How to fetch free options data and price a straddle with Python:

In this quick thread, you'll get Python code to:

• Fetch options data using Python

• Generate long straddle prices

• Design a risk profile

Let's go!

• Fetch options data using Python

• Generate long straddle prices

• Design a risk profile

Let's go!

First start with the imports.

The next step is to grab the unique expirations and filter the DataFrame with the options for calls and puts separately for the expiration date we care about.

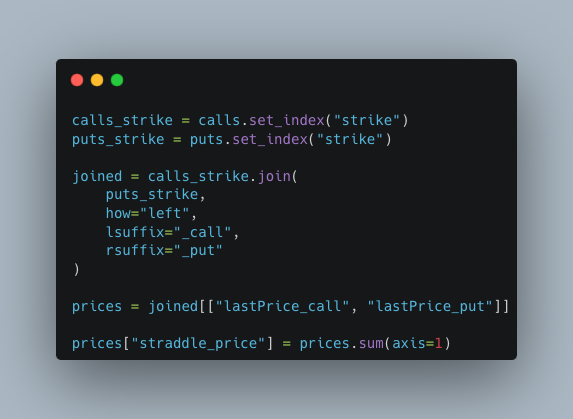

Next we’ll join the DataFrames with the calls and puts and compute the prices.

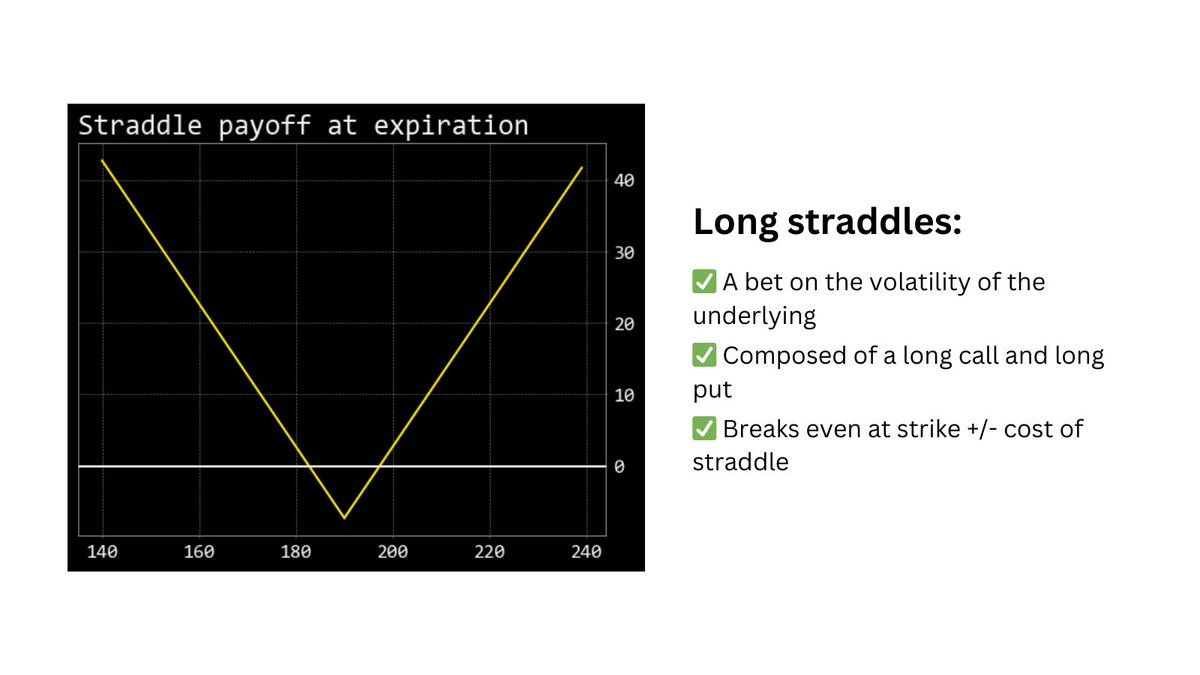

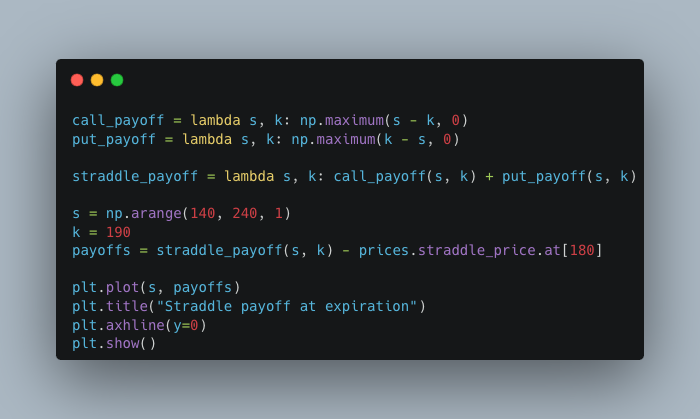

Now we can design the risk profile.

The result is the straddle payoff at expiration.

So what's next?

1. Model a short straddle (hint: it’s the opposite of a long straddle)

2. Use an options pricing model to model the options price before expiration

1. Model a short straddle (hint: it’s the opposite of a long straddle)

2. Use an options pricing model to model the options price before expiration

Looking to start using Python for quant finance?

Here's a free Ultimate Guide with everything you need to get started.

Join the 1,000s of people who finally started with Python after reading it:

links.pyquantnews.com

Here's a free Ultimate Guide with everything you need to get started.

Join the 1,000s of people who finally started with Python after reading it:

links.pyquantnews.com

Loading suggestions...