Techno-Funda Analysis of Sonata Software: A Consistent Mid-Cap IT Company

Market Cap ~ 17,200 Cr

CMP ~ 1225

PE ~ 36

1 Yr Return ~ 135%

Let's deep dive into it 👇

Market Cap ~ 17,200 Cr

CMP ~ 1225

PE ~ 36

1 Yr Return ~ 135%

Let's deep dive into it 👇

#fundamental Analysis

1. Business Overview

2. Vertical/Segmental Analysis

3. Acquisition History

4. Financial Analysis

5. Opportunities

6. Risk

7. Valuation

8. Guidance

1. Business Overview

2. Vertical/Segmental Analysis

3. Acquisition History

4. Financial Analysis

5. Opportunities

6. Risk

7. Valuation

8. Guidance

Business Overview

-Sonata is provided IT Services & software solutions to its clients

-Sonata is present in US, Europe, Middle East, APAC and New Zealand (17 Nations in total)

-It operates in two verticals:

1. International IT Services(IITS)

2. Domestic Product & Services(DPS)

-Sonata is provided IT Services & software solutions to its clients

-Sonata is present in US, Europe, Middle East, APAC and New Zealand (17 Nations in total)

-It operates in two verticals:

1. International IT Services(IITS)

2. Domestic Product & Services(DPS)

Domestic Product Services Business

-Sonata here focuses on the distribution of packaged software/application, including resale of cloud hosting of different technology gaints like Microsoft

-A low margin, but high ROCE Cash rich Biz (Simply resaler of other Co. Product)

-Sonata here focuses on the distribution of packaged software/application, including resale of cloud hosting of different technology gaints like Microsoft

-A low margin, but high ROCE Cash rich Biz (Simply resaler of other Co. Product)

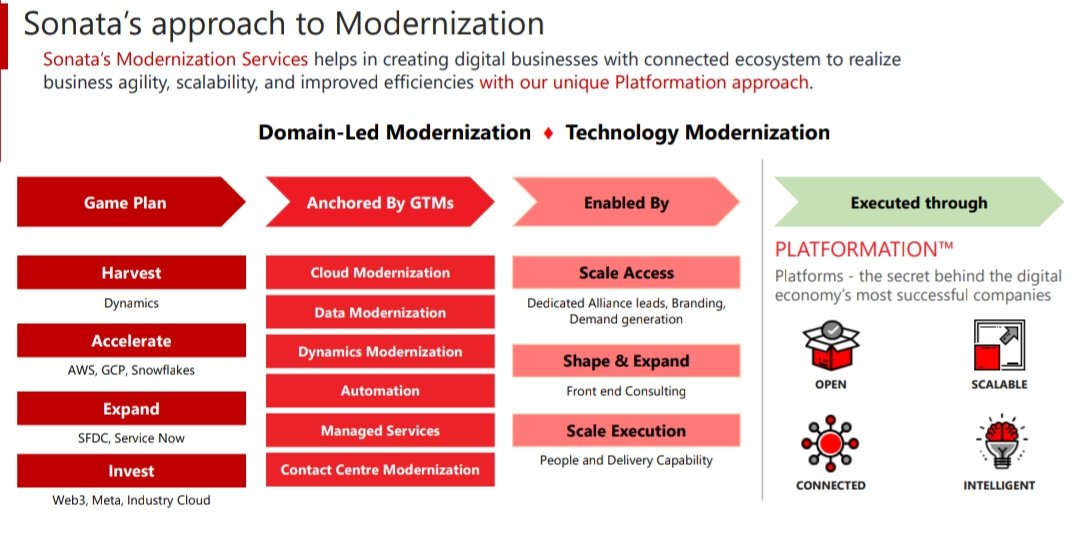

International IT Services Business (IITS)

-Sonata here provides customised & modernization services which improves consumer experience & growth, which help them achieve improved efficiency

-Its an High Margin-Low revenue contribution Vertical (A Premium vertical)

-Sonata here provides customised & modernization services which improves consumer experience & growth, which help them achieve improved efficiency

-Its an High Margin-Low revenue contribution Vertical (A Premium vertical)

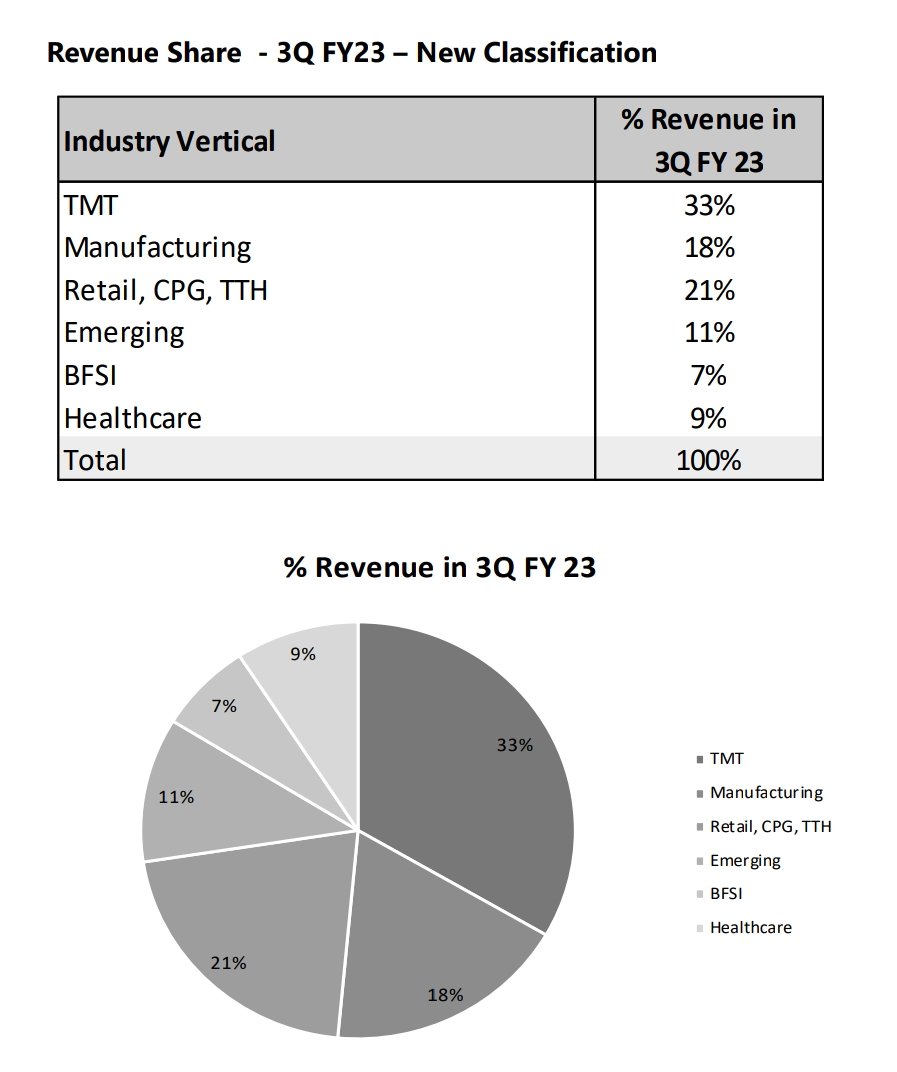

Caters to the following Industries like:

1. TMT: Technology Media & Telecom

2. RMD: Retail, Manuf., Travel & Distribution

3. BFSI: Banking, Financial & Insurance

4. HLS: Healthcare & Life science

5. Emerging

Revenue share 👇

1. TMT: Technology Media & Telecom

2. RMD: Retail, Manuf., Travel & Distribution

3. BFSI: Banking, Financial & Insurance

4. HLS: Healthcare & Life science

5. Emerging

Revenue share 👇

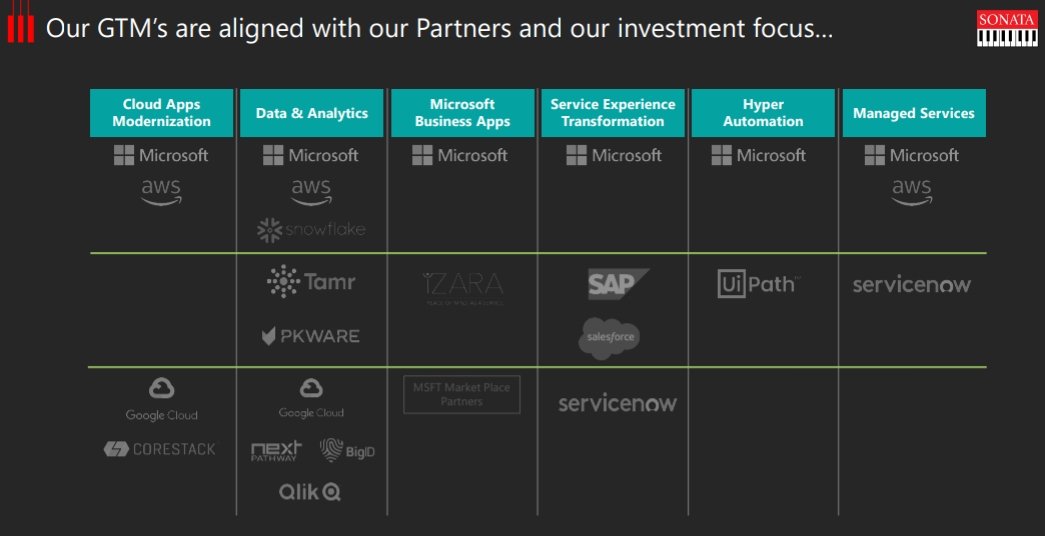

Partners: Ecosystem Partnership Tech + Domain

1. Microsoft

2. AWS

3. Google Cloud

4. Salesforce

5. Snowflake

6. Servicenow

7. Metricstream

8. SAP

Provide services like:

1. Cloud

2. Managed Services

3. Automation

4. AI & Data

5. Dynamics

6. Digital contact centre

1. Microsoft

2. AWS

3. Google Cloud

4. Salesforce

5. Snowflake

6. Servicenow

7. Metricstream

8. SAP

Provide services like:

1. Cloud

2. Managed Services

3. Automation

4. AI & Data

5. Dynamics

6. Digital contact centre

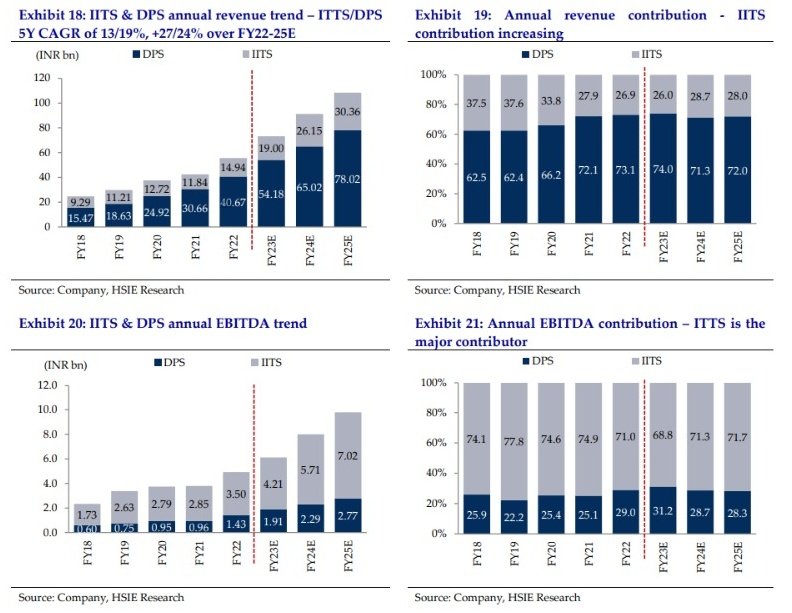

Revenue Contribution:

1. International IT Services(IITS)

-Low Revenue Contribution (26.5%)

-High margin (Low 20s)

2. Domestic Product & Services(DPS)

-High Revenue Contribution (73.5%)

-Low Margin (Low single degit)

Sonata Want to make IITS Biz as majority contri going forward

1. International IT Services(IITS)

-Low Revenue Contribution (26.5%)

-High margin (Low 20s)

2. Domestic Product & Services(DPS)

-High Revenue Contribution (73.5%)

-Low Margin (Low single degit)

Sonata Want to make IITS Biz as majority contri going forward

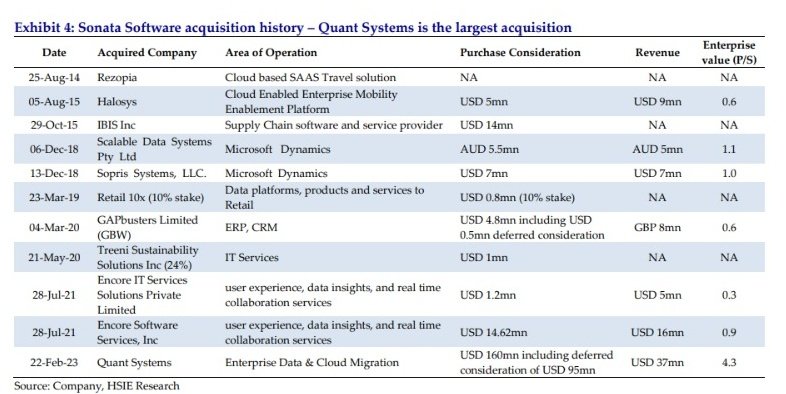

Acquisition History of Sonata:

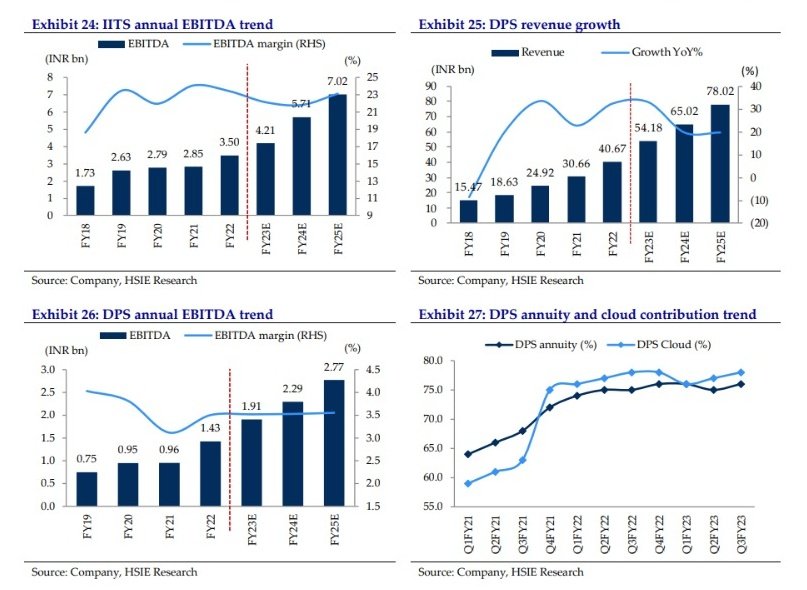

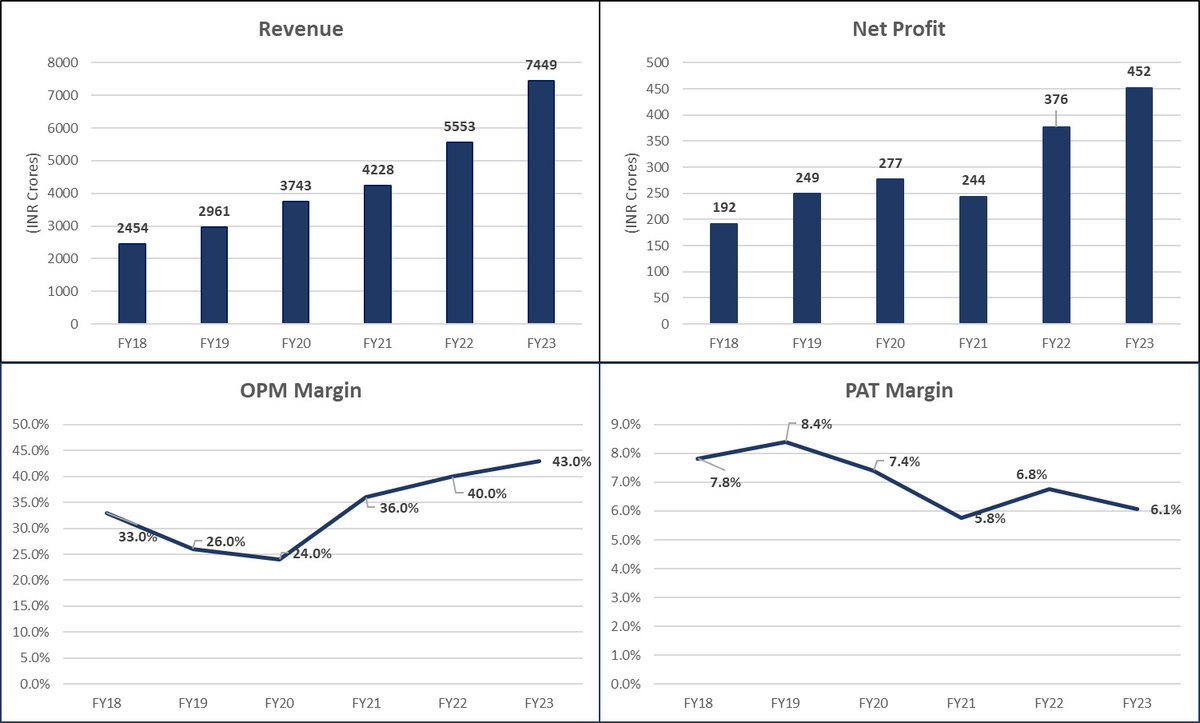

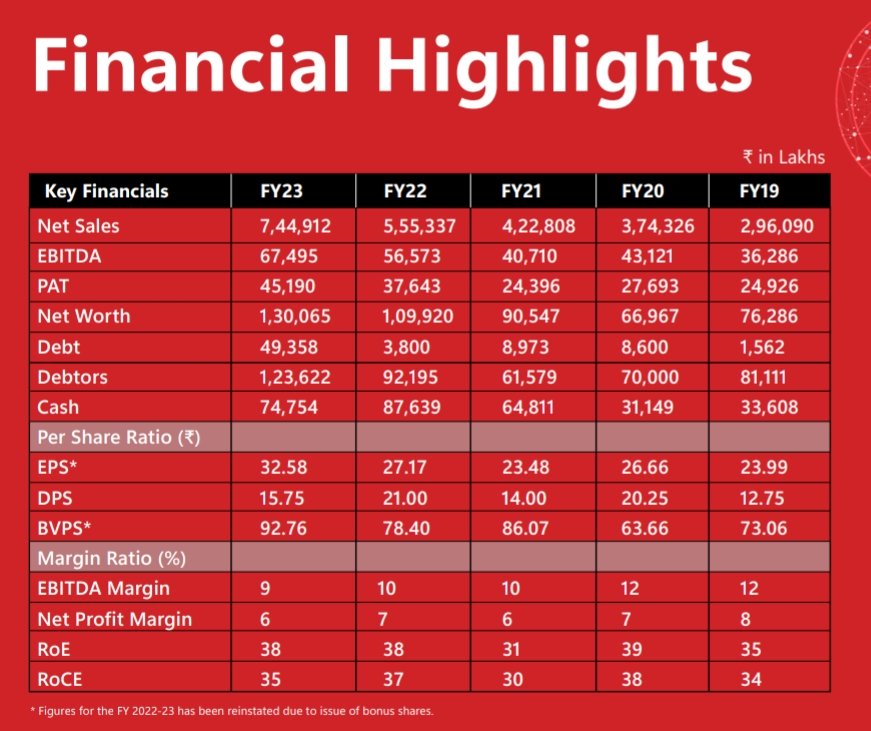

Financial Analysis:

-Revenue Growth of 25% in last 5 years

-OPM Margin consistent around 8-9% from last 3-4 years

-PAT Growth of 19% in last 5 years (Lower due to acquisition leading to High Int & Dep exp)

-PAT Margin of around 6%

-ROCE: 39%

-ROE: 38%

-Dividend Payout Ratio: 48%

-Revenue Growth of 25% in last 5 years

-OPM Margin consistent around 8-9% from last 3-4 years

-PAT Growth of 19% in last 5 years (Lower due to acquisition leading to High Int & Dep exp)

-PAT Margin of around 6%

-ROCE: 39%

-ROE: 38%

-Dividend Payout Ratio: 48%

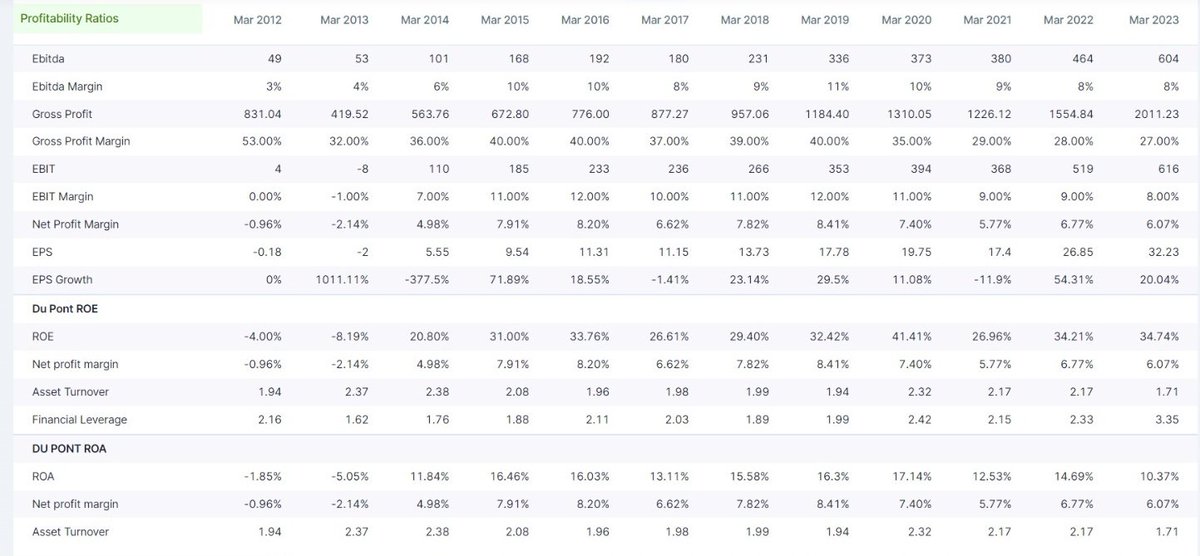

Other Metrics:

-Revenue per employee has started inching upward after a steep fall, due to COVID

-Major cost in P&L is Stock in Trade (RM) & Employee

-Sonata has good CFO Conversion with CFO to PAT at around 90% average

-Profitablity Ratios

-Revenue per employee has started inching upward after a steep fall, due to COVID

-Major cost in P&L is Stock in Trade (RM) & Employee

-Sonata has good CFO Conversion with CFO to PAT at around 90% average

-Profitablity Ratios

Opportunities

1. Rise in contribution of high margin IITS Vertical

2. Reputed Partnership network, which consists of AWS, Snowflake, Adobe etc

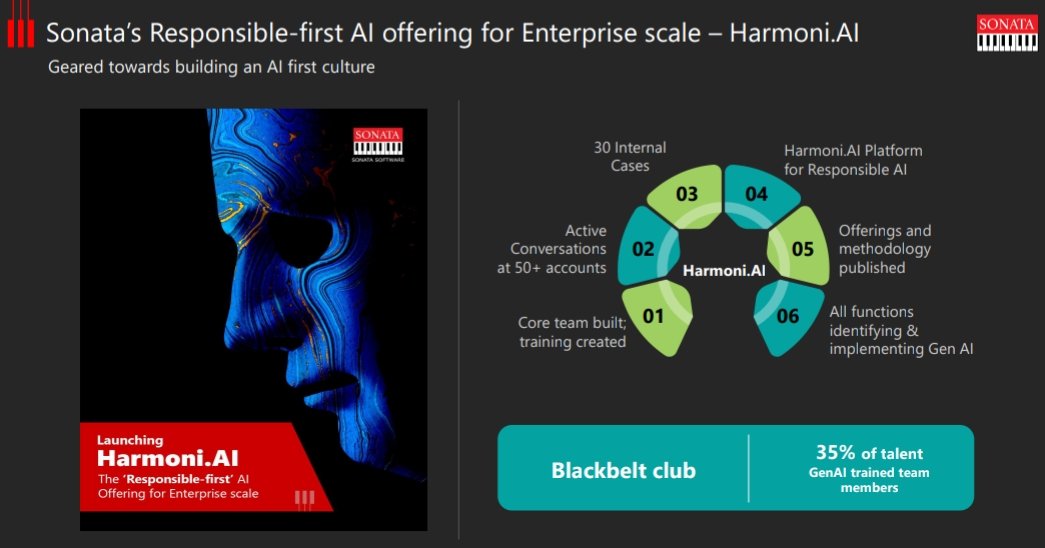

3. Harmoni AI Vertical

-Adopted as service offering & delivery platform (a white space in AI) & not competing with Google or Microsoft

1. Rise in contribution of high margin IITS Vertical

2. Reputed Partnership network, which consists of AWS, Snowflake, Adobe etc

3. Harmoni AI Vertical

-Adopted as service offering & delivery platform (a white space in AI) & not competing with Google or Microsoft

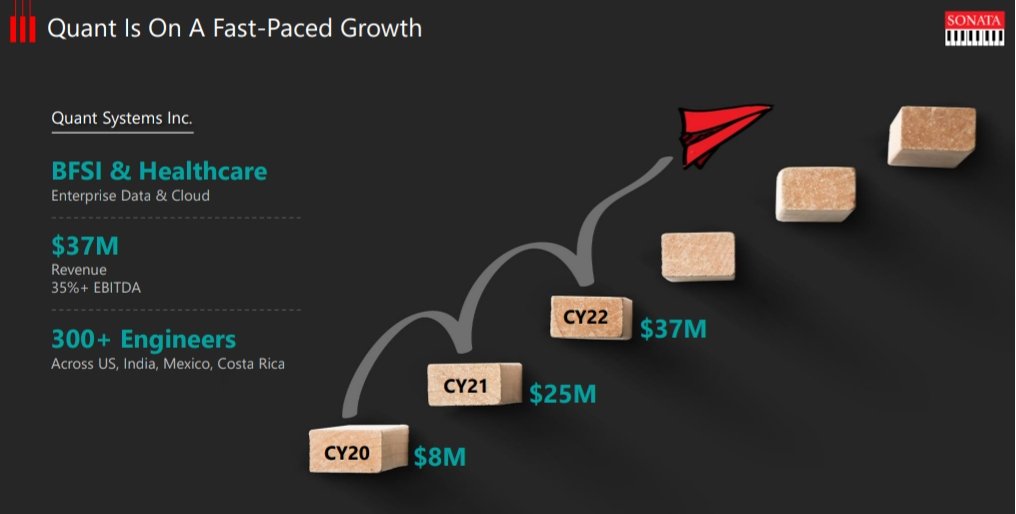

4. High Margin Quant Acquisition

-Quant has higher margin compared to Sonata

-It works in different verticals like Data analytics, Cyber security, cloud monetization & Data privacy

-Had partnership with major tech co. like Adobe, Mulesoft, Collibra etc

-Has differentiate IPs

-Quant has higher margin compared to Sonata

-It works in different verticals like Data analytics, Cyber security, cloud monetization & Data privacy

-Had partnership with major tech co. like Adobe, Mulesoft, Collibra etc

-Has differentiate IPs

5. Growth in BFS & Healthcare Vertical, this vertical is newly focused for Sonata which would cater through Quant Acquisition

(Sonata is not in such vertical earlier)

6. Expanding Digital & modernization solutions & Expanding other offerings of Microsoft like Data, Cloud & AI

(Sonata is not in such vertical earlier)

6. Expanding Digital & modernization solutions & Expanding other offerings of Microsoft like Data, Cloud & AI

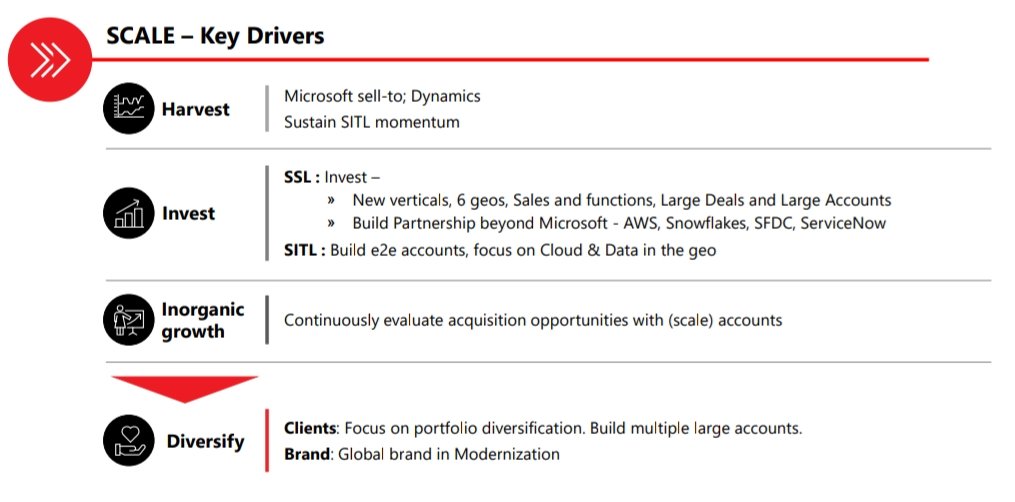

7. Restructuring in US Organisation for better alignment & Investing in Sales & Marketing for better client mining(Recently sponsored MIW team)

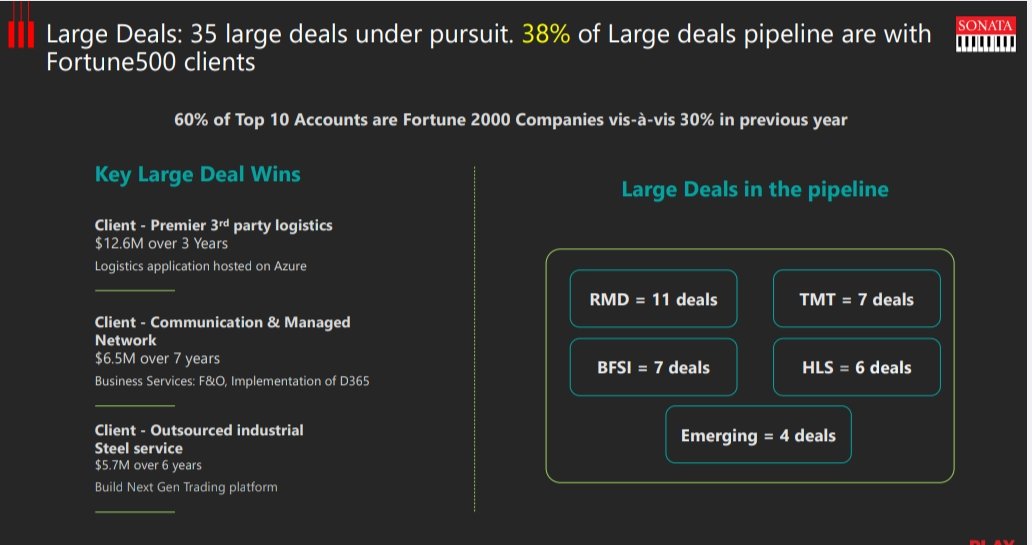

8. Large Deal Pipeline executions: Cloud & Data pipeline is 38% + 10 Large Deal win YTD

9. Geographical Exp. by entering new countrie

8. Large Deal Pipeline executions: Cloud & Data pipeline is 38% + 10 Large Deal win YTD

9. Geographical Exp. by entering new countrie

10. Investing in other Vertical through Cash Rich & High ROCE DPS Biz

11. Operating Leverage play(Currently playing out) which is leading to EBITDA Margin improvement

12. Inorganic Acquisition(Had a good past record of Acquisition)

13. Microsoft Strong Innovative Partnership

11. Operating Leverage play(Currently playing out) which is leading to EBITDA Margin improvement

12. Inorganic Acquisition(Had a good past record of Acquisition)

13. Microsoft Strong Innovative Partnership

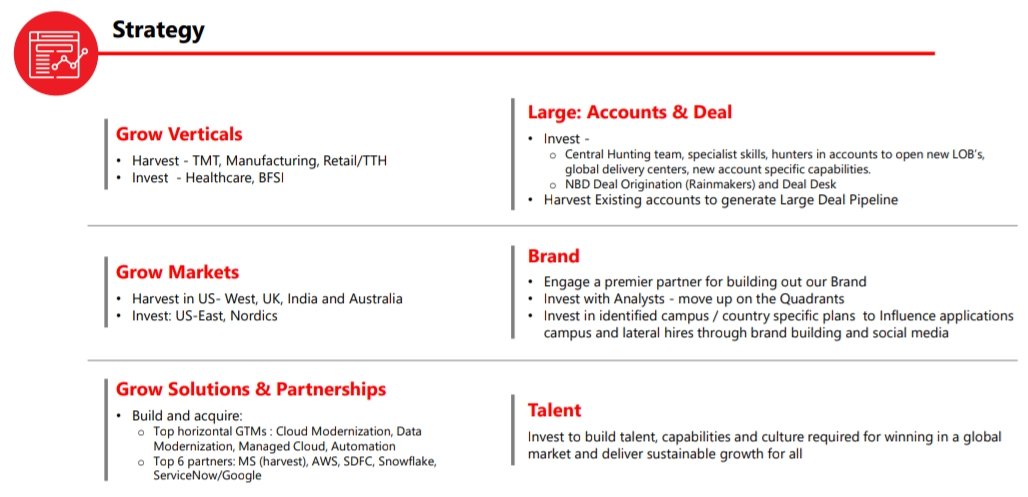

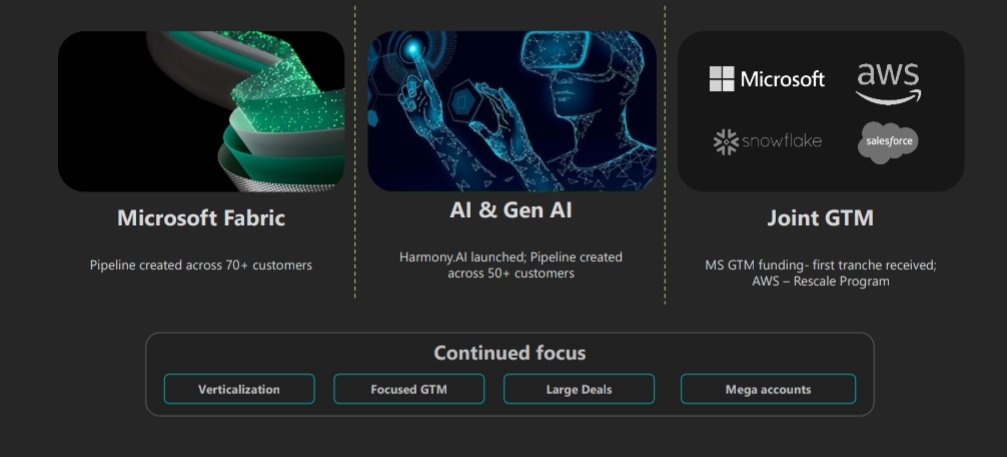

14. Key Future Bets like:

1. Microsoft Fabric

-Sonata is only Microsoft partner in Microsoft Fabric

2. AI & Gen AI

3. Joint Go to market software (Resale partner products with scale & new strategy)

15. Product Mix (From high DPS to IITS) improvement lead to margin Expansion

1. Microsoft Fabric

-Sonata is only Microsoft partner in Microsoft Fabric

2. AI & Gen AI

3. Joint Go to market software (Resale partner products with scale & new strategy)

15. Product Mix (From high DPS to IITS) improvement lead to margin Expansion

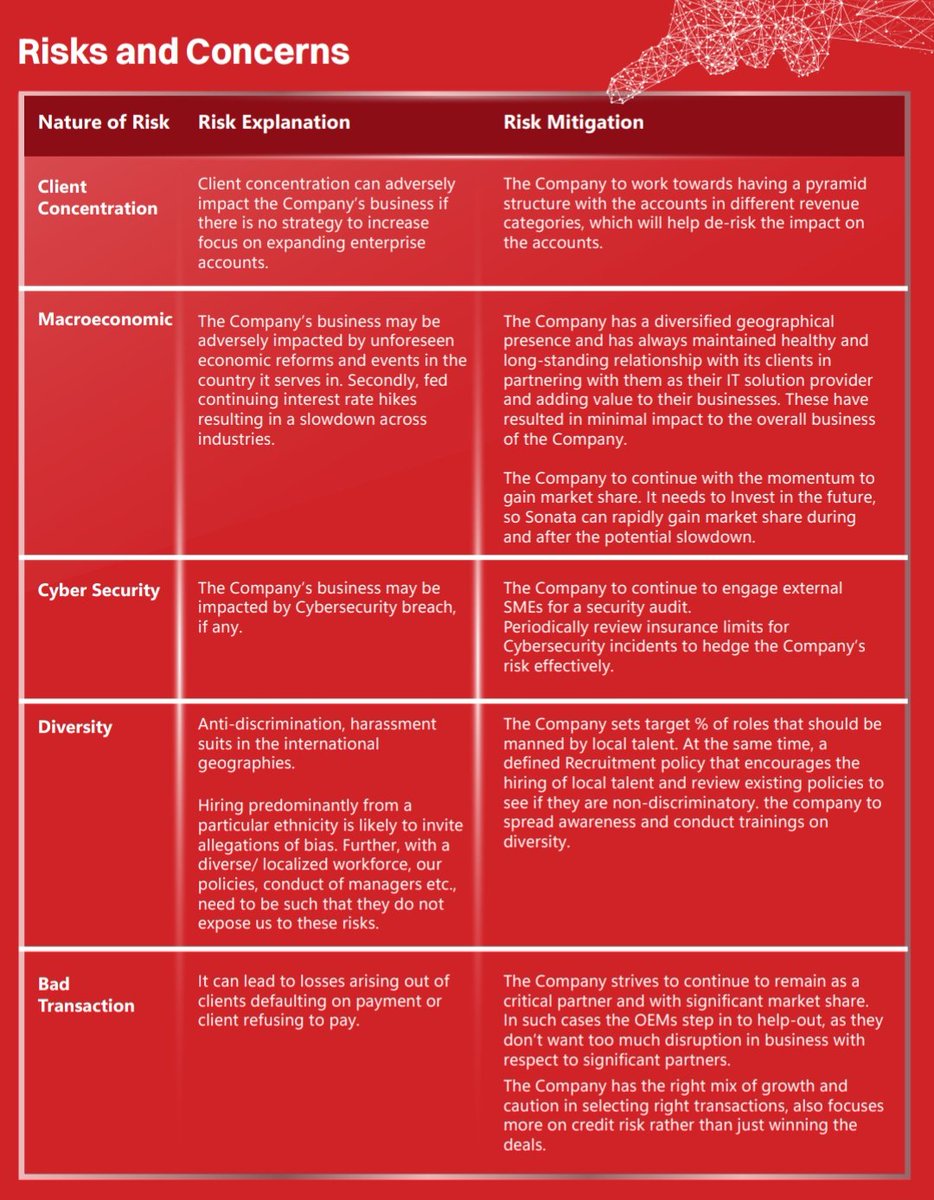

Risk:

-Dollar Revenue loss if INR Appreciate

-Pricing pressure in DPS Vertical

-Cyber security Risk

-Any large debt fund acquisition, which can hamper Profits

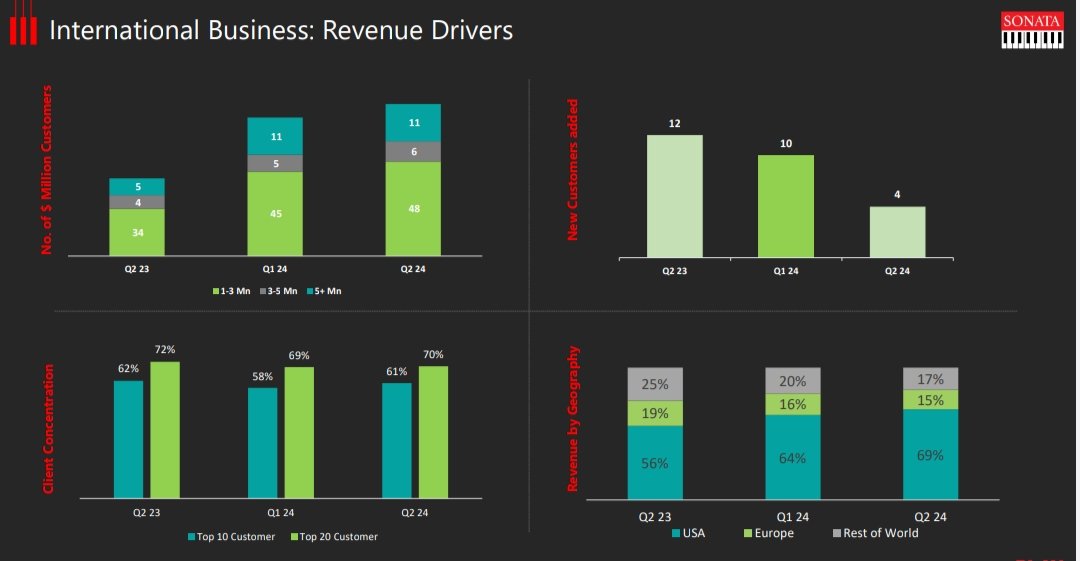

-High geographical/Client concentration

-Key customer loss risk

-Near term margin headwinds, due to Quant Acquisition v

-Dollar Revenue loss if INR Appreciate

-Pricing pressure in DPS Vertical

-Cyber security Risk

-Any large debt fund acquisition, which can hamper Profits

-High geographical/Client concentration

-Key customer loss risk

-Near term margin headwinds, due to Quant Acquisition v

Valuations:

Current PE: 36x

3 Yr Median PE: 25x

EV/EBITDA: 22x

3 Yr Median EV/EBITDA: 15x

Trading at overvaluation territory compared to 3 Yr Avg. But Sonata strategy has been changed & now it is moving to become its Biz more structural & consistent compared to earlier

Current PE: 36x

3 Yr Median PE: 25x

EV/EBITDA: 22x

3 Yr Median EV/EBITDA: 15x

Trading at overvaluation territory compared to 3 Yr Avg. But Sonata strategy has been changed & now it is moving to become its Biz more structural & consistent compared to earlier

Guidance:

-Revenue Guidance of $1.5 BN by FY26

-Internation EBITDA will be in low 20s & Aim to have 50% Revenue contribution from IITS vertical

- Significant investment in Harmoni.AI platform, with a goal to have 25% of topline contribution from it in next 2-3 Yrs

-Revenue Guidance of $1.5 BN by FY26

-Internation EBITDA will be in low 20s & Aim to have 50% Revenue contribution from IITS vertical

- Significant investment in Harmoni.AI platform, with a goal to have 25% of topline contribution from it in next 2-3 Yrs

#Technical Analysis:

1. Point & Finger Chart

2. 3% x 3 Point & Finger Chart

3. Moving Avg. Observation

4. RSI Observation

5. Donchian Channel Observation

6. Bollinger Band Observation

7. Ichimoku Observation

1. Point & Finger Chart

2. 3% x 3 Point & Finger Chart

3. Moving Avg. Observation

4. RSI Observation

5. Donchian Channel Observation

6. Bollinger Band Observation

7. Ichimoku Observation

1. Strong purchasing interest & support is expected to continue the previous long "X" anchor column & stock will probably issue a Bear Trap Follow Through confirmation signal & will also continue to trade above the 10SMA, indicating its bullish momentum & potential for more gains

2. Stock is quite strong, shown in chart Anchor Follow through pattern is formed by the current trendline B/O & DTB at 1205, which is configured to prolong the previous long "X" anchor column also significant activity in this lengthy "X" column, indicating strong bullish momentum

3. Moving Average Observations:

The 200-day moving average is still above the price.

Price above moving averages of 50, 100, and 200 days.

Alignment of the moving average is positive. It's a bullish situation with an upswing.

The 200-day moving average is still above the price.

Price above moving averages of 50, 100, and 200 days.

Alignment of the moving average is positive. It's a bullish situation with an upswing.

4. The Daily RSI indicator has continued to be above 60. This area is bullish. The Daily RSI is currently reading 69.93.

-The Weekly RSI has stayed over 70. The Weekly RSI is at 75.08.

-In the current session, the Monthly RSI indicator crossed over 80. The monthly RSI is at 87.44

-The Weekly RSI has stayed over 70. The Weekly RSI is at 75.08.

-In the current session, the Monthly RSI indicator crossed over 80. The monthly RSI is at 87.44

5. Donchian Channel Observations:

-Price is above the middle of the Donchian channel (Bullish).

-Difference between bands is 20.33%

6. Bollinger Band Observations:

-Price is above Uper band Bollinger band (Bullish to over-brought)

Difference between bands is 20.32%

-Price is above the middle of the Donchian channel (Bullish).

-Difference between bands is 20.33%

6. Bollinger Band Observations:

-Price is above Uper band Bollinger band (Bullish to over-brought)

Difference between bands is 20.32%

7. Ichimoku Observations:

-Price above Ichimoku clouds.

-Clouds are bullish.

-Tenkan line is above Kijun line. Ichimoku setup is bullish.

-Price above Ichimoku clouds.

-Clouds are bullish.

-Tenkan line is above Kijun line. Ichimoku setup is bullish.

No Recommendation

This post is purely for #educational purposes

Hope, you guys will like it!! ✨

For more such detailed Techno-Funda Analysis follow:

@Mr_Maurya16 & @BansalSwapan

This post is purely for #educational purposes

Hope, you guys will like it!! ✨

For more such detailed Techno-Funda Analysis follow:

@Mr_Maurya16 & @BansalSwapan

Loading suggestions...