In this Detailed Thread 🧵 we'll look to analyse a Microcap Company 'PARNAX LAB LTD 🧪' Each and every neeche details about this company will be covered in this thread from its Business, to its fundamentals, to its product mix, to its financials, to its

#ParnaxLab

#ParnaxLab

Management, to its Chart Pattern analysis 📉📈, to its valuation gap ⚖️♎ and at last I'll give my final commentary👨💻 about this stock.

☑️ABOUT THE COMPANY

💫Parnax Lab was Incorporated in 1985, Parnax Lab Ltd manufactures and exports Pharmaceutical Formulations.

☑️ABOUT THE COMPANY

💫Parnax Lab was Incorporated in 1985, Parnax Lab Ltd manufactures and exports Pharmaceutical Formulations.

☑️Business Overview:-

💫PLL is a part of the Naxpar Group and is a WHO-approved and EHS-compliant Company.

💫It is into contract manufacturing of Liquid Orals, Capsules, Ointments, External Powders & Tablets with its manufacturing facility located

at Silvassa.

💫PLL is a part of the Naxpar Group and is a WHO-approved and EHS-compliant Company.

💫It is into contract manufacturing of Liquid Orals, Capsules, Ointments, External Powders & Tablets with its manufacturing facility located

at Silvassa.

☑️International Presence:-

💫Company manufactures finished formulations for multinationals in India and in emerging pharmaceutical markets such as Nigeria, Kazakhstan, Kenya, Mauritius and is planning to venture into markets of South East Asia, CIS, LatAm, etc.

💫Company manufactures finished formulations for multinationals in India and in emerging pharmaceutical markets such as Nigeria, Kazakhstan, Kenya, Mauritius and is planning to venture into markets of South East Asia, CIS, LatAm, etc.

as a pharmaceuticals, cosmetics and herbal products manufacturer.

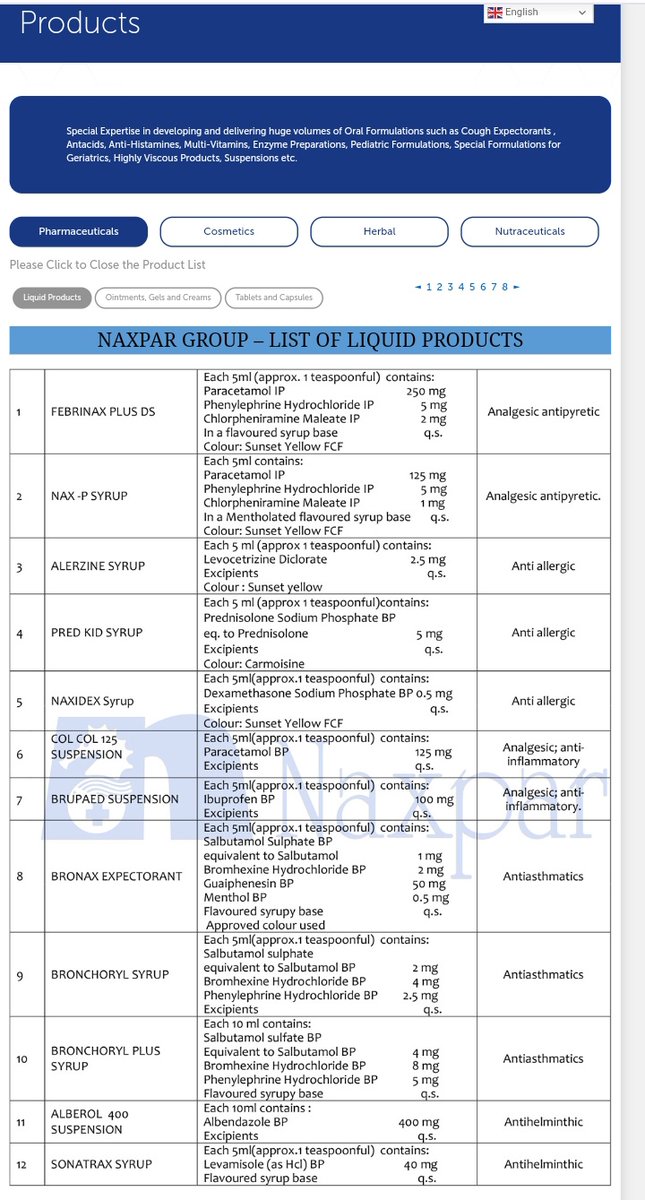

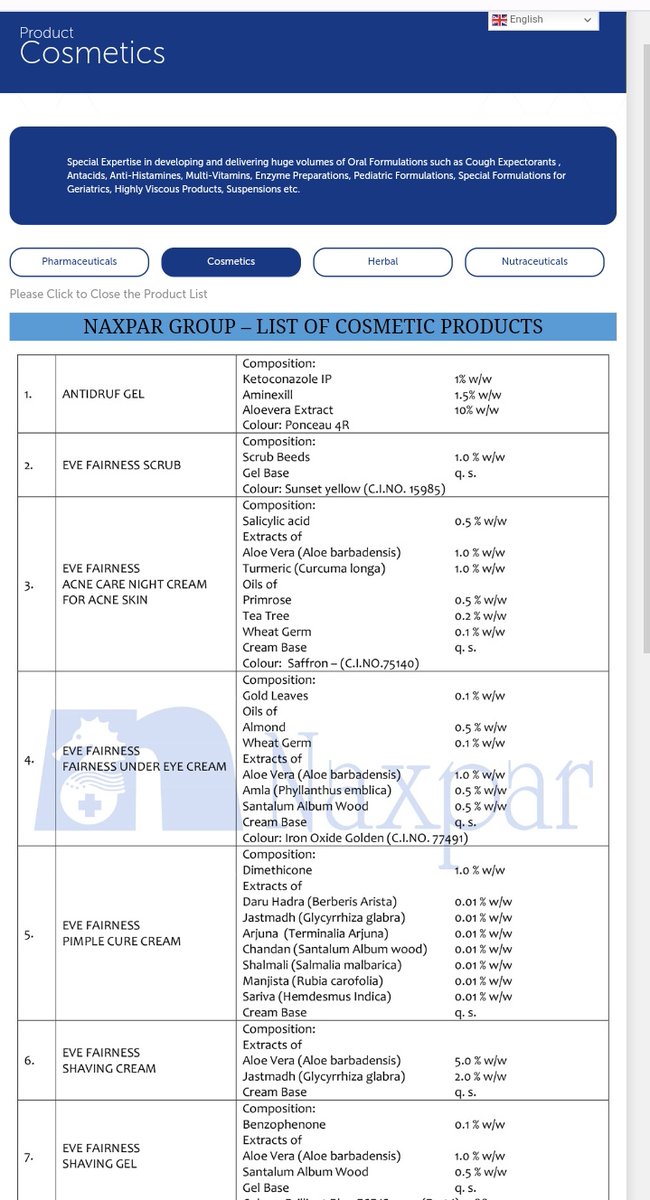

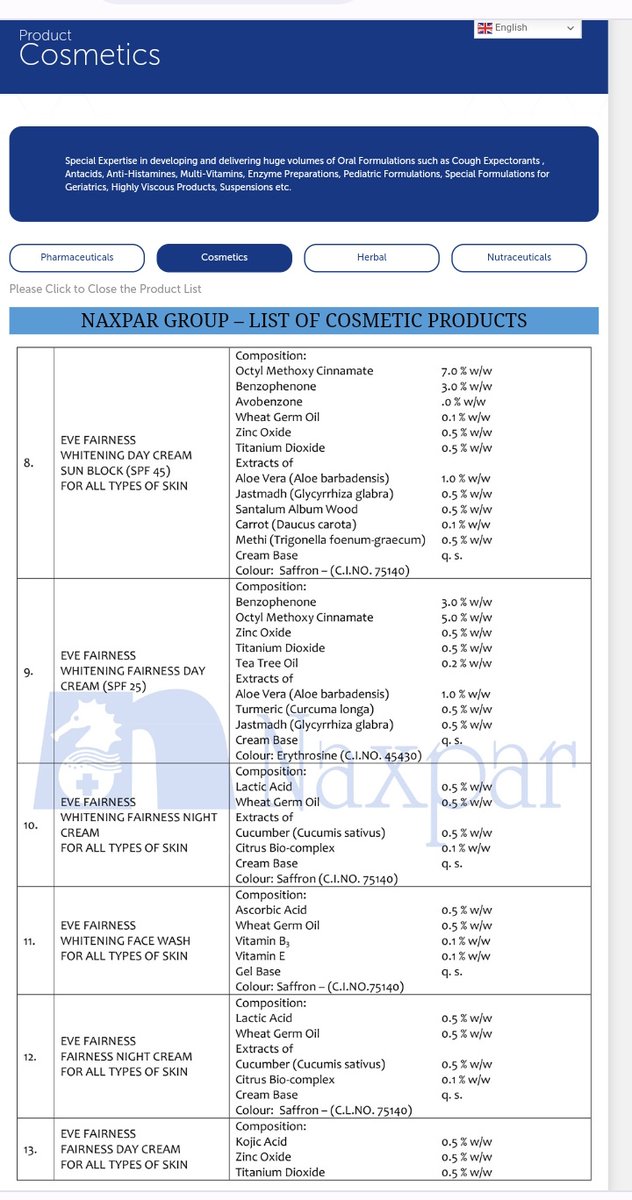

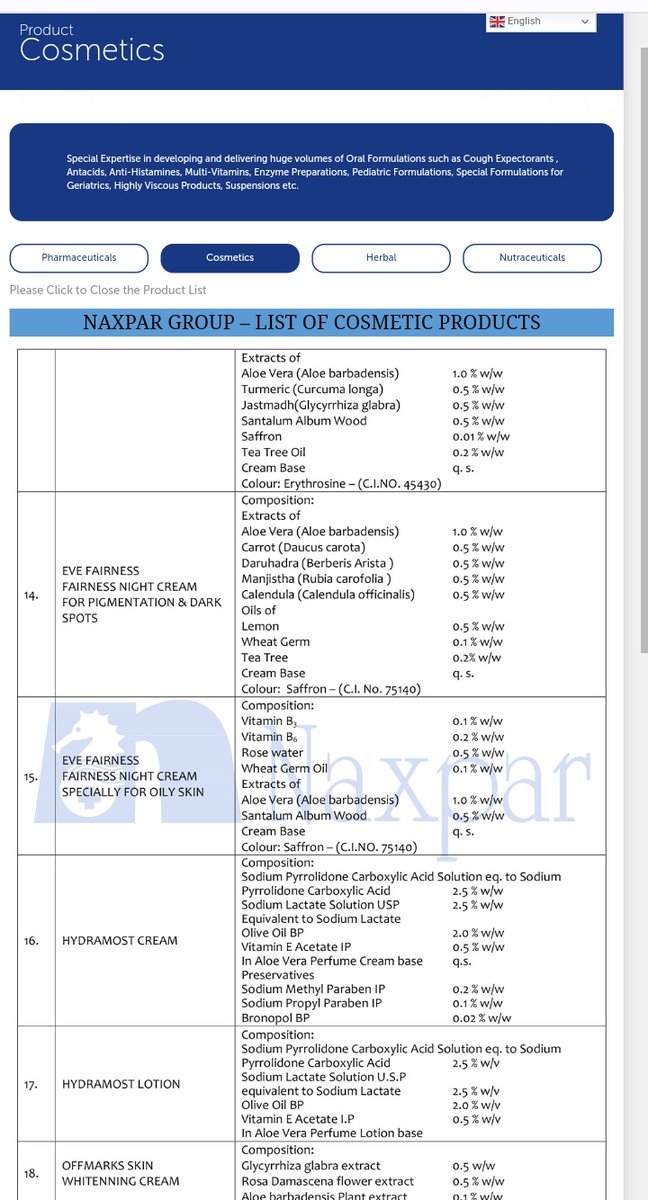

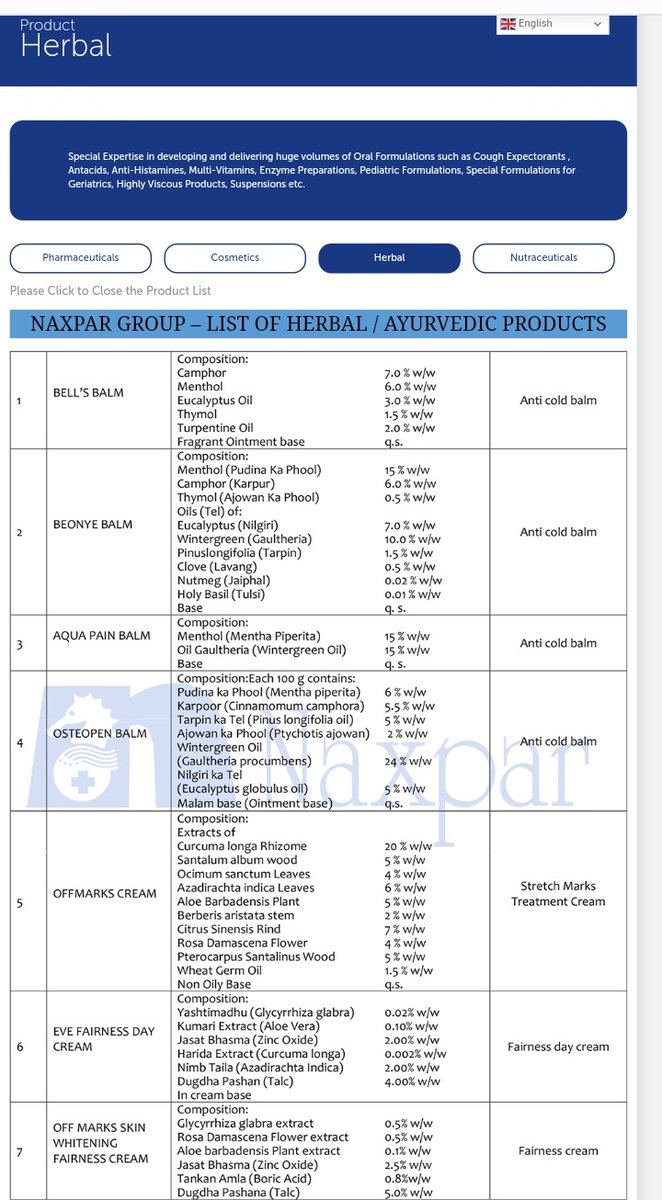

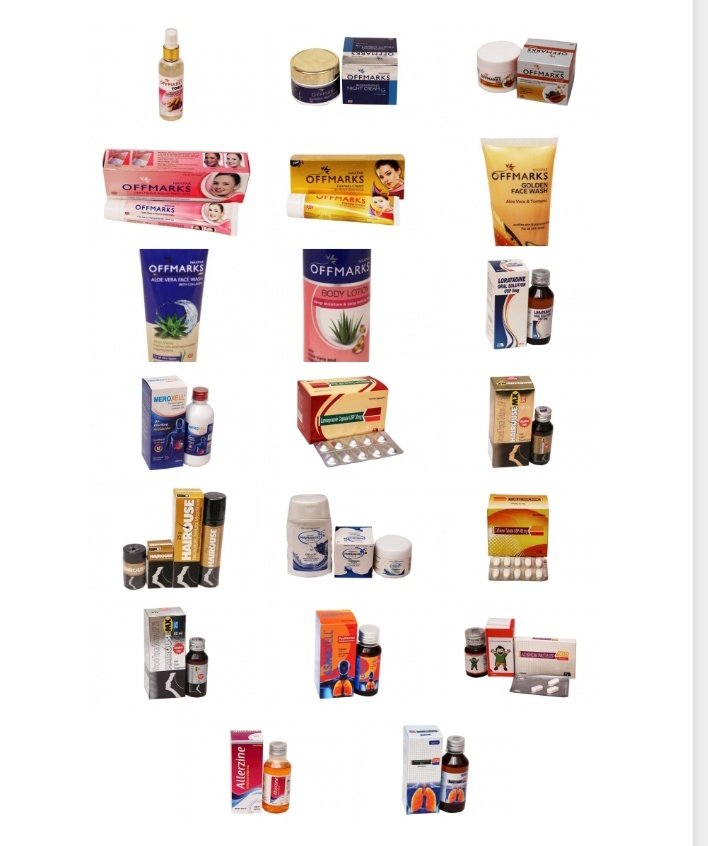

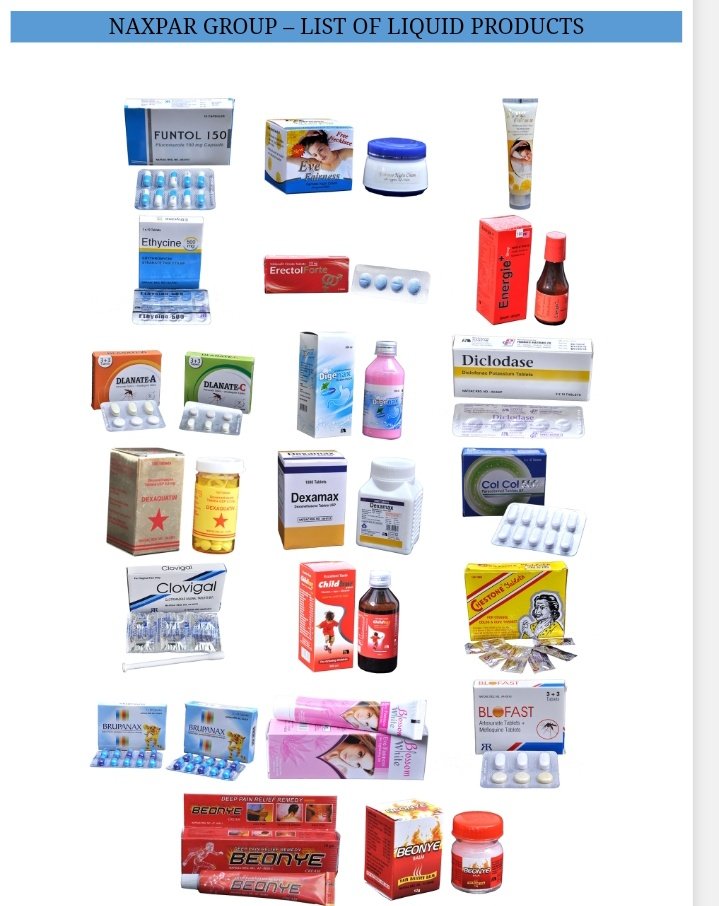

☑️Product Profile:-

💫Company specializes in developing and delivering high volume Oral Formulations viz. Cough Expectorants , Antacids, Anti-Histamines, Multi-Vitamins, Enzymes, Pediatric Formulations, Special

☑️Product Profile:-

💫Company specializes in developing and delivering high volume Oral Formulations viz. Cough Expectorants , Antacids, Anti-Histamines, Multi-Vitamins, Enzymes, Pediatric Formulations, Special

Formulations for Geriatrics, Highly Viscous Products, Suspensions etc.

These includes:-

a) Pharmaceuticals:

Liquid Products, Ointments, Gels and Creams, Tablets and Capsules, etc.

b) Cosmetics:

Antidruf Gel, EVE Fairness Creams, Hydramost Cream, Off Marks Cream, UV Block Cream,

These includes:-

a) Pharmaceuticals:

Liquid Products, Ointments, Gels and Creams, Tablets and Capsules, etc.

b) Cosmetics:

Antidruf Gel, EVE Fairness Creams, Hydramost Cream, Off Marks Cream, UV Block Cream,

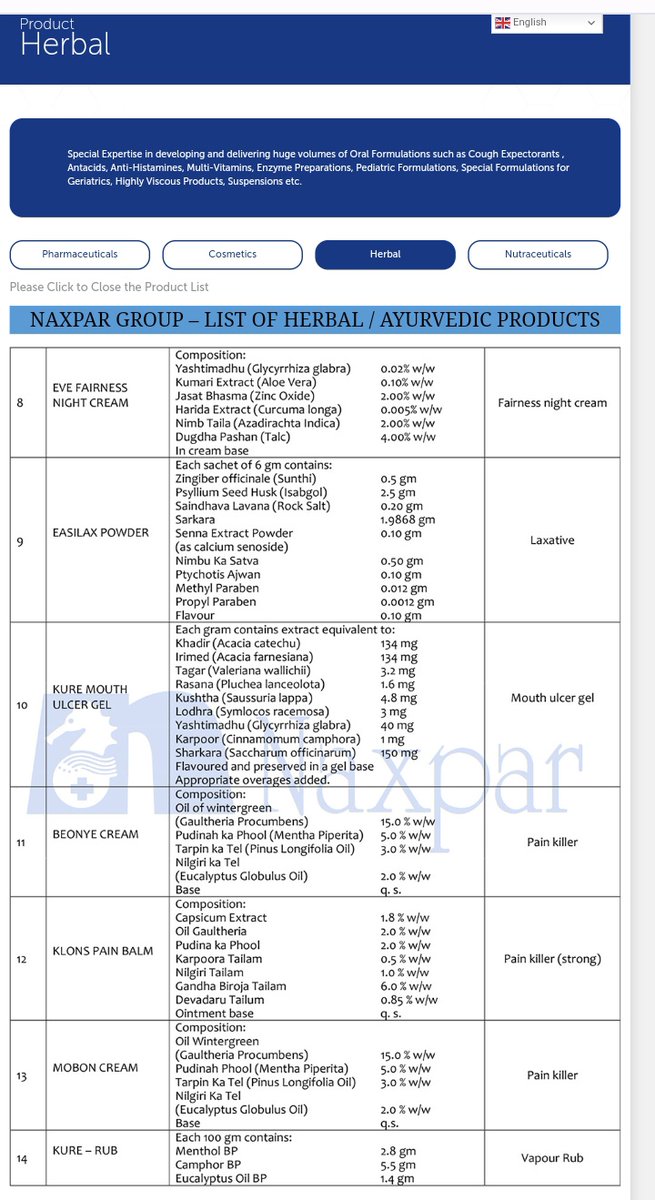

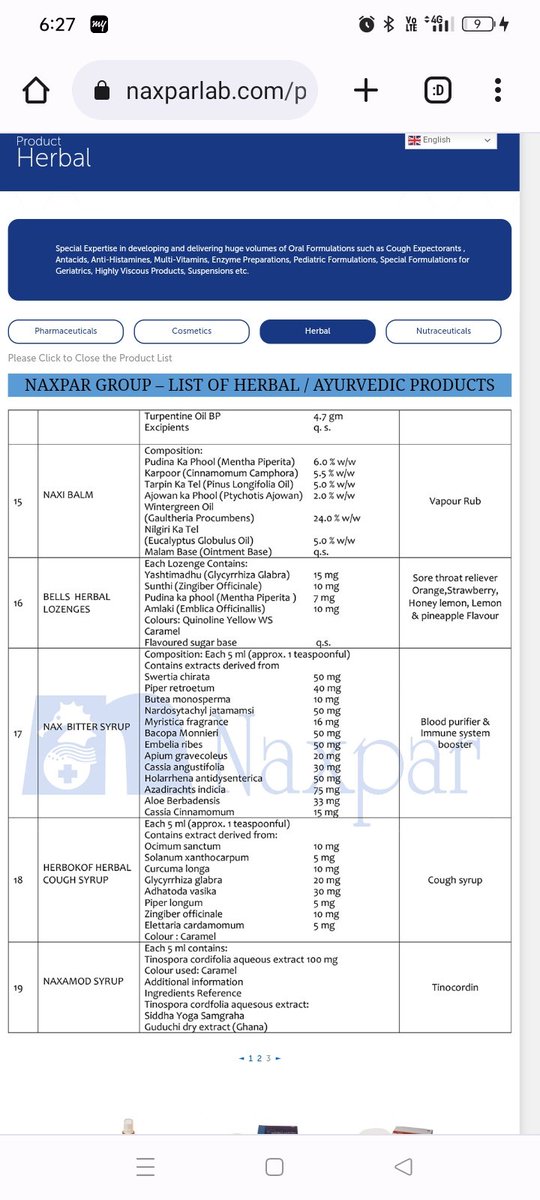

c) Herbal:

Bell's Balm, Beonye Balm, Aqua Pain Balm, Osteopen Balm, Easilax powder, Kure Gel, etc.

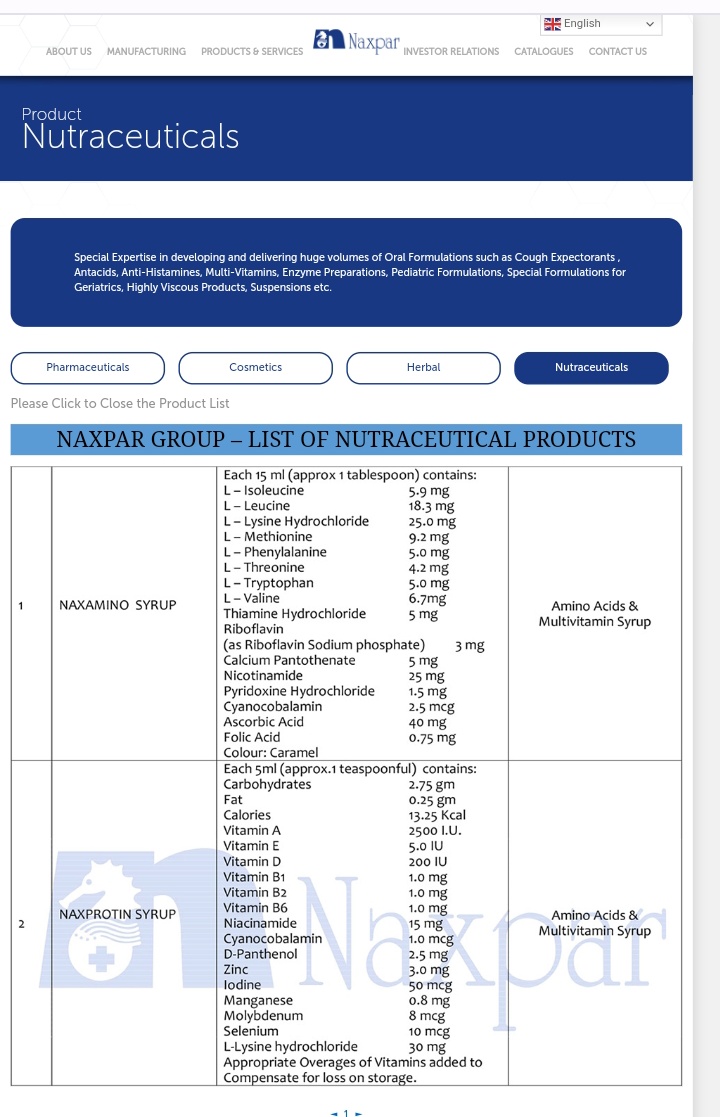

d) Nutraceutical:

Naxamino Syrup, Naxprotein Syrup

Services Offered:

a) Identifying and Developing Drug/ Product

b) Gaining Regulatory Approval

c) In and Out Licensing

Bell's Balm, Beonye Balm, Aqua Pain Balm, Osteopen Balm, Easilax powder, Kure Gel, etc.

d) Nutraceutical:

Naxamino Syrup, Naxprotein Syrup

Services Offered:

a) Identifying and Developing Drug/ Product

b) Gaining Regulatory Approval

c) In and Out Licensing

d) NDDS and Manufacturing Tie-Ups

e) CRAMS

☑️Customer Base:

💫Himalaya, L'Oreal, Sun Pharma, Cipla, Dabur, Cipla, Wockhardt, Ranbaxy, etc

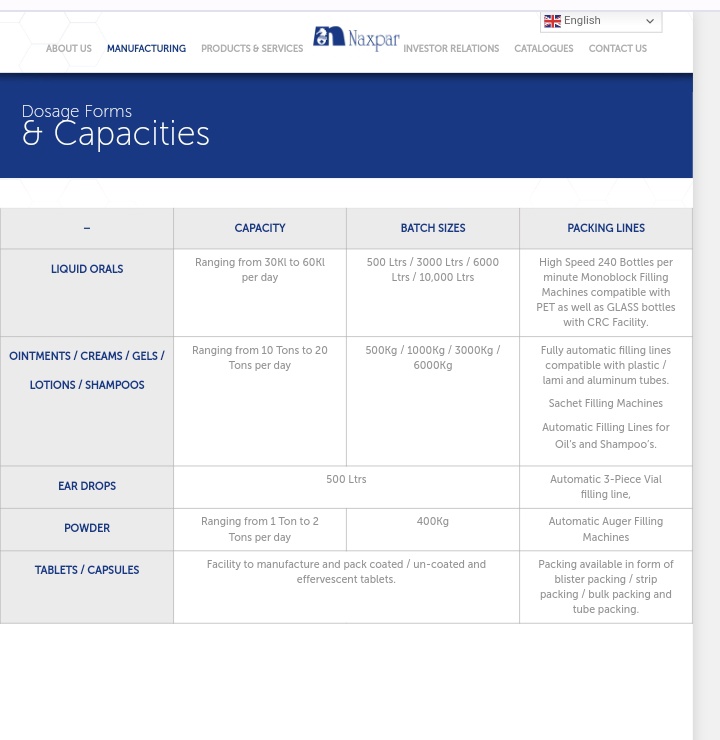

☑️Production Capacity:

a) Liquid Orals ~30Kl to 60Kl per day

b) Ointments / Creams / Gels / Lotions / Shampoos ~10 Tons to 20 Tons per day

e) CRAMS

☑️Customer Base:

💫Himalaya, L'Oreal, Sun Pharma, Cipla, Dabur, Cipla, Wockhardt, Ranbaxy, etc

☑️Production Capacity:

a) Liquid Orals ~30Kl to 60Kl per day

b) Ointments / Creams / Gels / Lotions / Shampoos ~10 Tons to 20 Tons per day

c) Ear Drops ~500 Ltrs

d) Powder ~1 Ton to 2 Tons per day

☑️Revenue Breakup - FY22:

Sale of Goods ~73%,

Sale of Services - Labour Charges ~ 27%

d) Powder ~1 Ton to 2 Tons per day

☑️Revenue Breakup - FY22:

Sale of Goods ~73%,

Sale of Services - Labour Charges ~ 27%

Fundamental Analysis♎⚖️

✅Market Capitalisation:- Rs 105 Cr(Microcap)

✅Stock PE:- 11.9(Undervalued)

✅Industry PE:- 30.7

✅Book Value:- Rs 58.6

✅Dividend Yield:- 0%

✅ROCE:- 14.8%

✅ROE:- 15.9%

✅Face Value:- 10

✅Intrinsic Value:- Rs 68.5

✅Graham No:- Rs 101

✅Market Capitalisation:- Rs 105 Cr(Microcap)

✅Stock PE:- 11.9(Undervalued)

✅Industry PE:- 30.7

✅Book Value:- Rs 58.6

✅Dividend Yield:- 0%

✅ROCE:- 14.8%

✅ROE:- 15.9%

✅Face Value:- 10

✅Intrinsic Value:- Rs 68.5

✅Graham No:- Rs 101

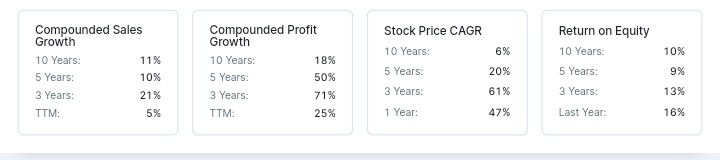

✅3 Years Sales Growth:- 21%

✅3 Years Net Profits Growth:- 71%

✅EPS:- 7.67

✅Debt to Equity:- 1.05

✅Debt:- Rs 59 Cr

✅Reserves:- Rs 56 Cr

✅Fixed Assets:- 89 Cr

✅Piotroski Score:- 5

✅PEG:- 0.24

✅ Pledged %:- 9.41%

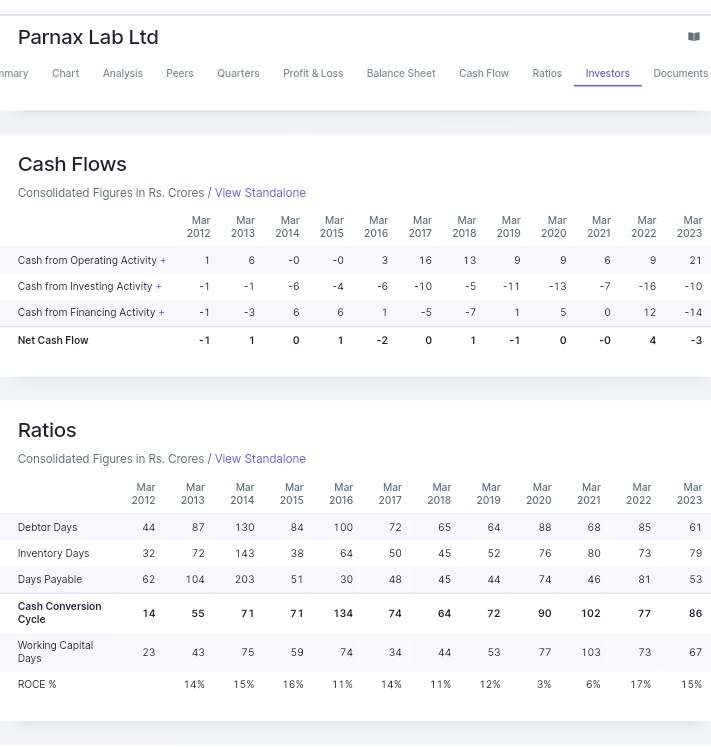

Last 3/5/10 Years Sales Growth💹Profit💹,CAGR,ROE,AR,CF👇

✅3 Years Net Profits Growth:- 71%

✅EPS:- 7.67

✅Debt to Equity:- 1.05

✅Debt:- Rs 59 Cr

✅Reserves:- Rs 56 Cr

✅Fixed Assets:- 89 Cr

✅Piotroski Score:- 5

✅PEG:- 0.24

✅ Pledged %:- 9.41%

Last 3/5/10 Years Sales Growth💹Profit💹,CAGR,ROE,AR,CF👇

☑️Chart Pattern Analysis📉📈, Financial Analysis♎⚖️, Valuation Gap and My Final Commentary

Chart Pattern Analysis(Monthly Timeframe)

✅The stock is trading above all the EMAs and DMAs

✅The stock is consolidating in a Darvax Box Pattern

✅8 Months old Breakout is possible

Chart Pattern Analysis(Monthly Timeframe)

✅The stock is trading above all the EMAs and DMAs

✅The stock is consolidating in a Darvax Box Pattern

✅8 Months old Breakout is possible

in Parnax above Rs 110+ CBS

✅21 Months old Breakout is possible in Parnax Lab above Rs 117+ CBS

✅Above Rs 117 CBS it will go into an uncharted territory and face the next resistance at Rs 170+

✅The ATH(All time Highs) of the Parnax is placed at Rs 190(ATH came in Nov-2011)

✅21 Months old Breakout is possible in Parnax Lab above Rs 117+ CBS

✅Above Rs 117 CBS it will go into an uncharted territory and face the next resistance at Rs 170+

✅The ATH(All time Highs) of the Parnax is placed at Rs 190(ATH came in Nov-2011)

Fundamental Analysis, Valuation and my Commentary

☑️Fundamental Analysis ⚖️♎

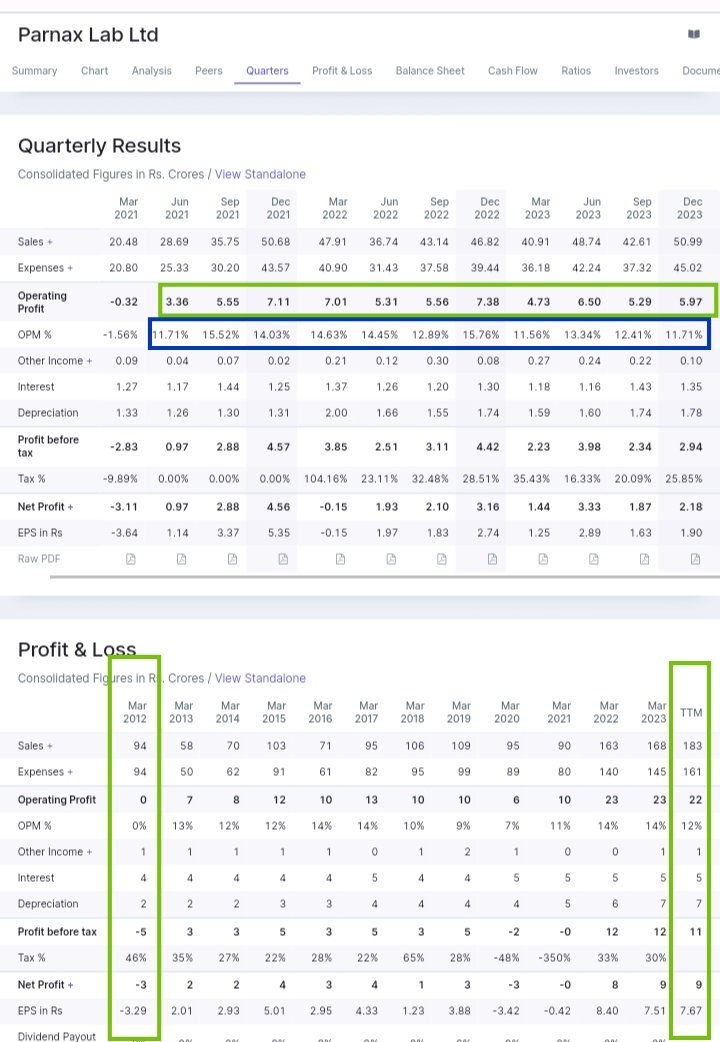

✅In FY24 on TTM Basis(Presumably Assuming that Q4 Sales to be a repeat of Q3FY24) Parnax Lab has a potential to do Sales of Rs 193 Cr

✅Parnax Lab Sales will increase by 15% on YOY Basis(Expected)

☑️Fundamental Analysis ⚖️♎

✅In FY24 on TTM Basis(Presumably Assuming that Q4 Sales to be a repeat of Q3FY24) Parnax Lab has a potential to do Sales of Rs 193 Cr

✅Parnax Lab Sales will increase by 15% on YOY Basis(Expected)

✅If Parnax Lab sees a Sales of Rs 190+ Cr in FY24 then this will be its highest ever Sales in its Business History

✅Parnax Lab Operating Profits of FY24(Presumably Assuming that Q4 Operating Profits will be a repeat of Q3) Parnax Lab has the potential to do Rs 23.73 Cr

✅Parnax Lab Operating Profits of FY24(Presumably Assuming that Q4 Operating Profits will be a repeat of Q3) Parnax Lab has the potential to do Rs 23.73 Cr

Operating Profits in FY24

✅The OPM of last 11 Quarters ranges from 11.71% to 15.52%

(As per the Annual Reports the company is optimistic for the growth in the Short term and medium Term in terms of total revenues and operating margins considering overall expected positive trend

✅The OPM of last 11 Quarters ranges from 11.71% to 15.52%

(As per the Annual Reports the company is optimistic for the growth in the Short term and medium Term in terms of total revenues and operating margins considering overall expected positive trend

In the Pharmaceutical Industry)

✅Since this is a very small company they do not do any Concall but one thing to note here is that the company has been able to double its Revenue in the past 3 Years

✅In FY21 its Revenue was only at Rs 90 Cr and now in TTM Basis its Revenue is

✅Since this is a very small company they do not do any Concall but one thing to note here is that the company has been able to double its Revenue in the past 3 Years

✅In FY21 its Revenue was only at Rs 90 Cr and now in TTM Basis its Revenue is

Rs 193 Cr

✅If the company maintains the increasing Sales trajectory and acheives a decent OPM% Growth in FY25 Financial Year then its valuations will become much more justified and undervalued

✅At its ATH of Rs 190 Parnax used to do only Rs 94 Cr Sales and its Margins was 0%

✅If the company maintains the increasing Sales trajectory and acheives a decent OPM% Growth in FY25 Financial Year then its valuations will become much more justified and undervalued

✅At its ATH of Rs 190 Parnax used to do only Rs 94 Cr Sales and its Margins was 0%

And its Operating Profits was at Rs 0 Cr

✅Now, it is doing Rs 193 Cr Sales(As per FY24 TTM) and Operating Profits is at Rs 23.74 Cr and Margins is hovering at 12-14%

✅Parnax is currently available at about 52% discounts from the ATH of Rs 190+

✅Now, it is doing Rs 193 Cr Sales(As per FY24 TTM) and Operating Profits is at Rs 23.74 Cr and Margins is hovering at 12-14%

✅Parnax is currently available at about 52% discounts from the ATH of Rs 190+

✅Promoters+ Big Investors are Holding 73.92% Stake or 78 Cr worth Shares. The public are holding 27 Cr worth Shares or 26.08% Stake

✅A Pharma company with Rs 193 Cr sales, Rs 23 Cr operating profits and 12-14% Margin available at just 105 Cr Market Cap is a very fair deal 🤝

✅A Pharma company with Rs 193 Cr sales, Rs 23 Cr operating profits and 12-14% Margin available at just 105 Cr Market Cap is a very fair deal 🤝

Disclaimer : Kindly consult your FA before buying / Selling any shares. This analysis is only for educational purposes and not recommendations.

Don't Buy on the basis of this thread 🧵 if you make profits you gonna not share with me likewise I'll not be responsible for loss too

Don't Buy on the basis of this thread 🧵 if you make profits you gonna not share with me likewise I'll not be responsible for loss too

Try to Retweet ♻️ this thread 🧵 so that it reaches more market participants as this company is very unknown. This thread took about 7 Hours time to be made so try to Retweet it so that it motivates me to bring more such Business thread in the future.

Loading suggestions...