

And that is roughly the inverse of ISM (ISM leads by 9 months). As ISM falls M2 should begin to grow.... ISM of 38, as per the model, puts M2 growth back at 13%.

The next 2 to 3 months will reveal a lot. As Stan Druckmiller says, the job of a macro investor is to buy or sell assets that are the most mispriced for the 12 to 18 months out. In the next 12 to 18 months we will have had a recession. Monetary conditions will be much weaker.

Just to be clear - I think risk assets probably go lower before reversing but not 100% sure. Yes, there is a risk of an extended recession like 2001/2 or 2008/9 but I dont really see that being the higher odds. Im still using 1947, 1974 and 2018 as my blended hypothesis

جاري تحميل الاقتراحات...