Taxes are your biggest expense in life so strategic tax planning is a must.

If you own a business you can pay your kids $13,850 tax-free & deduct it on your taxes.

Your child will owe $0 in taxes, can invest in a tax-free Roth IRA, and you legally avoided taxes.

Let's discuss:

If you own a business you can pay your kids $13,850 tax-free & deduct it on your taxes.

Your child will owe $0 in taxes, can invest in a tax-free Roth IRA, and you legally avoided taxes.

Let's discuss:

When you employ your children it's s a business expense and business expenses are tax-deductible.

Children can perform tasks such as administrative work, social media management, or other age-appropriate responsibilities.

Children can perform tasks such as administrative work, social media management, or other age-appropriate responsibilities.

You need to pay your children a reasonable wage for the work they do.

It's considered tax evasion if you pay a 1-year-old $13,850 per year to do your accounting.

It's considered tax evasion if you pay a 1-year-old $13,850 per year to do your accounting.

To avoid self-employment tax (15.3%), you put your child on payroll and issue a W-2, then use the standard deduction to reduce their taxable income.

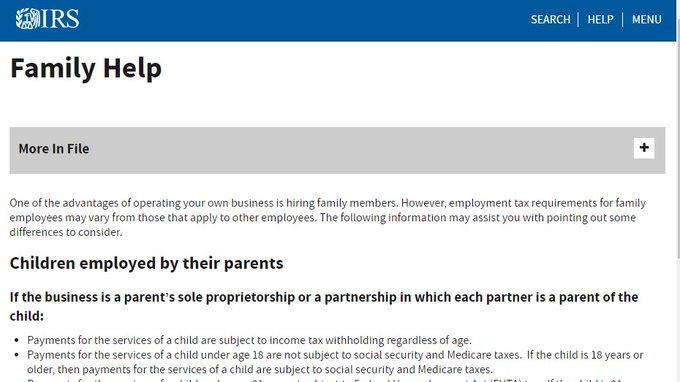

Children under 18 who work for a business owned by their parents are exempt from paying Social Security and Medicare taxes.

Children under 18 who work for a business owned by their parents are exempt from paying Social Security and Medicare taxes.

When you pay your child for their work it's considered a business expense and you can deduct it from your taxable income, lowering your tax liability.

Make your child a millionaire by opening a custodial Roth IRA, investing it in an S&P 500 index fund, and it will grow tax-free.

Make your child a millionaire by opening a custodial Roth IRA, investing it in an S&P 500 index fund, and it will grow tax-free.

A ROTH IRA is a retirement account that allows you to invest tax-free!

Because ROTH IRAs offer tax-free growth, your investments compound and grow faster!

With a ROTH IRA, you can withdraw your contributions at any time.

Because ROTH IRAs offer tax-free growth, your investments compound and grow faster!

With a ROTH IRA, you can withdraw your contributions at any time.

Your child can become a millionaire with a ROTH IRA & pay no taxes:

1) Invest $11 a day into an S&P 500 index fund

2) Let compound interest do all the work

3) In 30 years you’ll have $1,002,208, tax-free

*Historically, the S&P 500 earned ~11% per year, over the last 96 years

1) Invest $11 a day into an S&P 500 index fund

2) Let compound interest do all the work

3) In 30 years you’ll have $1,002,208, tax-free

*Historically, the S&P 500 earned ~11% per year, over the last 96 years

The power of compound interest and maxing out a Roth IRA:

10 Years: $117,369

20 Years: $433,591

30 Years: $1,331,479

40 Years: $3,880,962

50 Years: $11,120,016

(*based on an 11% return, after the S&P 500's 96-year historical average, since 1926)

10 Years: $117,369

20 Years: $433,591

30 Years: $1,331,479

40 Years: $3,880,962

50 Years: $11,120,016

(*based on an 11% return, after the S&P 500's 96-year historical average, since 1926)

Popular Roth IRA index fund options:

$VOO: exposure to the S&P 500, 500 large-cap US companies

$VTI: exposure to the entire U.S. stock market, including both large and small-cap companies

$QQQ: exposure to the NASDAQ-100, 100 large-cap and tech-focused companies

$VOO: exposure to the S&P 500, 500 large-cap US companies

$VTI: exposure to the entire U.S. stock market, including both large and small-cap companies

$QQQ: exposure to the NASDAQ-100, 100 large-cap and tech-focused companies

4 ways to max a Roth IRA:

• $18 a day, or

• $125 a week, or

• $542 a month, or

• $6,500 a year

Advantages of a Roth IRA:

• Tax-free growth

• Tax-free withdrawals

• Can be used as an emergency fund

• $18 a day, or

• $125 a week, or

• $542 a month, or

• $6,500 a year

Advantages of a Roth IRA:

• Tax-free growth

• Tax-free withdrawals

• Can be used as an emergency fund

You can withdraw your contributions anytime.

You can withdraw capital gains before 59 1/2 penalty-free for:

• Disabilities

• Education expenses

• First-time home purchase

• Birth/ adoption expenses

• Health insurance (if unemployed)

You can withdraw capital gains before 59 1/2 penalty-free for:

• Disabilities

• Education expenses

• First-time home purchase

• Birth/ adoption expenses

• Health insurance (if unemployed)

You can have over $1.3 million for retirement when you are 60 if you start investing $100 a week into an S&P 500 index fund at 25.

It's important to start investing for retirement as early as possible, to take advantage of the power of compound interest.

It's important to start investing for retirement as early as possible, to take advantage of the power of compound interest.

Hiring your children for your business (or side hustle) and investing their pay in a tax-free ROTH IRA is a strategy to save you money on taxes and teach your child valuable skills.

They will learn about budgeting, saving, and investing, all while earning money for themselves.

They will learn about budgeting, saving, and investing, all while earning money for themselves.

Please remember:

• Track hours worked

• Child has to perform actual task

• Check state requirements for age

• Create contract detailing responsibilities

• Child has to be paid age-appropriate reasonable wage

Consult with tax professional or visit the IRS website for more:

• Track hours worked

• Child has to perform actual task

• Check state requirements for age

• Create contract detailing responsibilities

• Child has to be paid age-appropriate reasonable wage

Consult with tax professional or visit the IRS website for more:

Tax misconception:

A tax refund is NOT a "gift" from the government, it's an overpayment of your tax bill.

Receiving a large refund is giving the government can be compared to an interest-free loan throughout the year.

This is money you could have invested in a Roth IRA.

A tax refund is NOT a "gift" from the government, it's an overpayment of your tax bill.

Receiving a large refund is giving the government can be compared to an interest-free loan throughout the year.

This is money you could have invested in a Roth IRA.

Pay your legal share of taxes, and nothing more. If you found this thread helpful, please:

• RT the FIRST tweet to share it🔁

• Follow me @FluentInFinance for more

• Sign-up for my FREE newsletter to learn more about money: TheMoneyNewsletter.com!

• RT the FIRST tweet to share it🔁

• Follow me @FluentInFinance for more

• Sign-up for my FREE newsletter to learn more about money: TheMoneyNewsletter.com!

Loading suggestions...