Third-Largest Broker in #India: Angel One Techno-Funda Analysis

#Fundamentals by @BansalSwapan

#Technicals by @Mr_Maurya16

Market Cap ~ 18,750 Cr

CMP ~ 2,235

PE ~ 18.4x

1 Yr Return ~ 40%

Let's deep dive into it 👇

#Fundamentals by @BansalSwapan

#Technicals by @Mr_Maurya16

Market Cap ~ 18,750 Cr

CMP ~ 2,235

PE ~ 18.4x

1 Yr Return ~ 40%

Let's deep dive into it 👇

Technical analysis.

1.Point-and-Figure (P&F) Chart

2.Candlestick chart

1.Point-and-Figure (P&F) Chart

2.Candlestick chart

The 1% x 3 Point and Figure chart highlights the stock's considerable strength. The current DTB ( double top buy ) at 2517 is set to extend the

prior lengthy "X" anchor column & maintaining its position above the 10SMA and B/O of consolidation phase

prior lengthy "X" anchor column & maintaining its position above the 10SMA and B/O of consolidation phase

2.#Candlestick chart

The stock is now trading at its ATH. The long-term moving average (200EMA) and the short-term moving average (50EMA) have recently crossed above each other, creating a golden cross on the chart that indicates the continuation of the bullish trend.

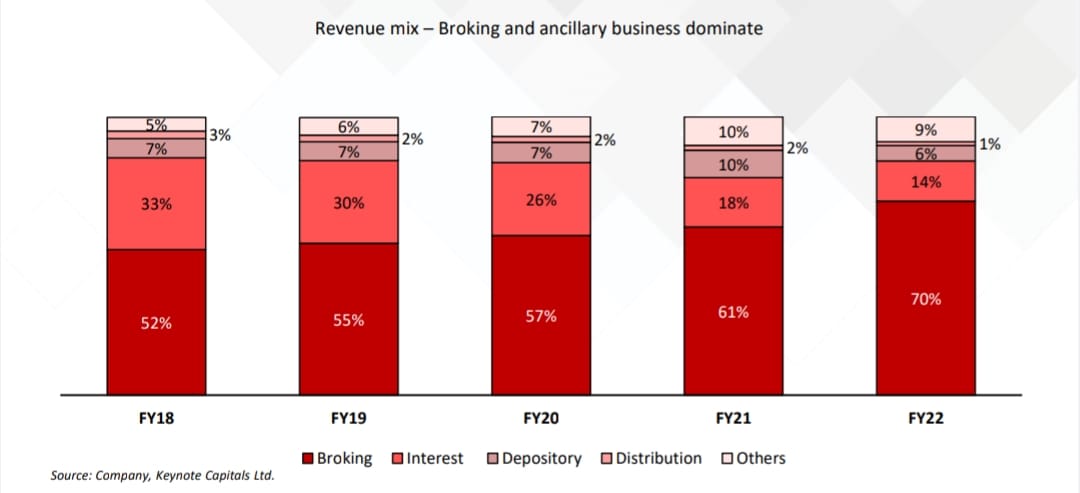

Fundamental analysis:

Business Overview:

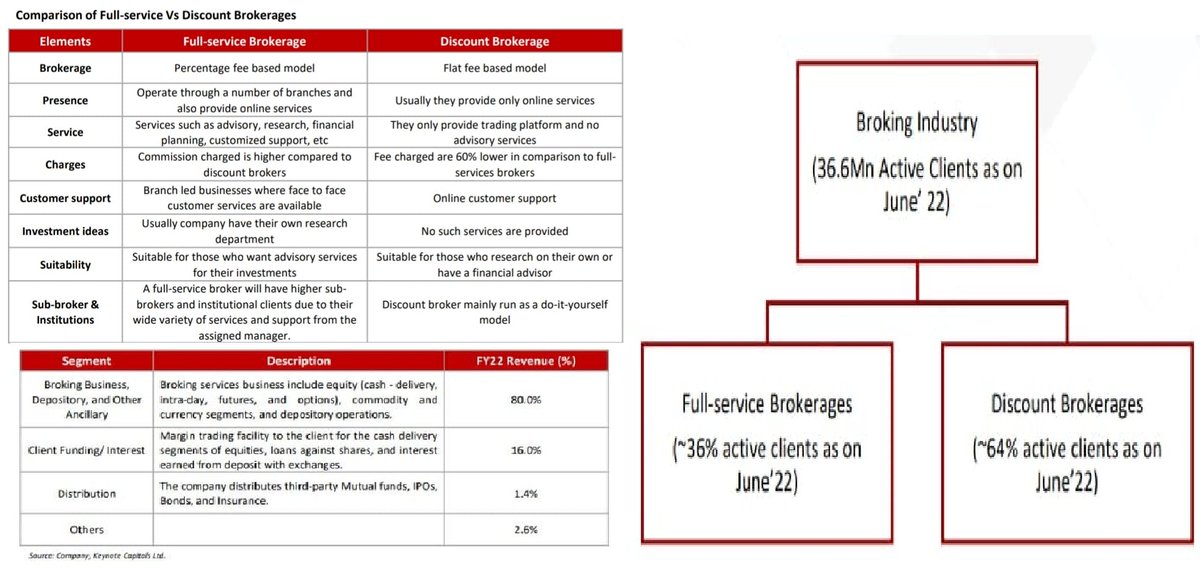

Started in 1996 as a #traditional stock #brokerage firm. Formally known as 'Angel Broking'. Operate in three segments i.e. broking & advisory, client funding & distribution. An all in one financial house with 10M+ Registered clients

Business Overview:

Started in 1996 as a #traditional stock #brokerage firm. Formally known as 'Angel Broking'. Operate in three segments i.e. broking & advisory, client funding & distribution. An all in one financial house with 10M+ Registered clients

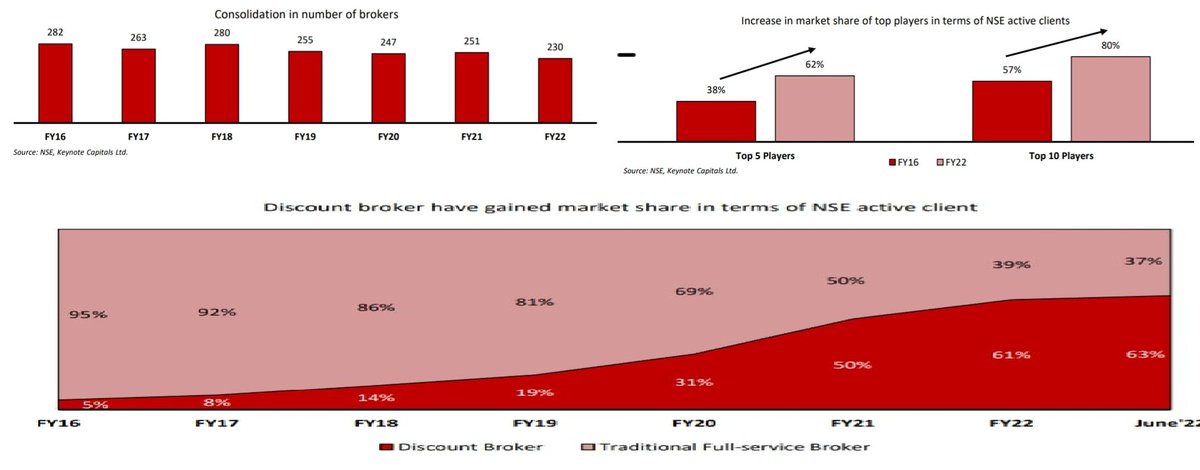

Industry trends:

1. Discount Broker gaining share from traditional brokers

2. Consolidation in Industry with top brokers gaining market share

1. Discount Broker gaining share from traditional brokers

2. Consolidation in Industry with top brokers gaining market share

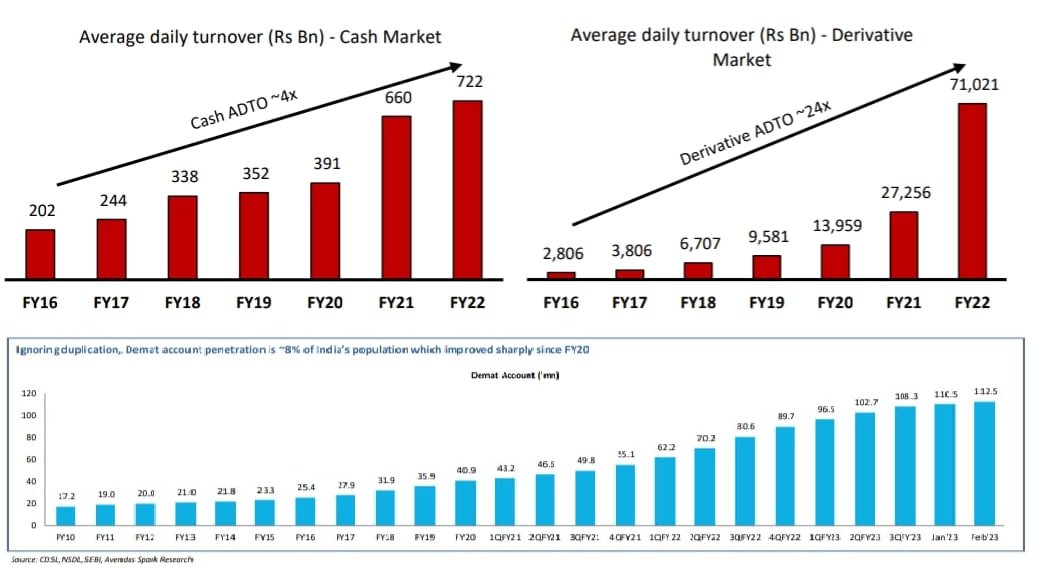

3. Robust client addition after COVID

4. Surge in Average Daily Turnover

4. Surge in Average Daily Turnover

Transformation to 'Angel one' from 'Angel Broking'

Turned from a branch type Biz model to complete digitisation model

Traditional models are high margin but low client addition Biz whereas Flat fee (discount broker) model is slight low margin but high client addition verticle

Turned from a branch type Biz model to complete digitisation model

Traditional models are high margin but low client addition Biz whereas Flat fee (discount broker) model is slight low margin but high client addition verticle

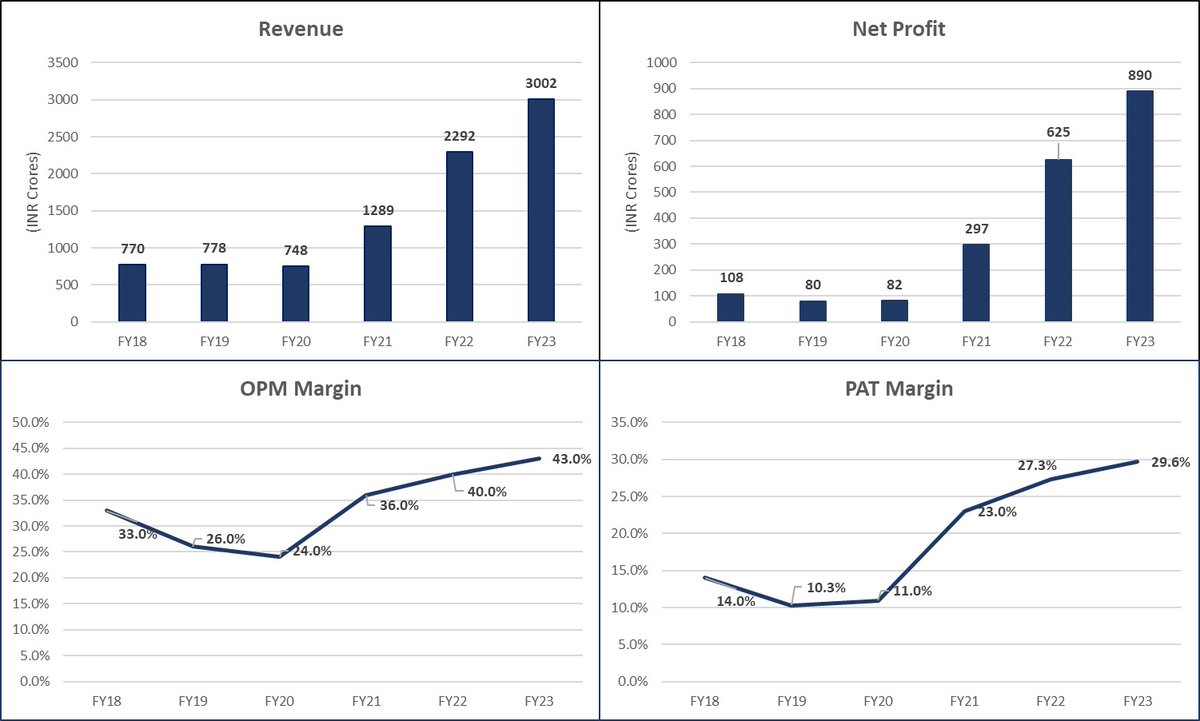

Financial analysis:

-#Sales has been grown at a CAGR of 31% in last 5 years (Industry tailwinds + move to flat fee model)

-PAT has been grown at a CAGR of 52% in last 5 years

-OPM expanded to 43% from 33% in FY18 (Growth of Brokerage arm verticle + Operating Lvg)

-#Sales has been grown at a CAGR of 31% in last 5 years (Industry tailwinds + move to flat fee model)

-PAT has been grown at a CAGR of 52% in last 5 years

-OPM expanded to 43% from 33% in FY18 (Growth of Brokerage arm verticle + Operating Lvg)

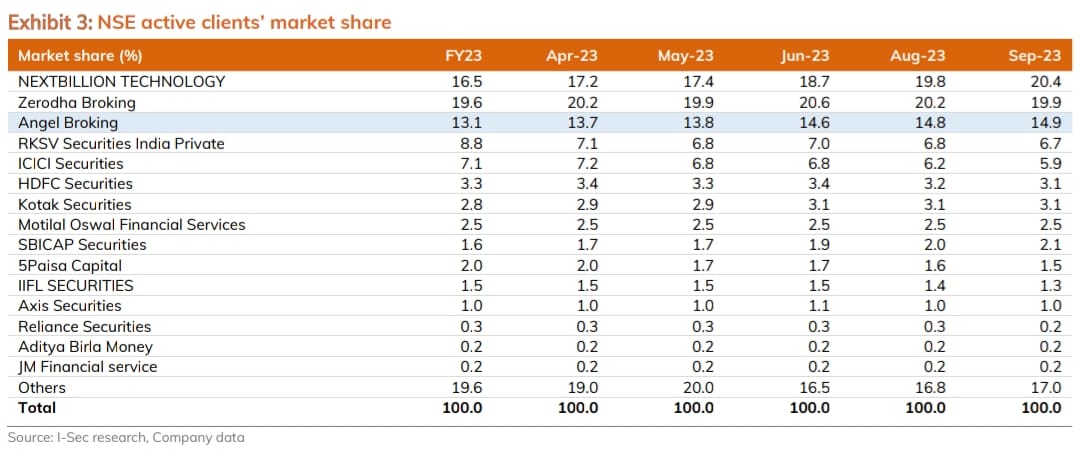

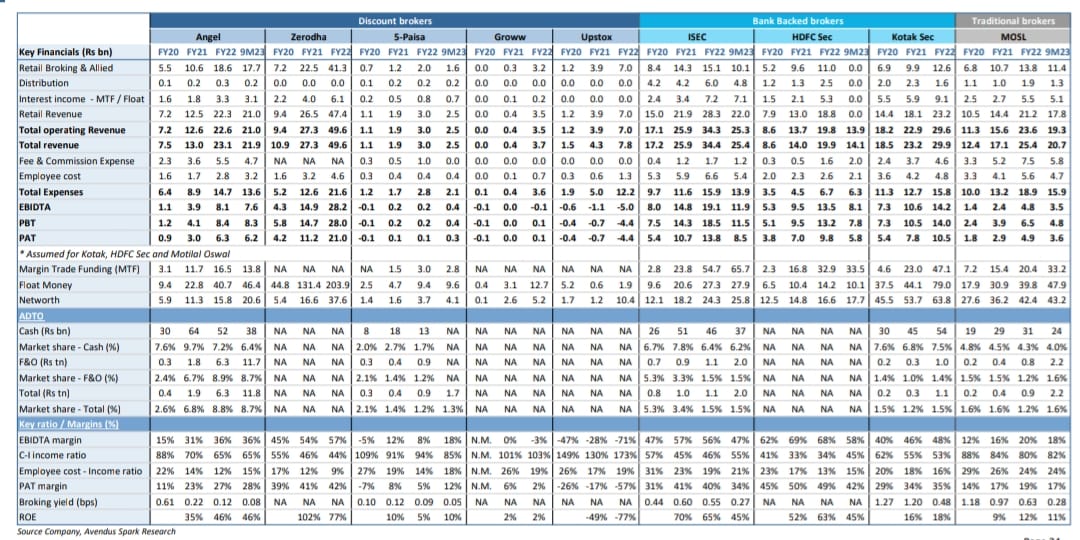

Peer Comparison:

-Whole Broking Sector is in tailwinds led by favourable Industry Trends

-Continues gain in Market share by Angel from other players led by innovative offerings at a low cost

-Whole Broking Sector is in tailwinds led by favourable Industry Trends

-Continues gain in Market share by Angel from other players led by innovative offerings at a low cost

Opportunities/Growth Drivers:

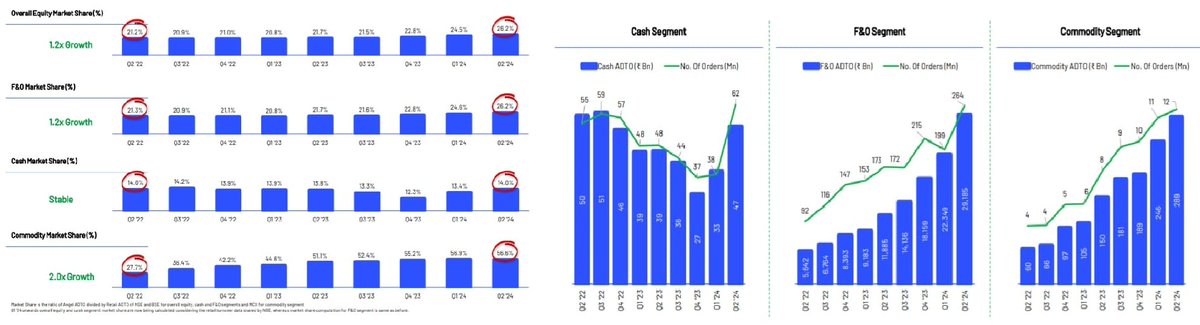

1. Rise in High margin/Revenue F&O share in total mix

-Rises from 23% in Q1FY22 to 26.2% in Q2FY24

2. Continues Gaining Market share from other players in all segments

1. Rise in High margin/Revenue F&O share in total mix

-Rises from 23% in Q1FY22 to 26.2% in Q2FY24

2. Continues Gaining Market share from other players in all segments

3. Continues rise in order volume + Client Active Base (Key Revenue & Growth Drivers)

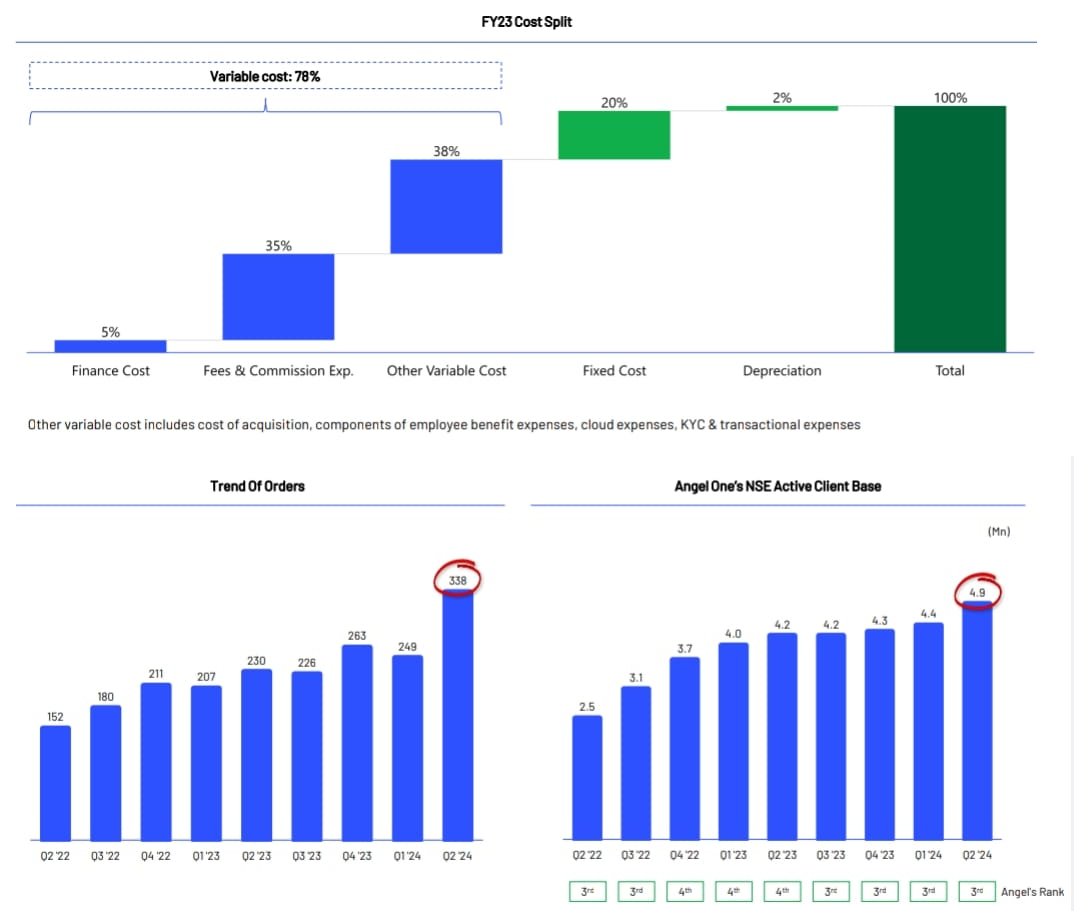

4. High Variable cost structure, which provides cost levers to protect margins

Fixed cost includes Employee & Advertising, which are continuously falling as a % of sales, led to margin ⬆️

4. High Variable cost structure, which provides cost levers to protect margins

Fixed cost includes Employee & Advertising, which are continuously falling as a % of sales, led to margin ⬆️

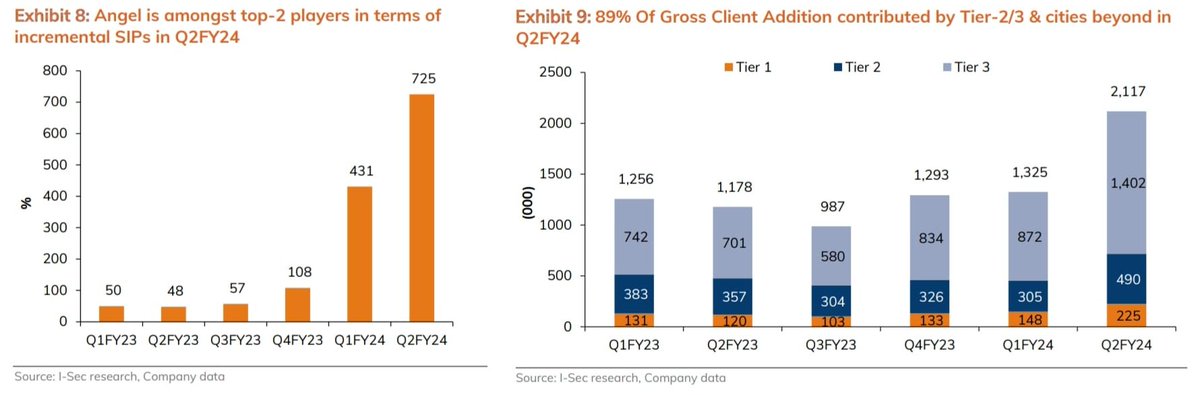

5. High Penetration in Tier 2 & Tier 3 cities without any branch network

6. Top 2 players in terms of incremental SIPs in Q2FY24

6. Top 2 players in terms of incremental SIPs in Q2FY24

7. Industry trends led growth

-Rising smartphone penetration

-Young Educated clients knowing importance of financial independence led to Growth in DEMAT & Client base + Avg. Turnover

-Increase in Mutual funds Penetration

8. Developing Super App & further innovation for offering

-Rising smartphone penetration

-Young Educated clients knowing importance of financial independence led to Growth in DEMAT & Client base + Avg. Turnover

-Increase in Mutual funds Penetration

8. Developing Super App & further innovation for offering

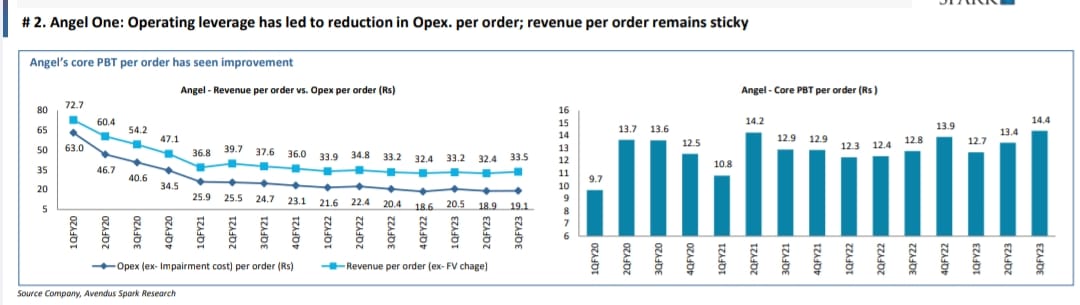

9. Operating Leverage play

-Cost per order reducing

-Net brokerage realisation improves with higher share of direct clients

10. Experienced & Top grade management

-Cost per order reducing

-Net brokerage realisation improves with higher share of direct clients

10. Experienced & Top grade management

Risks:

1. Highly Cyclical Industry with client addition depends upon Market sentiments (Poor sentiments fall in client addition & Vice versa)

2. IT/Software Disruption (led to loss to clients, which need to be compensated)

3. Only the broker arm is firing & rest are Laggard

1. Highly Cyclical Industry with client addition depends upon Market sentiments (Poor sentiments fall in client addition & Vice versa)

2. IT/Software Disruption (led to loss to clients, which need to be compensated)

3. Only the broker arm is firing & rest are Laggard

Valuations:

Trading at a PE of 18x

Median 3 year PE is of 20x

Peers like:

ISec trades at a PE of 17x

Industry is highly cyclical with regulator holding the key role

With things like Industry Trend, Growth & Risk in consideration Angel might be trading at fair to exp. Side

Trading at a PE of 18x

Median 3 year PE is of 20x

Peers like:

ISec trades at a PE of 17x

Industry is highly cyclical with regulator holding the key role

With things like Industry Trend, Growth & Risk in consideration Angel might be trading at fair to exp. Side

Note : No Recommendation

This post is for #educational purposes

For more such analysis follow:

@Mr_Maurya16 & @BansalSwapan

This post is for #educational purposes

For more such analysis follow:

@Mr_Maurya16 & @BansalSwapan

جاري تحميل الاقتراحات...