We published our annual Big Ideas report this week

ark-invest.com

This has been a year marked by convergence

Convergences that should yield unprecedented value accrual

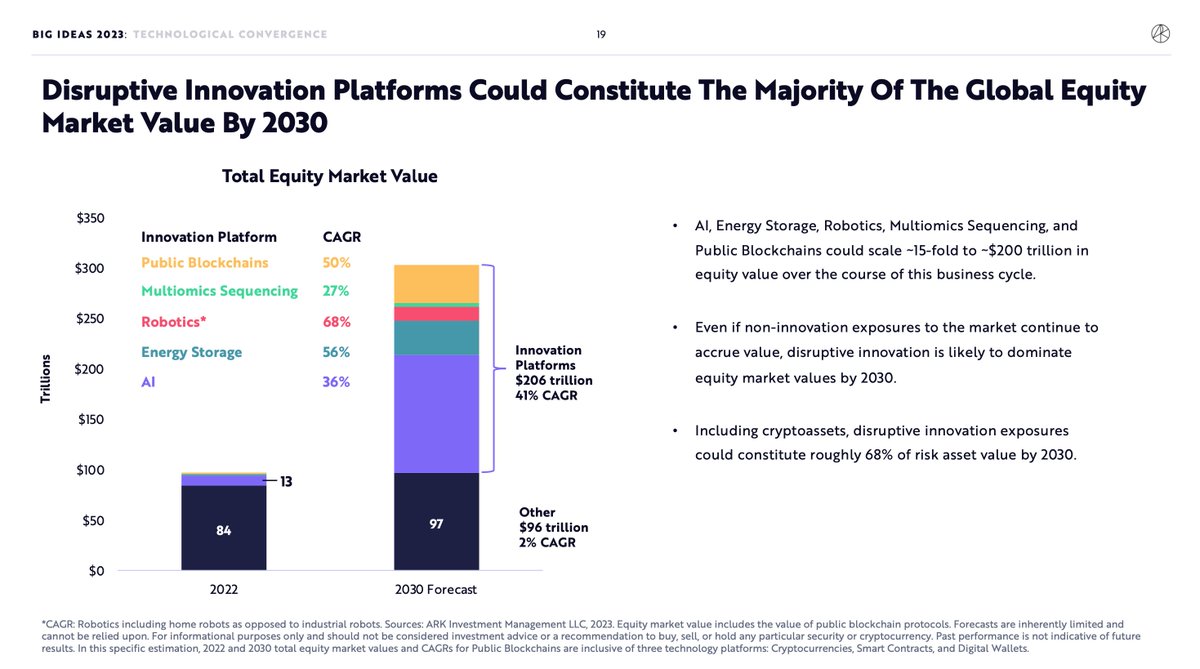

We believe that disruptive innovation should command more than half of total market cap by 2030

ark-invest.com

This has been a year marked by convergence

Convergences that should yield unprecedented value accrual

We believe that disruptive innovation should command more than half of total market cap by 2030

We focus on 5 innovation platforms that all follow steep cost declines, cut across sectors and are themselves platforms of innovation.

Fascinating how technologies are not only cutting across sectors, but also serving as catalysts for each other

(fly)wheels within (fly)wheels

Fascinating how technologies are not only cutting across sectors, but also serving as catalysts for each other

(fly)wheels within (fly)wheels

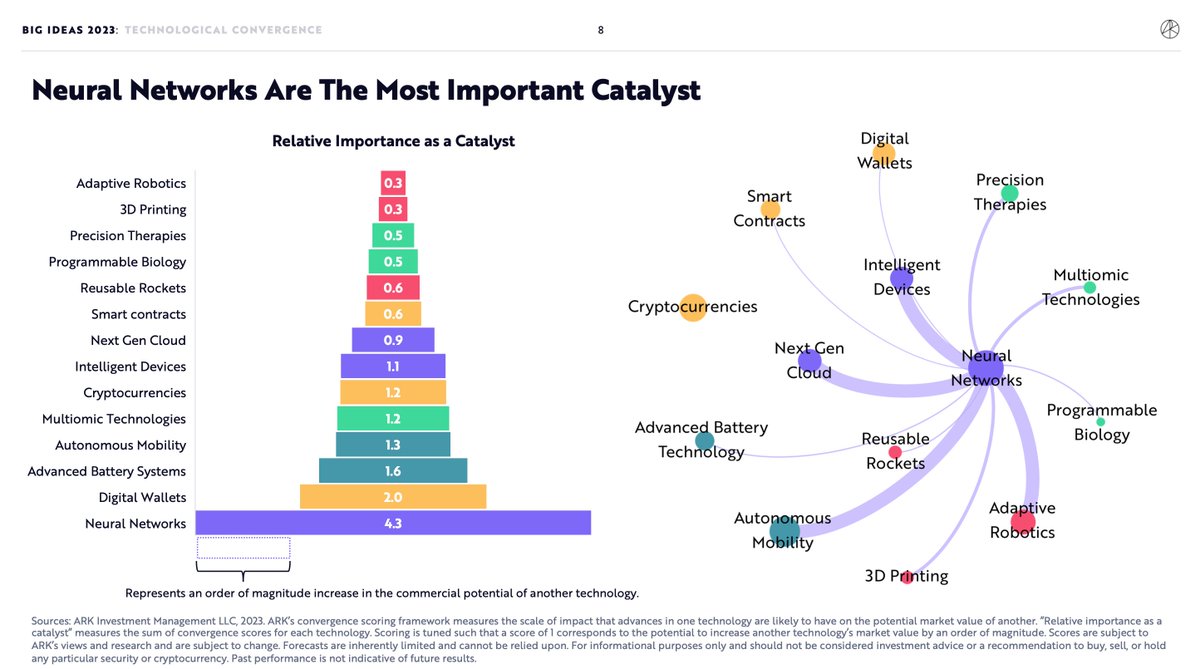

We dimension and map that convergence at a lower level of our technology taxonomy, visualized here.

We identify 14 disruptive technologies—each with its own cost decline and demand-expectation—that are distinctly investable.

We identify 14 disruptive technologies—each with its own cost decline and demand-expectation—that are distinctly investable.

(Investable: there is the opportunity for extra-normal cashflow accrual in a part of the value chain that is materially mispriced in today’s equity markets.)

Each of these 14 technologies is catalyzed by and catalyzing other technologies

An acceleration in AI leads to an acceleration in autonomous mobility and wearable devices and demand for batteries and the utility of multiomics data and truly digitized finance.

An acceleration in AI leads to an acceleration in autonomous mobility and wearable devices and demand for batteries and the utility of multiomics data and truly digitized finance.

That AI is so obviously accelerating raises the odds for every accompanying technology to accelerate.

There is already plenty of evidence of convergence already.

There is already plenty of evidence of convergence already.

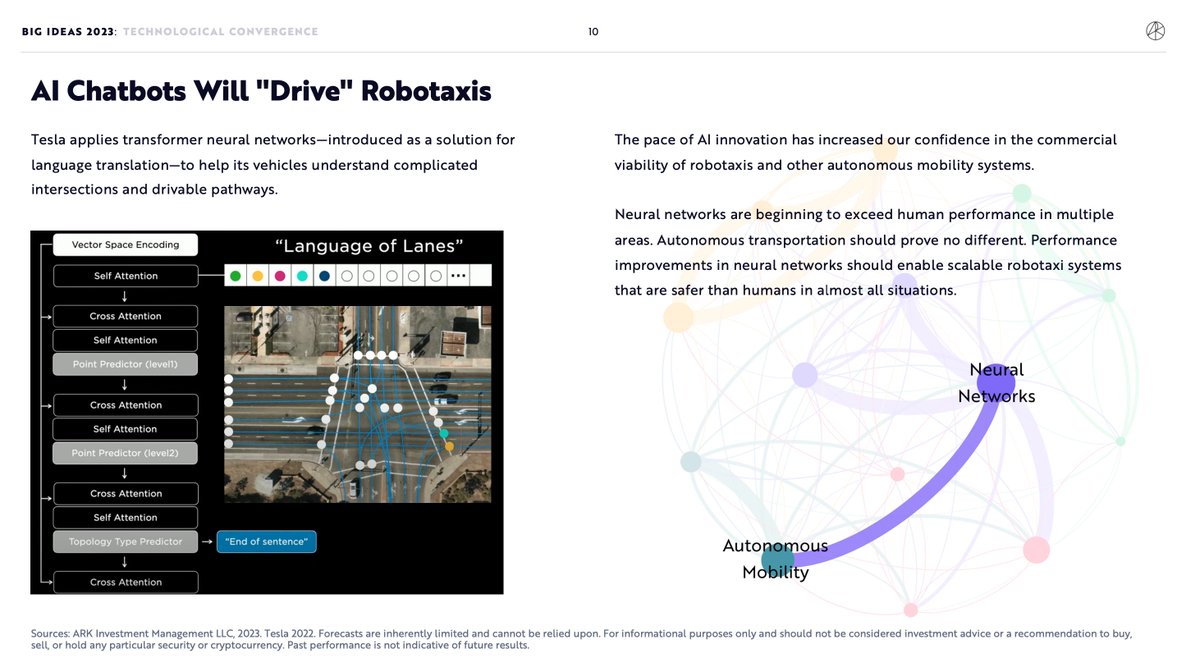

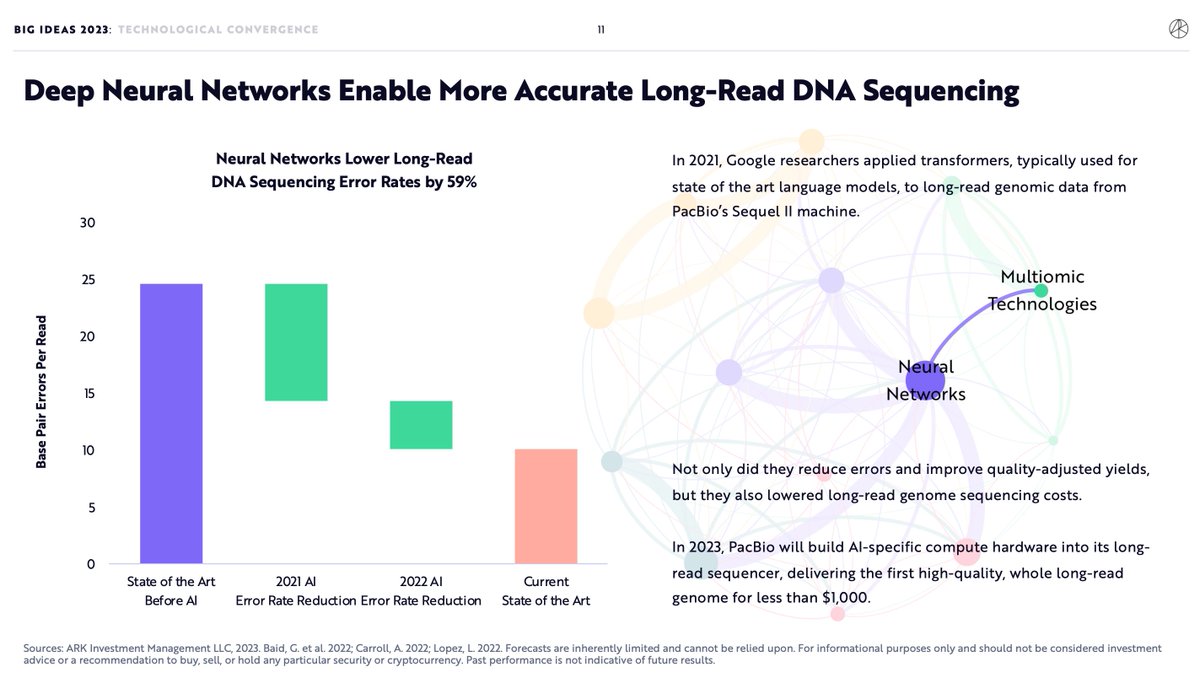

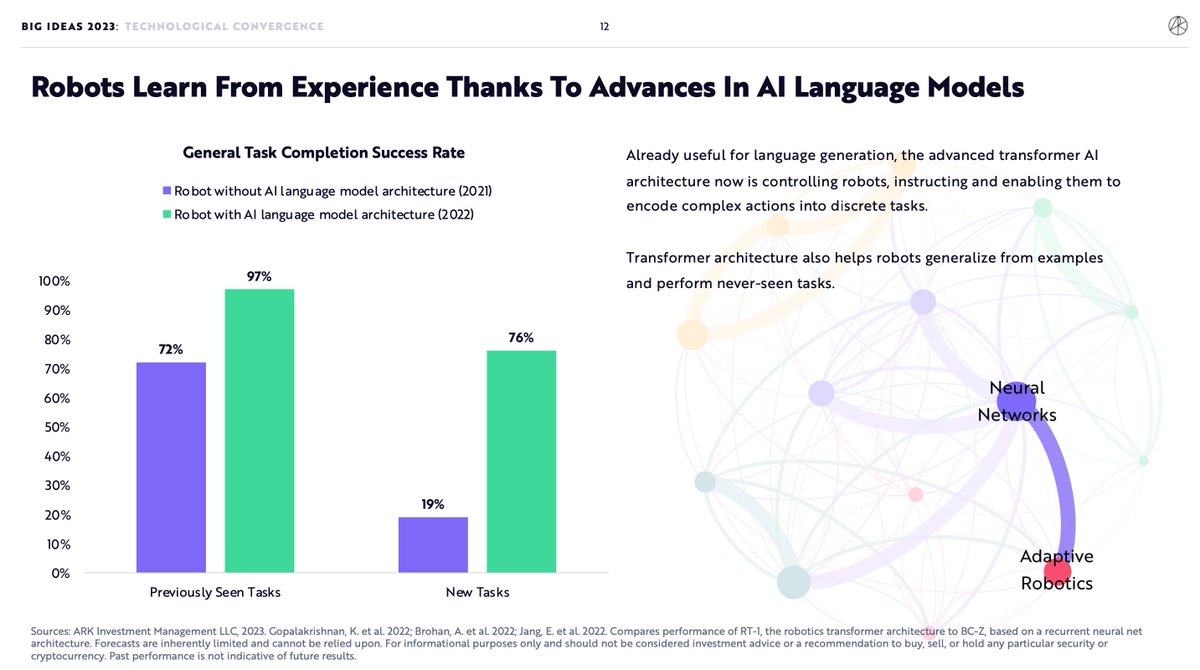

The transformer architecture, introduced to improve AI language translation, not only led to chatGPT, it also helped robotaxis understand intersections, long-read sequencers >halve their base-read error rates, and allowed robots to perform never-before-seen household tasks.

And it’s not just AI.

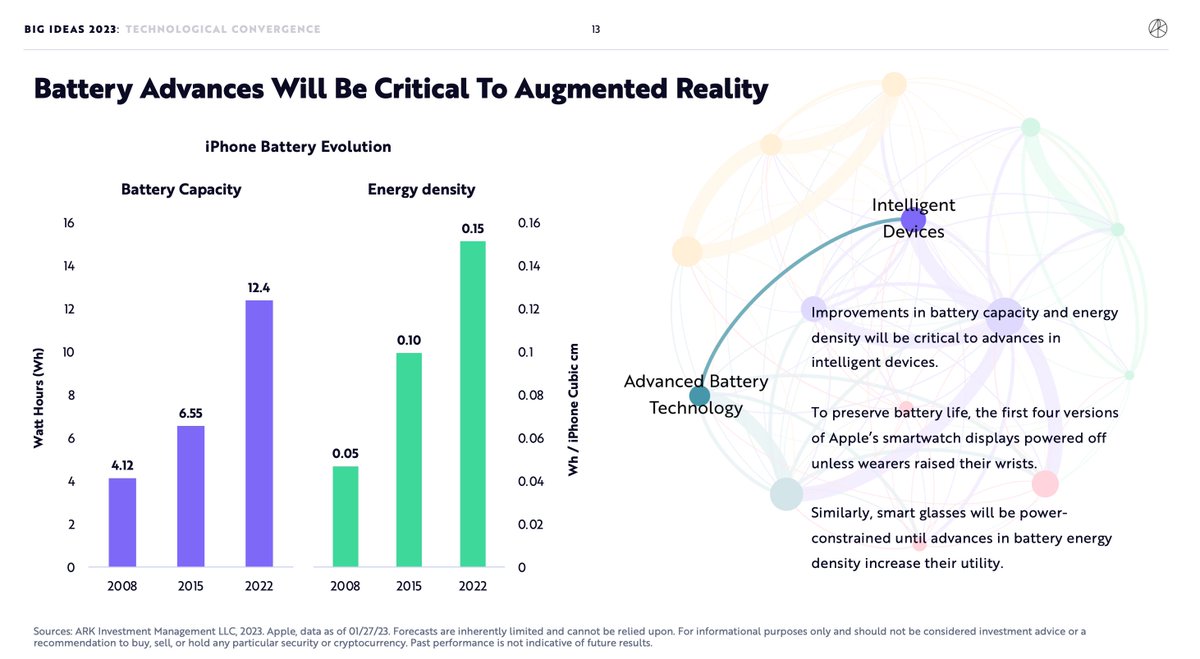

Continued battery advances are probably required to enable practically useful augmented reality goggles.

Electric vehicle adoption may be critical for our augmented reality future.

Continued battery advances are probably required to enable practically useful augmented reality goggles.

Electric vehicle adoption may be critical for our augmented reality future.

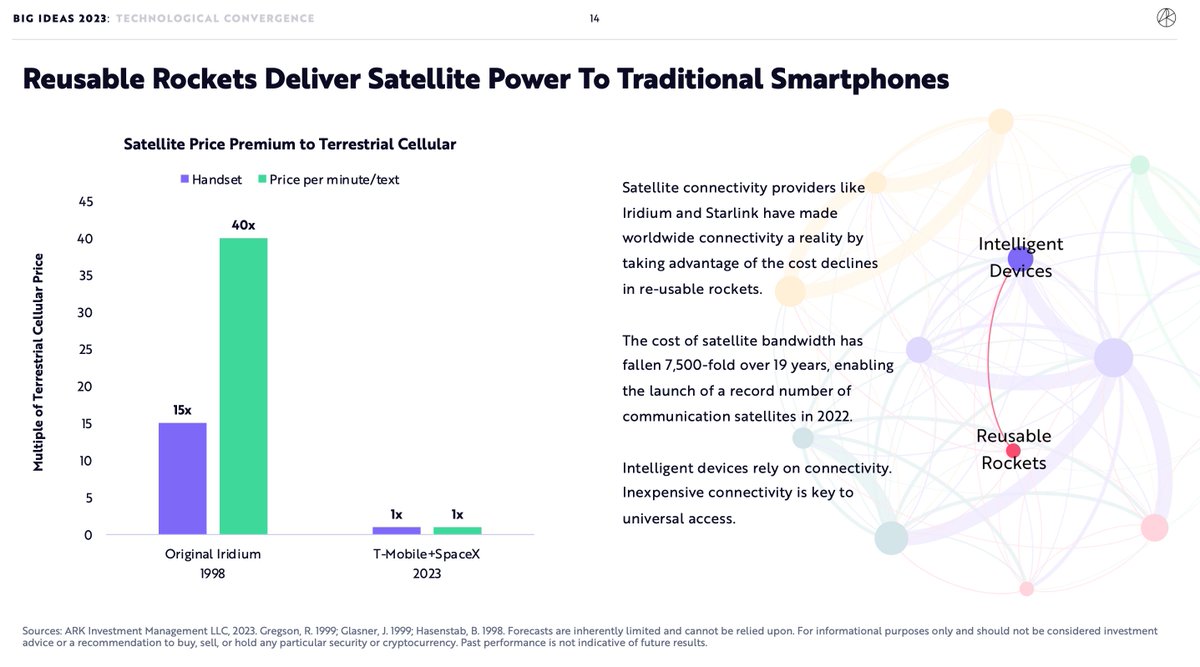

Reusable rockets are about to upgrade smartphones

The low cost of lofting large satellites should let tMobile provide satellite connectivity bundled with a standard data plan.

Possible before reusable rockets but at an order of magnitude higher cost on a specialized device.

The low cost of lofting large satellites should let tMobile provide satellite connectivity bundled with a standard data plan.

Possible before reusable rockets but at an order of magnitude higher cost on a specialized device.

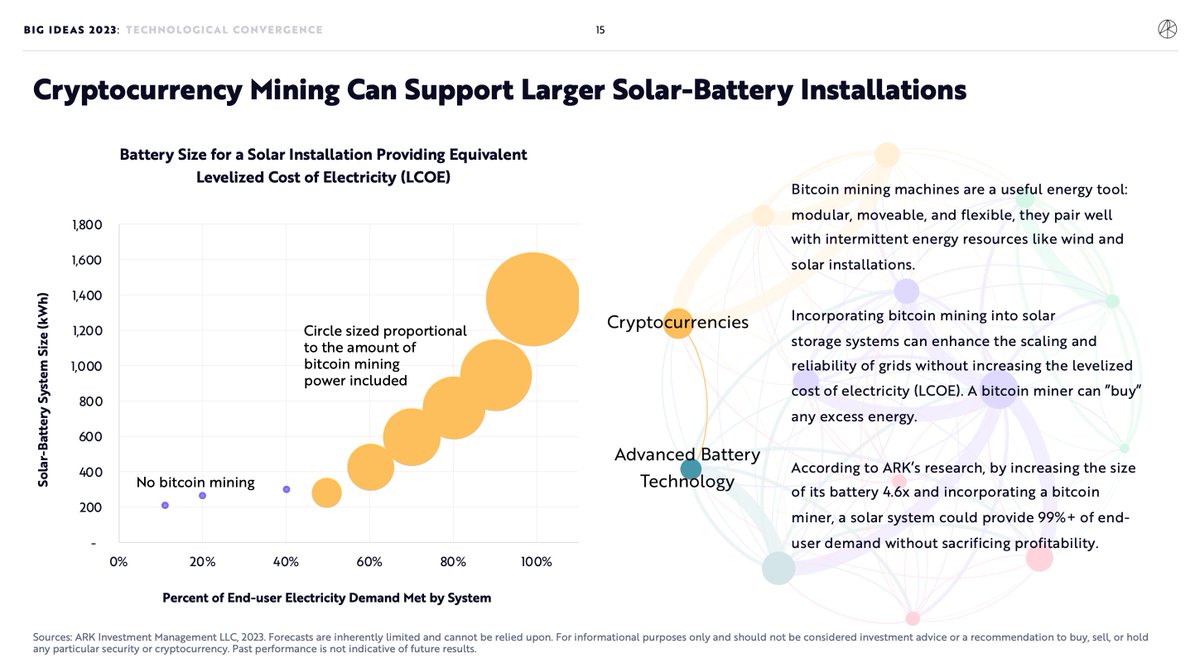

And bitcoin provides energy companies with a new tool to balance and offset energy demand.

Intermittent solar can become a reliable energy system for no additional cost to the end consumer with a much larger battery and bitcoin mining to monetize excess energy

Intermittent solar can become a reliable energy system for no additional cost to the end consumer with a much larger battery and bitcoin mining to monetize excess energy

As these technologies stack, we believe they are going to yield profound productivity advances.

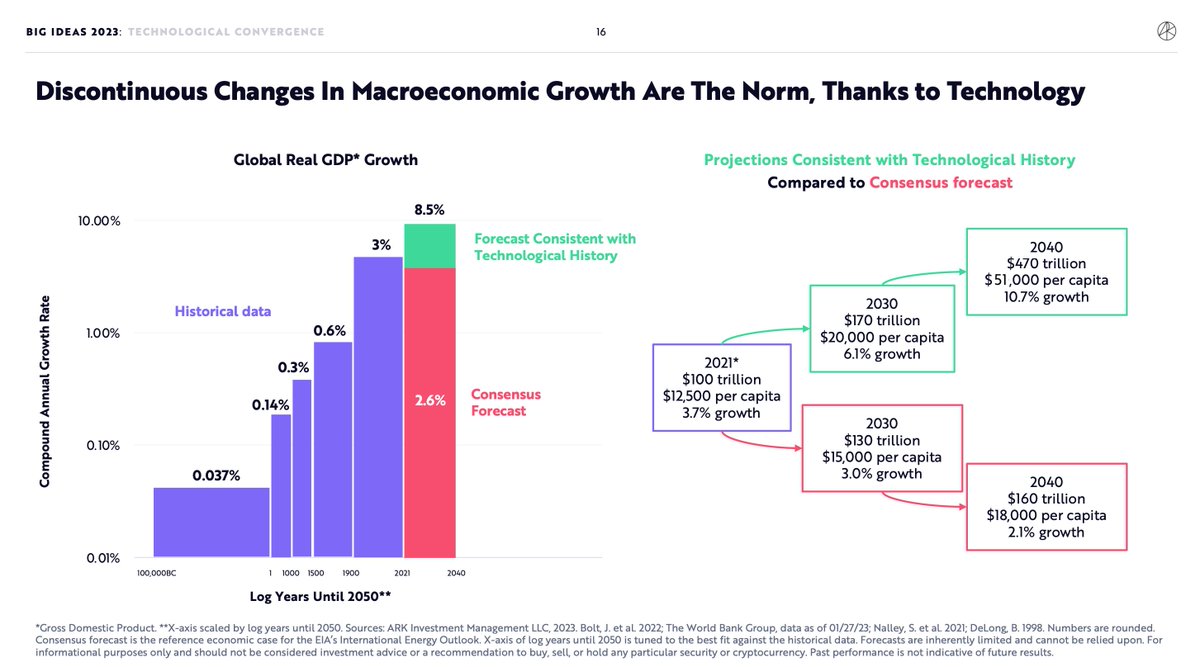

Though many don’t recognize it, a profound inflection in the rate of growth would be consistent with technological economic history.

Though many don’t recognize it, a profound inflection in the rate of growth would be consistent with technological economic history.

But the timing of a change in the rate of growth can be tricky.

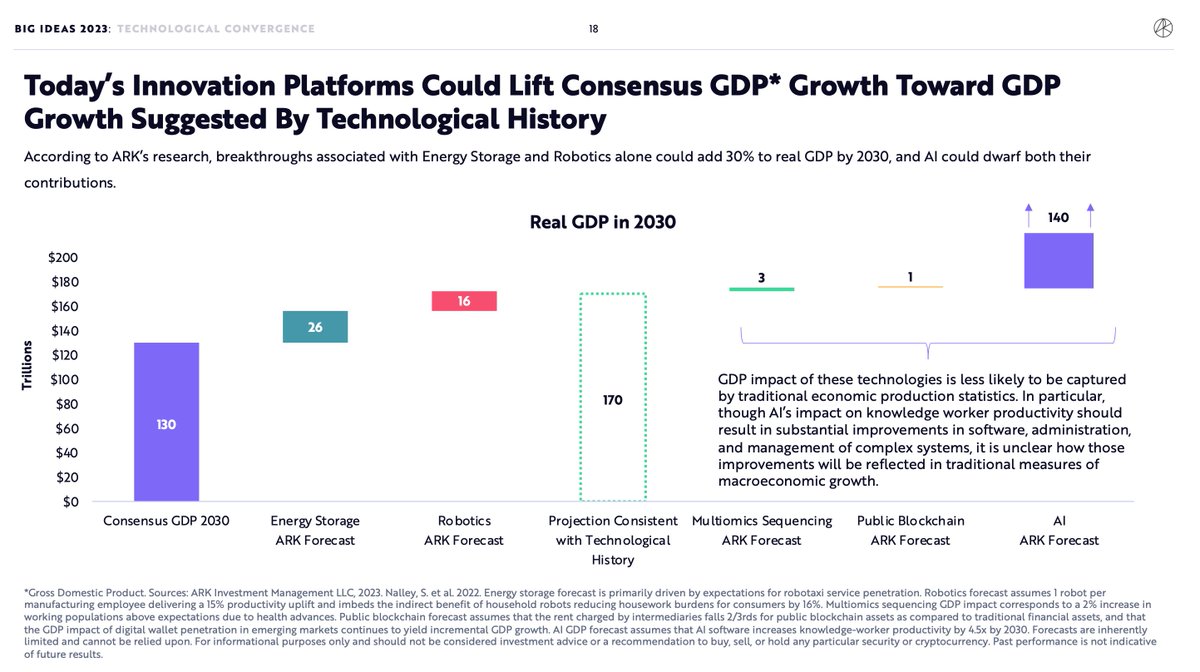

In robotics and robotaxi-driven energy storage alone—areas where productivity advances are more likely to be captured in GDP—our modeling suggests that the discontinuous growth trajectory is likely this decade.

In robotics and robotaxi-driven energy storage alone—areas where productivity advances are more likely to be captured in GDP—our modeling suggests that the discontinuous growth trajectory is likely this decade.

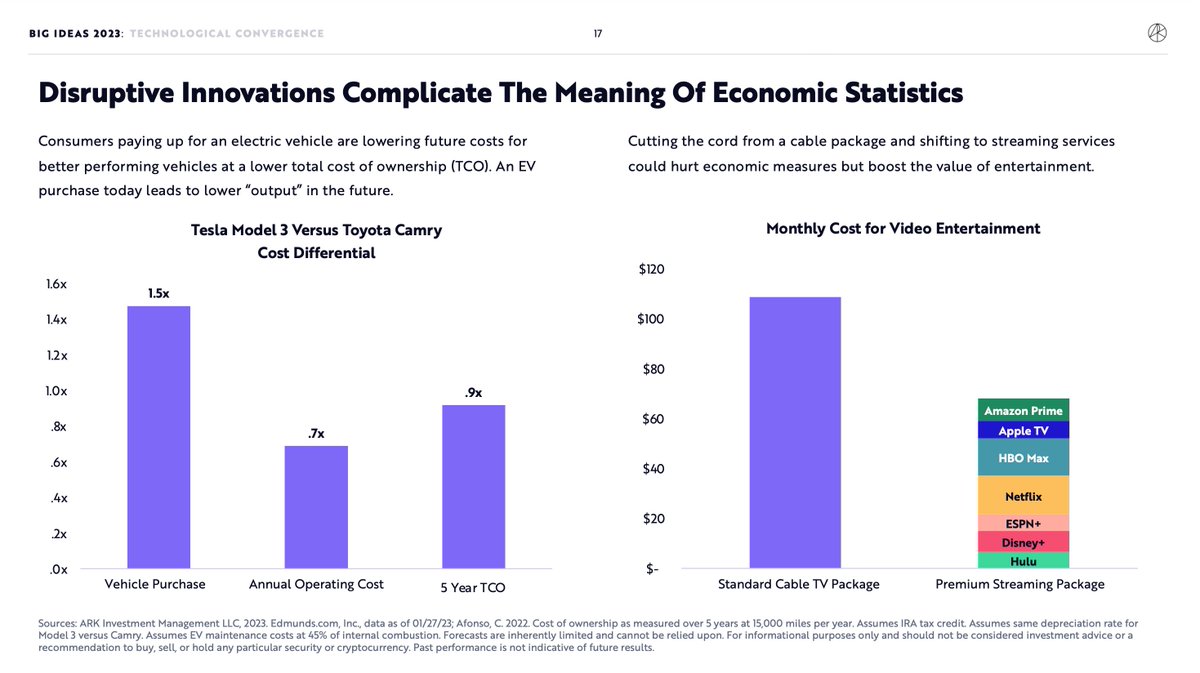

It is true, however, that disruptive technology confounds macroeconomic statistics, and though the strongest productivity advances are likely to feed through AI, it’s less clear how the deflationary growth that AI yields will appear in traditional measurements of output.

Somebody cutting their pay TV cable in exchange for advertising-free streaming services, for example, would be read through as GDP negative though the value to the end-consumer is clearly positive.

Ditto an electric vehicle being “more expensive” when it is TCO cheaper.

Ditto an electric vehicle being “more expensive” when it is TCO cheaper.

Ultimately we believe that hundreds of trillions in value will accrue to the 5 innovation platforms in this business cycle.

Due to convergence, more than ever, a technological acceleration anywhere will proliferate across innovation platforms.

Due to convergence, more than ever, a technological acceleration anywhere will proliferate across innovation platforms.

An AI acceleration begets an acceleration in everything.

(fly)wheels within (fly)wheels (within (fly)wheels)

(fly)wheels within (fly)wheels (within (fly)wheels)

Loading suggestions...