The arbitrage thread.

How kings are made.

How kings are made.

Arbitrage is the trading of mispriced things

Ex:

Imagine you buy pencils from Jim in Math class for $0.10

However, you can sell them to Frank in English class for $0.15

By buying from Jim and selling to Frank, you're arbitraging the price inefficiency between the two classes.

Ex:

Imagine you buy pencils from Jim in Math class for $0.10

However, you can sell them to Frank in English class for $0.15

By buying from Jim and selling to Frank, you're arbitraging the price inefficiency between the two classes.

But many things that aren't items can be mispriced:

• Interest Rates

• Derivatives

• Fees

• Funding Rates

• Yields

And if you can spot these price inefficiencies, you can often generate outsized returns with minimal risk.

• Interest Rates

• Derivatives

• Fees

• Funding Rates

• Yields

And if you can spot these price inefficiencies, you can often generate outsized returns with minimal risk.

Peg Arbitrage

When an asset trades at less then its backed value, there's almost always an arbitrage opportunity.

stETH: 8% ROI in 90 days

ETH2: 50% ROI in 81 days

BNBx: 1,000% ROI in 1 day

cbETH: 9% ROI in 130 days

crETH2: 46% in 19 days

When an asset trades at less then its backed value, there's almost always an arbitrage opportunity.

stETH: 8% ROI in 90 days

ETH2: 50% ROI in 81 days

BNBx: 1,000% ROI in 1 day

cbETH: 9% ROI in 130 days

crETH2: 46% in 19 days

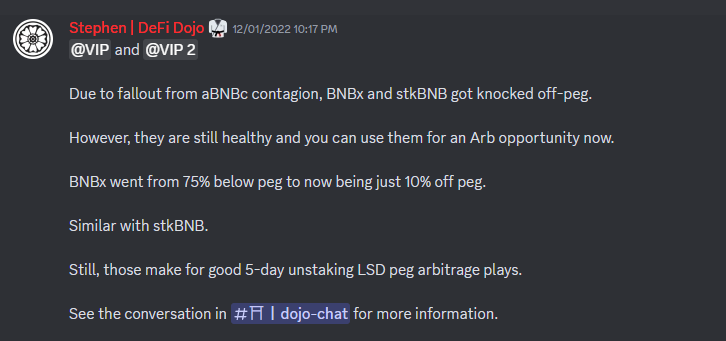

Peg Arbitrage: Case Study, BNBx

When aBNBc was exploited, millions of aBNBc were minted and ankrBNB LPs were drained.

BNBx down to 0.1 WBNB because of a 3pool both aBNBc and BNBx were in.

However, BNBx was still fully backed, verifiable on-chain.

Those who noticed did well.

When aBNBc was exploited, millions of aBNBc were minted and ankrBNB LPs were drained.

BNBx down to 0.1 WBNB because of a 3pool both aBNBc and BNBx were in.

However, BNBx was still fully backed, verifiable on-chain.

Those who noticed did well.

Interest Rate Arb #1: Delta Neutral

When an asset's yield exceeds its cost to borrow, you can arb the difference.

Ex:

Cost to borrow ATOM: 9%

Staking yield of ATOM: 20%

1. Collateralize USDC

2. Borrow ATOM

3. Stake ATOM

Profit APR = (Staking Yield - Borrow Rate) * LTV

When an asset's yield exceeds its cost to borrow, you can arb the difference.

Ex:

Cost to borrow ATOM: 9%

Staking yield of ATOM: 20%

1. Collateralize USDC

2. Borrow ATOM

3. Stake ATOM

Profit APR = (Staking Yield - Borrow Rate) * LTV

Interest Rate Arb #2: Leveraged Lending

When an interest-bearing derivative of an asset (like wstETH) can be used as collateral and the yield of that asset exceeds the borrow cost of the underlying asset (ETH), you can arbitrage the difference between those rates with leverage.

When an interest-bearing derivative of an asset (like wstETH) can be used as collateral and the yield of that asset exceeds the borrow cost of the underlying asset (ETH), you can arbitrage the difference between those rates with leverage.

Leveraged Lending: Case Study

wstETH yield: 4%

ETH borrow cost (@MorphoLabs): 3.1%

Max LTV: 90%

Max Leverage: 1/(1-Max LTV)

Max Leverage = 1/(1-0.9) = 10

The yield is the difference between the rates multiplied by the leverage.

0.9% * 10 = 9% on ETH, 125% increase in yield

wstETH yield: 4%

ETH borrow cost (@MorphoLabs): 3.1%

Max LTV: 90%

Max Leverage: 1/(1-Max LTV)

Max Leverage = 1/(1-0.9) = 10

The yield is the difference between the rates multiplied by the leverage.

0.9% * 10 = 9% on ETH, 125% increase in yield

Funding Rate Arbitrage: Cash-and-Carry

When the funding rate of an asset is negative, you can arbitrage the cost to hold the asset and the return to short the asset.

Ex

Buy ATOM Spot (cost to hold: 0%)

Short ATOM on @dYdX (funding: 20%)

Delta Neutral Yield: 10% (no leverage)

When the funding rate of an asset is negative, you can arbitrage the cost to hold the asset and the return to short the asset.

Ex

Buy ATOM Spot (cost to hold: 0%)

Short ATOM on @dYdX (funding: 20%)

Delta Neutral Yield: 10% (no leverage)

Funding Rate Arbitrage: Double Funding

Sometimes funding will be positive on one platform and negative on another. You can arbitrage this difference as well.

Short ATOM on DyDx for 20%

Long ATOM on HperLiquid for 18%

Total Yield: 19%, Delta Neutral

Sometimes funding will be positive on one platform and negative on another. You can arbitrage this difference as well.

Short ATOM on DyDx for 20%

Long ATOM on HperLiquid for 18%

Total Yield: 19%, Delta Neutral

You can also combine arbitrage strategies.

For example, the staking yield of ATOM is 20%, and the funding rate for ATOM on DyDx is 20%.

Therefore, you can stake your long exposure to ATOM for 20% to get a delta neutral yield of 20% (without leverage).

For example, the staking yield of ATOM is 20%, and the funding rate for ATOM on DyDx is 20%.

Therefore, you can stake your long exposure to ATOM for 20% to get a delta neutral yield of 20% (without leverage).

But why stop there? Let's combine even more strategies.

• Leveraged Lending

• Funding Rate

• Peg Arbitrage

Mega case study: cbETH👇

• Leveraged Lending

• Funding Rate

• Peg Arbitrage

Mega case study: cbETH👇

Conditions:

cbETH 3% under peg

cbETH as collateral on Aave V3 e-Mode (90% LTV)

cbETH Yield: 4%

ETH Borrow 3%

ETH Funding Rate: 10%

Strategy:

1. Long X cbETH

2. Short cbETH backing value in ETH

3. Borrow ETH & Convert to cbETH

4. Add cbETH as collateral

5. Repeat from step 3

cbETH 3% under peg

cbETH as collateral on Aave V3 e-Mode (90% LTV)

cbETH Yield: 4%

ETH Borrow 3%

ETH Funding Rate: 10%

Strategy:

1. Long X cbETH

2. Short cbETH backing value in ETH

3. Borrow ETH & Convert to cbETH

4. Add cbETH as collateral

5. Repeat from step 3

Outcome:

10x leverage long on the repeg (30% ROI)

10x leverage borrow rate difference (10% APR)

10% APR on short

Assuming 3-month repeg: 70%APY Delta Neutral

10x leverage long on the repeg (30% ROI)

10x leverage borrow rate difference (10% APR)

10% APR on short

Assuming 3-month repeg: 70%APY Delta Neutral

You can also do fixed rate interest yields on things like @pendle_fi and @Flashstake.

But I've already talked about that before:

But I've already talked about that before:

These are some of the most profitable, risk-adjusted plays in DeFi.

Arbitrage also makes markets more efficient, being value-additive to the space long-term.

If you want to stay on top of arb opportunities, join the DeFi Dojo. We'll be waiting for you.

whop.com

Arbitrage also makes markets more efficient, being value-additive to the space long-term.

If you want to stay on top of arb opportunities, join the DeFi Dojo. We'll be waiting for you.

whop.com

If you liked this thread and/or found it valuable, please consider retweeting.

Loading suggestions...