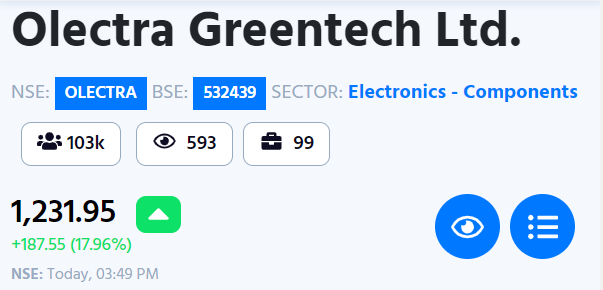

A ₹10,000 crore mcap company, secured a massive order for 5,150 electric buses worth over ₹10,000 crores, driving the stock up by over 17%. 📈

Join us in this 🧵 as we analyze Olectra Greentech's future prospects. 🔎

Grab a coffee ☕ and stick around!

#OlectraGreentech #Quest

Join us in this 🧵 as we analyze Olectra Greentech's future prospects. 🔎

Grab a coffee ☕ and stick around!

#OlectraGreentech #Quest

With over 1,188 electric buses hitting Indian roads, this company is revolutionizing the EV bus industry!

We can see the products of the company in the image.

But first, let's try to understand this booming sector. ⤵️

#EV #ElectricBuses

We can see the products of the company in the image.

But first, let's try to understand this booming sector. ⤵️

#EV #ElectricBuses

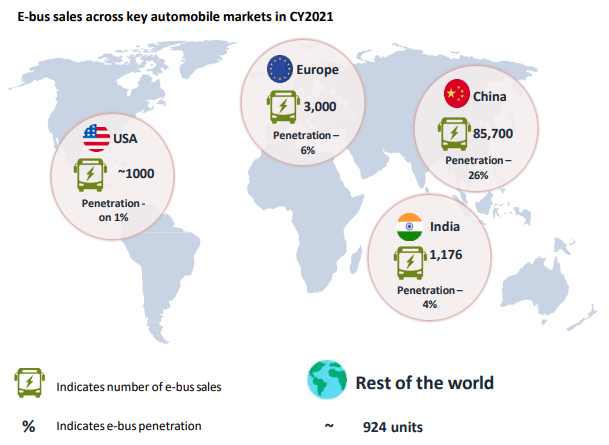

Check out the image showing E-bus sales in major automobile markets during CY2021.

Except for China, global penetration in the E-bus segment remains below 10%.

India, the USA, and Europe have a great opportunity to catch up!

Except for China, global penetration in the E-bus segment remains below 10%.

India, the USA, and Europe have a great opportunity to catch up!

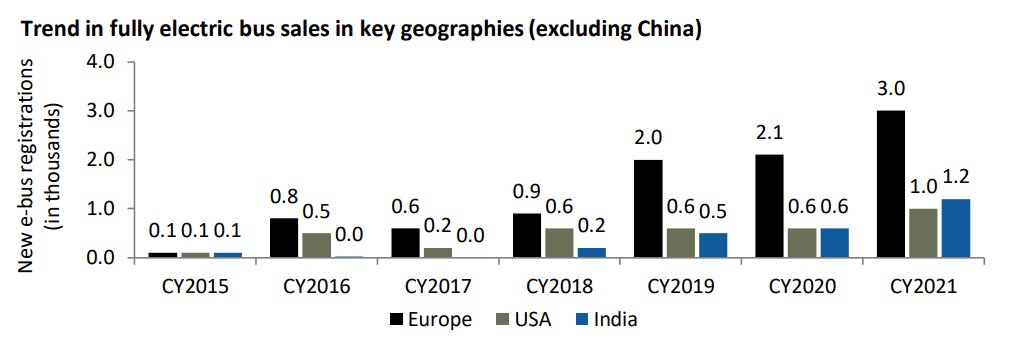

Historical data reveals a promising trend: the penetration of e-buses is on the rise in Europe and India.

As the world prioritizes sustainability, the transition to electric buses gains momentum.

As the world prioritizes sustainability, the transition to electric buses gains momentum.

India's PLI Scheme aims to allocate a total of US$20 billion, including US$2.5 billion specifically for batteries.

These incentives will attract more players and foster the growth of the low-emission vehicle ecosystem.

Also...

These incentives will attract more players and foster the growth of the low-emission vehicle ecosystem.

Also...

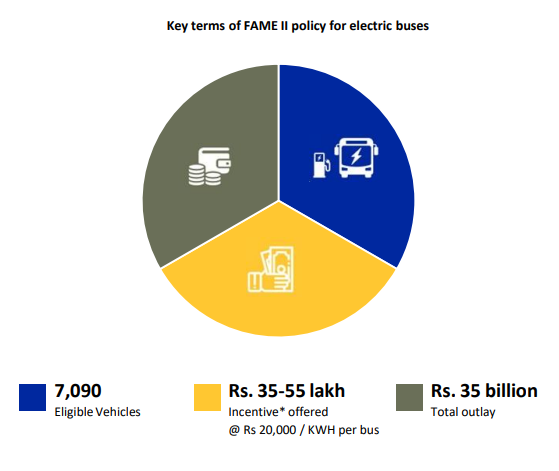

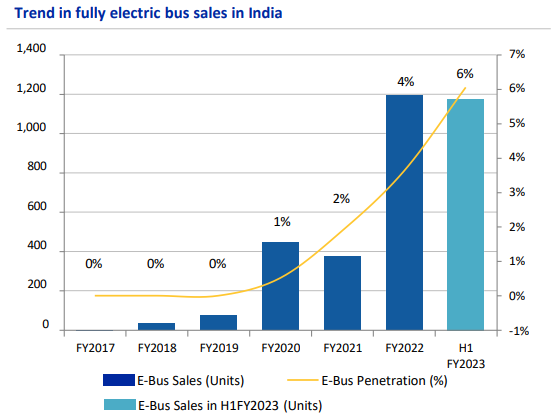

The allocation of significant capital under FAME II is driving e-bus adoption in India.

The penetration of e-buses has seen remarkable growth, increasing from 1% in FY20 to 4% in FY22, and further to 6% as of H1FY23.

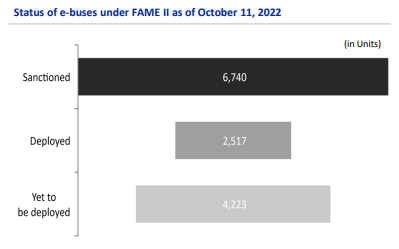

Till October 22, you can see how e-buses are doing under FAME II. Out of which,

🚌 Intra-city operations: Over 90% of tenders awarded.

🚌 9-meter buses: 80% tenders awarded.

And, Olectra earns significant revenue from these categories.

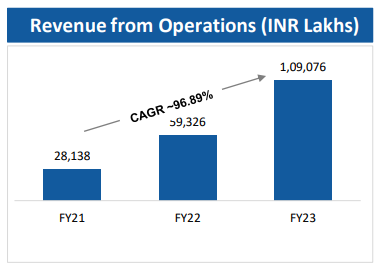

If we talk about financials of Olectra,

🚌 Intra-city operations: Over 90% of tenders awarded.

🚌 9-meter buses: 80% tenders awarded.

And, Olectra earns significant revenue from these categories.

If we talk about financials of Olectra,

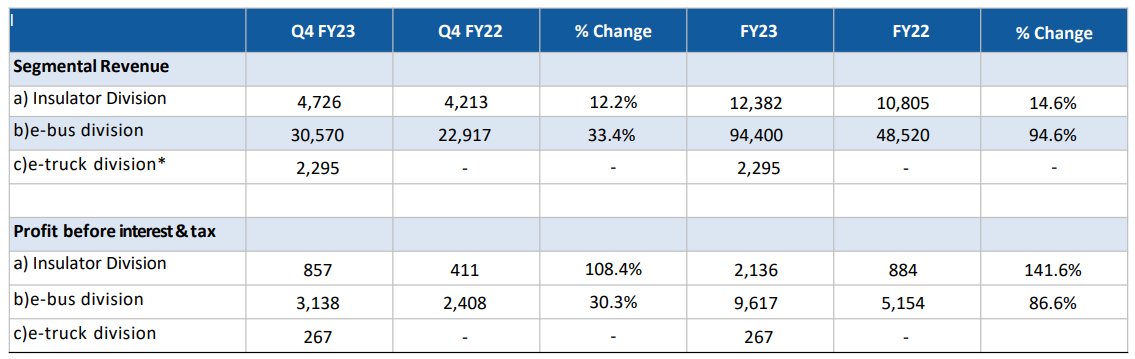

The company has witnessed a remarkable growth in revenue, with a CAGR of 96.89% from FY21 to FY23.

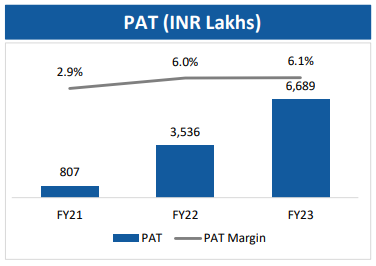

When it comes to PAT, the company recorded a profit of ₹8 crores in FY21, which has now increased to approximately ₹67 crores.

The profit margin has expanded from 2.9% to 6.1%.

When it comes to PAT, the company recorded a profit of ₹8 crores in FY21, which has now increased to approximately ₹67 crores.

The profit margin has expanded from 2.9% to 6.1%.

Check out the image showcasing the company's growing unit sales and the YOY change in its e-bus division and other divisions.

Looks like a promising future right? 🤔

But...

Looks like a promising future right? 🤔

But...

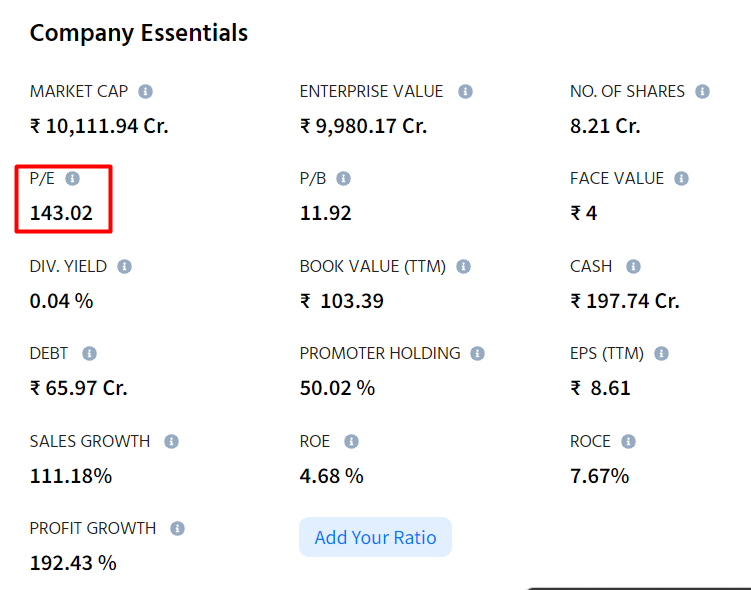

The company's current PE ratio stands at approximately 150, indicating a very premium valuation.

The question arises whether the fundamentals and future prospects of the company can justify this premium.

Let's see ⤵️

The question arises whether the fundamentals and future prospects of the company can justify this premium.

Let's see ⤵️

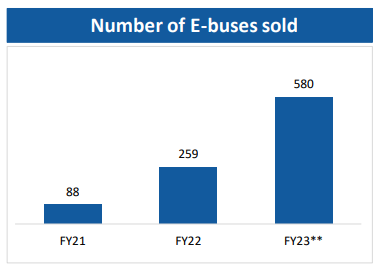

When we look at the company's sales, the company sold around 580 e-buses, including 17 e-tippers, in FY23.

Still, the order book till March 23 was standing at 3,394 e-buses.

When we talk about FY24,

Still, the order book till March 23 was standing at 3,394 e-buses.

When we talk about FY24,

The company received an order for 2,100 e-buses from Brihan Mumbai Electric Supply & Transport in May-23.

And today, on July 7, 2023, the company secured orders for 5,100 e-buses worth over ₹10,000 crores.

However, can the company meet the demand capacity?

Let's see⤵️

And today, on July 7, 2023, the company secured orders for 5,100 e-buses worth over ₹10,000 crores.

However, can the company meet the demand capacity?

Let's see⤵️

The company's Hyderabad facilities produce 1,500 units/year.

Olectra acquired 150 acres in Hyderabad for a new greenfield plant with a capacity of 5,000 units/year, which is scalable upto 10,000 units/year.

Also...

Olectra acquired 150 acres in Hyderabad for a new greenfield plant with a capacity of 5,000 units/year, which is scalable upto 10,000 units/year.

Also...

From the future perspective,

▶️ The company has started to sell e-tippers in Q4FY23. The average selling price of one tipper is around ₹1.4 crores. Also the margins in tipper is greater than the buses.

▶️ The company is strengthening intercity private transport segment.

▶️ The company has started to sell e-tippers in Q4FY23. The average selling price of one tipper is around ₹1.4 crores. Also the margins in tipper is greater than the buses.

▶️ The company is strengthening intercity private transport segment.

▶️ The company has entered into Staff Transport Segment.

▶️ The company is establishing TARMAC buses in airports.

▶️ The company is establishing TARMAC buses in airports.

Considering the future plans, solid fundamentals, robust orderbook, and substantial CAPEX to meet the orders, the company's earnings may experience substantial growth. 📈

Considering all the factors, the market has assigned a price-to-earnings PE of 140 to this company.

Considering all the factors, the market has assigned a price-to-earnings PE of 140 to this company.

This was all.

Thanks for following our analysis on Olectra!

Like 👍, retweet 🔁 the first tweet, and comment your thoughts on the company's valuation.

Follow @Finology_Quest for more analysis.

Visit bit.ly to learn about finance. Happy learning! 💼💡

#Quest

Thanks for following our analysis on Olectra!

Like 👍, retweet 🔁 the first tweet, and comment your thoughts on the company's valuation.

Follow @Finology_Quest for more analysis.

Visit bit.ly to learn about finance. Happy learning! 💼💡

#Quest

جاري تحميل الاقتراحات...