10 Money rules that can help you simplify personal finance and investing decisions.

1. Rule of 72

Helps you estimate the number of years needed to double your money at a given annual rate of return

1. Rule of 72

Helps you estimate the number of years needed to double your money at a given annual rate of return

For example if you have 10M invested, how long will it take you to double your money to 20M?

We assume a minimum required rate of return of 10% per annum

72 divided by 10 = 7.2yrs

Hence with a required rate of return of 10% per annum, it will take you 7.2yrs to double your money.

We assume a minimum required rate of return of 10% per annum

72 divided by 10 = 7.2yrs

Hence with a required rate of return of 10% per annum, it will take you 7.2yrs to double your money.

2. 4% withdrawal rule in retirement.

This rule suggests that a retiree can withdraw 4% of the balance in their retirement account or investment portfolio in the first year after retiring,

And then withdraw the same dollar amount, adjusted for inflation, every year thereafter.

This rule suggests that a retiree can withdraw 4% of the balance in their retirement account or investment portfolio in the first year after retiring,

And then withdraw the same dollar amount, adjusted for inflation, every year thereafter.

This rule helps answer the question, "How much should you withdraw from your retirement portfolio every year to never run out of money.

4% is the recommended rate in the U.S. market since that's what long term U.S bonds return per annum, hence it's easily achievable in a low risk asset.

Hence by withdrawing 4% you will be only withdrawing the returns on investment and not your capital.

4% is the recommended rate in the U.S. market since that's what long term U.S bonds return per annum, hence it's easily achievable in a low risk asset.

Hence by withdrawing 4% you will be only withdrawing the returns on investment and not your capital.

For the Kenyan market, you can use a higher rate of about 10% since that's slightly below the normal return of long term bonds of 12-13%

That rule can only be used backwards to determine how much money you need to be financially free or to retire.

That rule can only be used backwards to determine how much money you need to be financially free or to retire.

3. 50/30/20 Budgeting rule.

If you struggle with budgeting your money, this rule will help you stick to the basics of budgeting.

It suggests that:

50% of your net income should be used to meet your needs (things you can't live without)

30% should be allocated toy our wants

20% should be allocated to savings and investments

If you struggle with budgeting your money, this rule will help you stick to the basics of budgeting.

It suggests that:

50% of your net income should be used to meet your needs (things you can't live without)

30% should be allocated toy our wants

20% should be allocated to savings and investments

4/ 100 minus age rule

This rule helps you determine an appropriate asset allocation rule in your portfolio.

It suggests that you should subtract your age from 100 to determine the allocation to Equities and the rest to debt instruments (bonds)

E.g. If you are 30 years old, you should allocate 70% of your portfolio in Equities and 30% in bonds.

This rule helps you determine an appropriate asset allocation rule in your portfolio.

It suggests that you should subtract your age from 100 to determine the allocation to Equities and the rest to debt instruments (bonds)

E.g. If you are 30 years old, you should allocate 70% of your portfolio in Equities and 30% in bonds.

The rule shifts your asset allocation strategy from equities (high risk) to bonds (low risk) as you age or approach retirement.

This is because, when you are young, you have a higher ability to take risk to maximize portfolio growth.

But when you are approaching retirement, your main goal is wealth preservation hence you can't afford to expose your portfolio to high risks

This is because, when you are young, you have a higher ability to take risk to maximize portfolio growth.

But when you are approaching retirement, your main goal is wealth preservation hence you can't afford to expose your portfolio to high risks

5. 3-6 months Expense's rule

This is a rule to guide you on how much emergency fund is enough before you start investing.

The rule suggests that your emergency fund should cater for your normal expenses for a period of 3-6 months

This is a rule to guide you on how much emergency fund is enough before you start investing.

The rule suggests that your emergency fund should cater for your normal expenses for a period of 3-6 months

6. The 2X purchase price rule

This is a rule that can guide you whenever you are making huge purchases.

The rule suggests that if you can't buy something twice, then you still can't afford it.

This rule aims to help people from spending a huge chunk of their savings or income on a material item

This is a rule that can guide you whenever you are making huge purchases.

The rule suggests that if you can't buy something twice, then you still can't afford it.

This rule aims to help people from spending a huge chunk of their savings or income on a material item

7. 25X Retirement Rule

This rule suggests that when it comes to retirement savings, you need to save 25 times your annual expenses.

However, this rule assumes a 4% withdrawal rate in retirement which is a USD rate used in U.S.

The Kenyan equivalent is 12 times your annual income with an expected withdrawal rate of 9% in retirement.

This rule suggests that when it comes to retirement savings, you need to save 25 times your annual expenses.

However, this rule assumes a 4% withdrawal rate in retirement which is a USD rate used in U.S.

The Kenyan equivalent is 12 times your annual income with an expected withdrawal rate of 9% in retirement.

8/ 28% Rule

This rule suggests that you should not spend more than 28% of your net income to meet household expenses like mortgage repayments or rent expenses.

This rule helps you to determine or estimate your housing expenses relative to your income.

This rule suggests that you should not spend more than 28% of your net income to meet household expenses like mortgage repayments or rent expenses.

This rule helps you to determine or estimate your housing expenses relative to your income.

9/ Rule of 72(Inflation)

The rule of 72 can also be used to determine how long it would take inflation to reduce the purchasing power of your money into half.

If the inflation rate for a certain period is 5%

Then it will take 72 divide by 5 = 14.4yrs for inflation to reduce the purchasing power of your savings into half.

This rule helps emphasize the importance of saving money in avenues that beat inflation rate.

The rule of 72 can also be used to determine how long it would take inflation to reduce the purchasing power of your money into half.

If the inflation rate for a certain period is 5%

Then it will take 72 divide by 5 = 14.4yrs for inflation to reduce the purchasing power of your savings into half.

This rule helps emphasize the importance of saving money in avenues that beat inflation rate.

10. Bonus rule

Personal finance is very personal and these rules are only used for guidance purposes and doesn't necessarily mean that you should follow them.

Let your personal finance and investment decisions be guided by your personal finance goals.

Stick to the ones that make sense to you and break the ones you don't agree with.

Personal finance is very personal and these rules are only used for guidance purposes and doesn't necessarily mean that you should follow them.

Let your personal finance and investment decisions be guided by your personal finance goals.

Stick to the ones that make sense to you and break the ones you don't agree with.

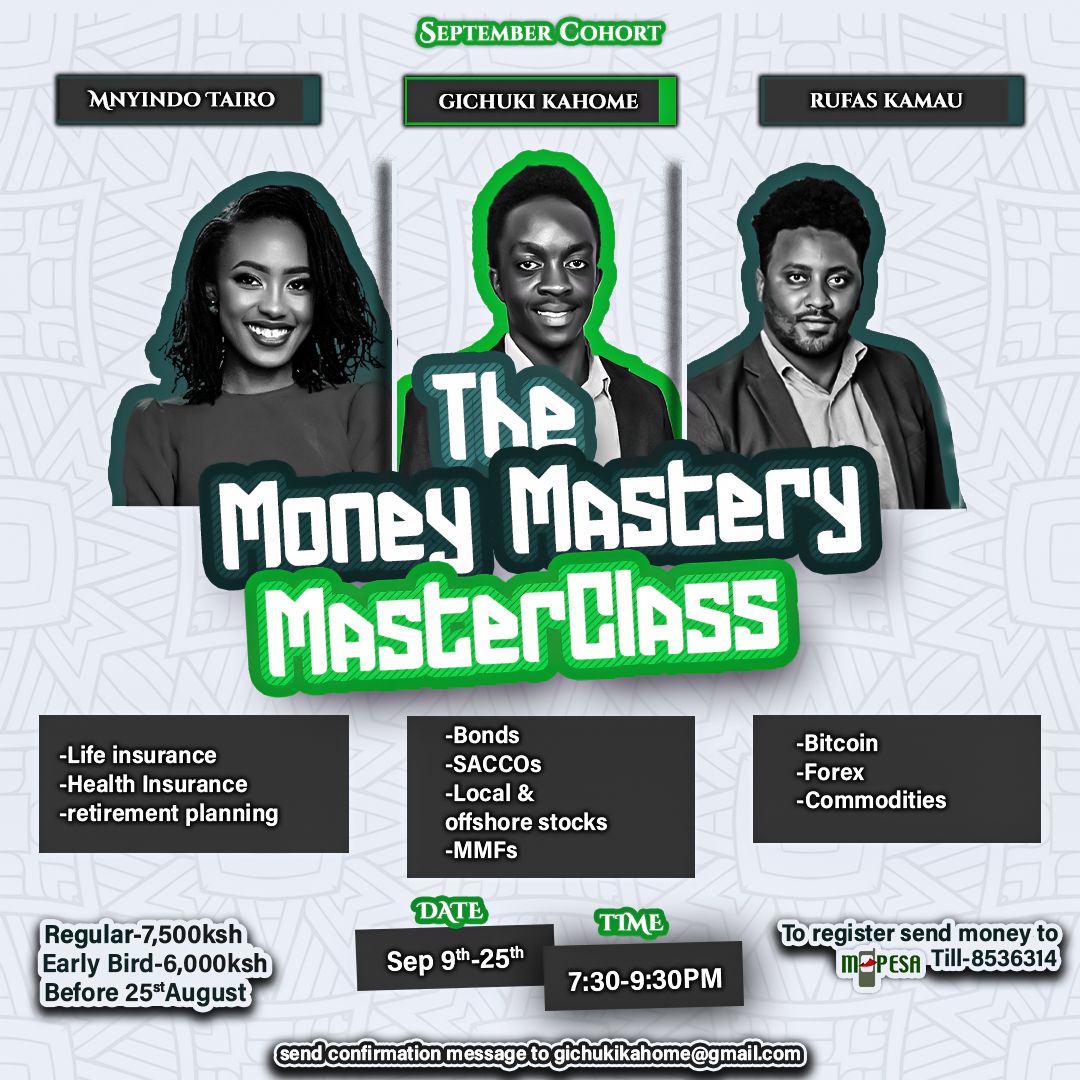

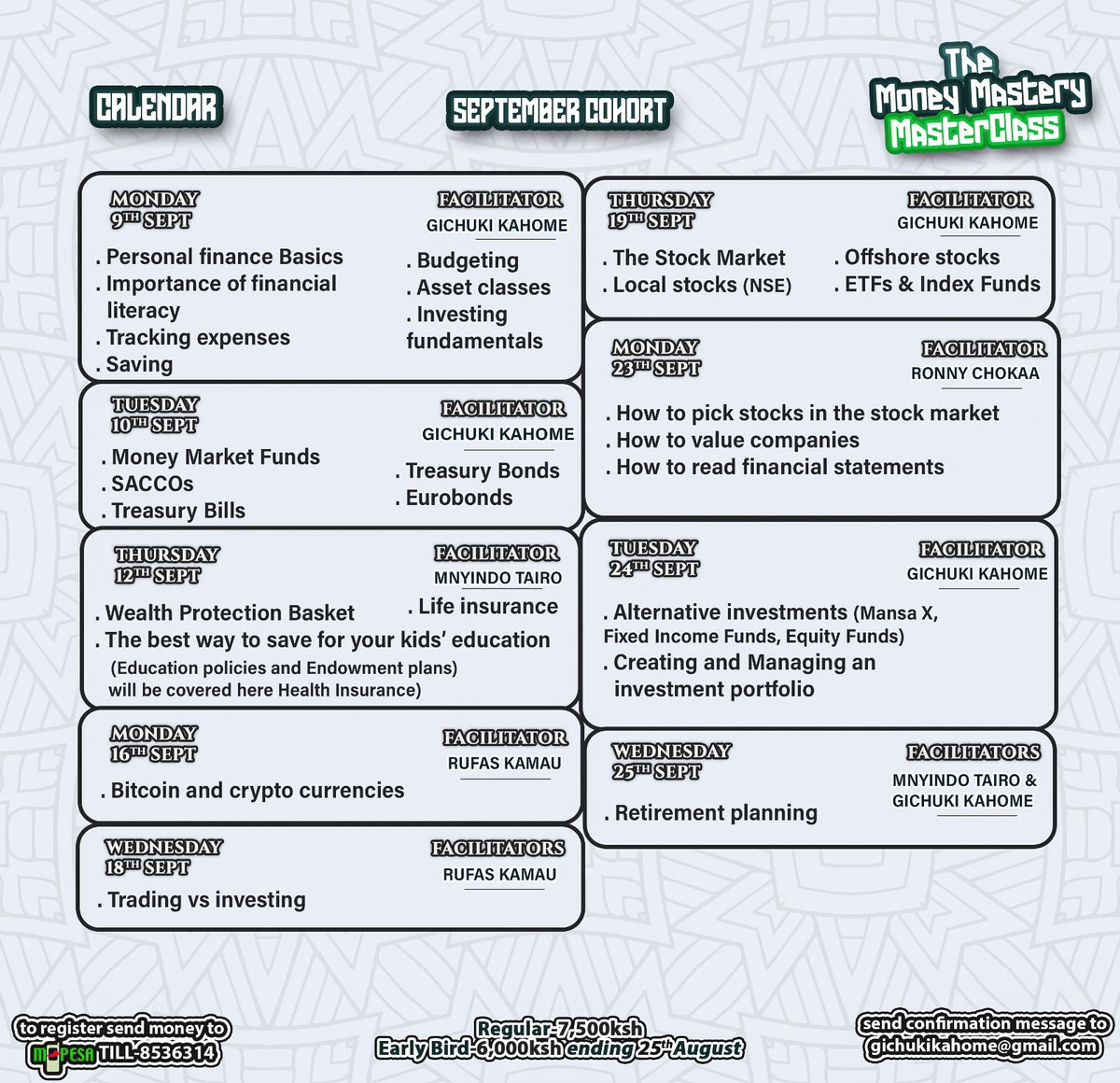

Registration for our Money Mastery Masterclass, September Cohort is now open

Enroll today to enjoy the early Bird discount

We cover:

MMFs, SACCOs, Stocks, offshore stocks & ETFs, Bitcoin, Life Insurance, Tbonds, Eurobonds, etc

Join us to level up your financial literacy

Enroll today to enjoy the early Bird discount

We cover:

MMFs, SACCOs, Stocks, offshore stocks & ETFs, Bitcoin, Life Insurance, Tbonds, Eurobonds, etc

Join us to level up your financial literacy

Loading suggestions...