The latest FASB ruling will be a pretty big deal for #Bitcoin.

But what’s FASB, and why should you care?

Time for a Corporate Treasury 🧵👇

But what’s FASB, and why should you care?

Time for a Corporate Treasury 🧵👇

Accounting is boring. FASB bleh. 🤮

Normally, yes. But not this time. The latest FASB vote opens the door for companies to buy and hold Bitcoin in corporate treasuries without balance sheet penalties

OK, how?

Let's walk through it nice and easy, shall we?

Normally, yes. But not this time. The latest FASB vote opens the door for companies to buy and hold Bitcoin in corporate treasuries without balance sheet penalties

OK, how?

Let's walk through it nice and easy, shall we?

🤓 What’s FASB?

First, the Financial Accounting Standards Board, known as FASB (FAZ-bee), is an independent organization that establishes accounting and financial reporting standards for US-based companies

These are known as the generally accepted accounting principles, or GAAP

First, the Financial Accounting Standards Board, known as FASB (FAZ-bee), is an independent organization that establishes accounting and financial reporting standards for US-based companies

These are known as the generally accepted accounting principles, or GAAP

As investors, why do we care?

Because the SEC recognizes FASB as the official accounting rule maker for US public companies

If companies do not follow GAAP principles, they’re out of compliance, and no respectable accounting firm will certify their financials as correct.

Because the SEC recognizes FASB as the official accounting rule maker for US public companies

If companies do not follow GAAP principles, they’re out of compliance, and no respectable accounting firm will certify their financials as correct.

🧐 Long-Lived Intangible Assets

At the heart of why the latest FASB ruling matters for Bitcoin, is the 'long-lived intangible asset'

See, FASB originally determined that Bitcoin was to be considered a long-lived intangible asset, much like a patent, copyright, or trademark. 🙄

At the heart of why the latest FASB ruling matters for Bitcoin, is the 'long-lived intangible asset'

See, FASB originally determined that Bitcoin was to be considered a long-lived intangible asset, much like a patent, copyright, or trademark. 🙄

This creates a problem when the asset is accounted for on a company’s balance sheet

Keeping it simple, say a company buys a drug patent from another company for $100M

The company lists it as a long-lived intangible asset on its balance sheet at the purchase price of $100M.

Keeping it simple, say a company buys a drug patent from another company for $100M

The company lists it as a long-lived intangible asset on its balance sheet at the purchase price of $100M.

Let’s say another company then creates a better drug, making this patent worth less than the purchase price

The original patent is said to be *impaired* in value,

and the patent evaluators now say it is only worth $50M.

The original patent is said to be *impaired* in value,

and the patent evaluators now say it is only worth $50M.

The company must list the patent on its balance sheet as a $50M asset and recognize a $50M loss

Let’s then say the new drug ends up not working and is taken off the market. People turn back to the original drug, restoring its $100M value

As far as FASB is concerned, too bad.

Let’s then say the new drug ends up not working and is taken off the market. People turn back to the original drug, restoring its $100M value

As far as FASB is concerned, too bad.

It has been *impaired*

And until the company sells that patent, the asset must be held at the impaired value of $50 million

**Note: this example purposefully ignores amortization, etc. to keep it simple for today.

And until the company sells that patent, the asset must be held at the impaired value of $50 million

**Note: this example purposefully ignores amortization, etc. to keep it simple for today.

OK, then how exactly does this affect Bitcoin and companies buying Bitcoin with their extra cash?

Let’s see.

Let’s see.

✍️ MicroStrategy & BTC Losses

The main problem with treating Bitcoin as a long-lived intangible asset, is that it's actually a liquid asset that trades on exchanges globally

24 hours a day, 365 days a year, Bitcoin’s price is continuously updated.

The main problem with treating Bitcoin as a long-lived intangible asset, is that it's actually a liquid asset that trades on exchanges globally

24 hours a day, 365 days a year, Bitcoin’s price is continuously updated.

Though Bitcoin is not a security, it trades even more often than securities

Plus, Gary Gensler, the Chairman of the SEC has stated he considers Bitcoin a commodity

It goes to reason, therefore, that Bitcoin should be treated like other tangible commodities, i.e., gold or oil

Plus, Gary Gensler, the Chairman of the SEC has stated he considers Bitcoin a commodity

It goes to reason, therefore, that Bitcoin should be treated like other tangible commodities, i.e., gold or oil

Yet FASB initially decided that Bitcoin should be considered a long-lived intangible asset

What this means is that if a company buys Bitcoin, it must list it on its balance sheet at the lower amount of cost or market value.

What this means is that if a company buys Bitcoin, it must list it on its balance sheet at the lower amount of cost or market value.

For example:

A public company uses some extra cash to buy $1M of Bitcoin, and lists the holding as a Digital Asset on its balance sheet, worth $1M

Then the Bitcoin price rises 20%

In its financials, the company cannot recognize this increase and must maintain Bitcoin at $1M.

A public company uses some extra cash to buy $1M of Bitcoin, and lists the holding as a Digital Asset on its balance sheet, worth $1M

Then the Bitcoin price rises 20%

In its financials, the company cannot recognize this increase and must maintain Bitcoin at $1M.

Then, let’s say that Bitcoin falls 50%, and is now worth 60% of where the company bought it

In its financials, the company must recognize this decrease as an impairment in value and list its Bitcoin holdings at $600K, with a $400K loss.

In its financials, the company must recognize this decrease as an impairment in value and list its Bitcoin holdings at $600K, with a $400K loss.

Even if Bitcoin then trades back up, $600K would remain the carrying value for the company’s balance sheet going forward

The only way to recognize price recovery is to sell the Bitcoin and trigger a *capital gain*

This is exactly what happened to MicroStrategy.

The only way to recognize price recovery is to sell the Bitcoin and trigger a *capital gain*

This is exactly what happened to MicroStrategy.

Michael Saylor bought billions of dollars of Bitcoin, the price increased, and he had to hold the Bitcoin on MicroStrategy’s Balance Sheet at the purchase price

Then, when Bitcoin fell in value, MicroStrategy had to recognize the impairment, and list it as a loss.

Then, when Bitcoin fell in value, MicroStrategy had to recognize the impairment, and list it as a loss.

Furthermore, when Bitcoin recovered in price, MicroStrategy could not recognize this recovery, and they had to keep the value on its books at that 'impaired' level

Even though Bitcoin had since recovered much of the value.

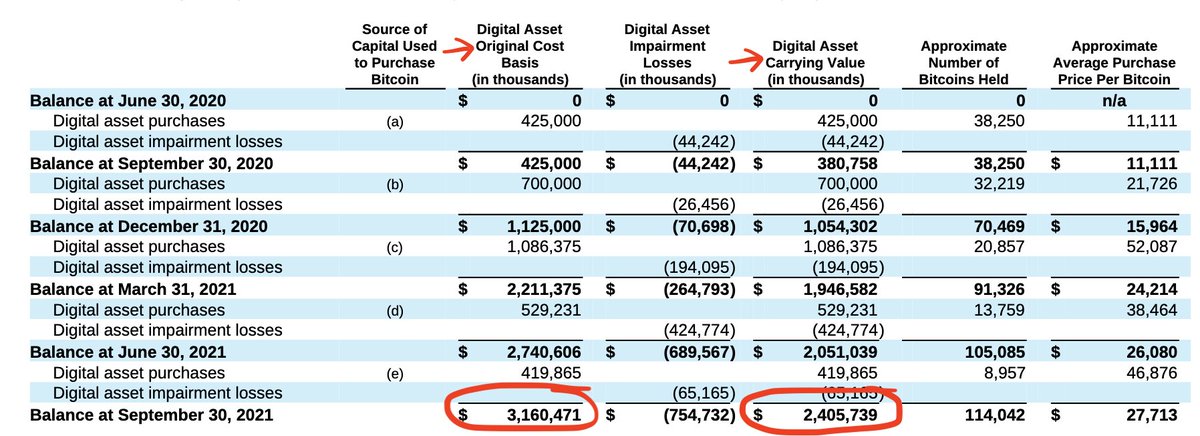

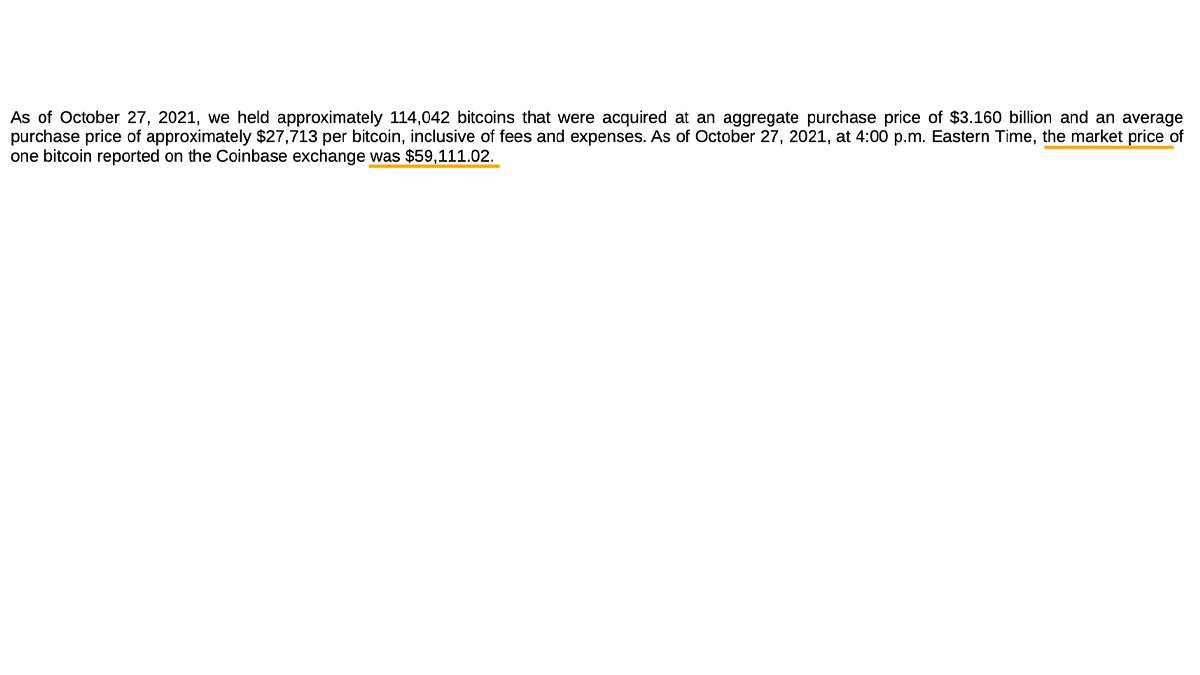

MSTR 10-Q 09/30/2021:

Even though Bitcoin had since recovered much of the value.

MSTR 10-Q 09/30/2021:

And so instead of listing the value where it was now trading in the markets, MicroStrategy had to just include a footnote to show what the actual trading value was at the time of the financial statement, instead.

MSTR 10-Q 09/30/2021:

MSTR 10-Q 09/30/2021:

Mainstream media honed in on this, criticizing Saylor and repeating the word impaired in headlines over and over again

This is why so many companies have been reluctant to buy any Bitcoin in their treasuries, even if positively predisposed to the asset as an alternative to cash.

This is why so many companies have been reluctant to buy any Bitcoin in their treasuries, even if positively predisposed to the asset as an alternative to cash.

With the latest ruling, this issue has been eliminated for companies

Going forward, if a company buys Bitcoin, they will use a recognized exchange *market value* to price the asset every quarter, just like a stock, bond or commodity that trades on a public exchange.

Going forward, if a company buys Bitcoin, they will use a recognized exchange *market value* to price the asset every quarter, just like a stock, bond or commodity that trades on a public exchange.

Bitcoin goes up, it can be recognized

Bitcoin goes down, it is accounted for

Bitcoin recovers, it is recognized

And with this ruling, it is most likely that any profits or losses will then flow through to the income statement and be recognized, too. Another important feature.

Bitcoin goes down, it is accounted for

Bitcoin recovers, it is recognized

And with this ruling, it is most likely that any profits or losses will then flow through to the income statement and be recognized, too. Another important feature.

🤩 Corporate Treasuries Incoming

Great! So, now there will be a rush of companies ready to pour their treasury cash into Bitcoin, right?

Right?

Well, this accounting barrier has been removed, yes, but FASB still must determine the timing and logistics around the new standard.

Great! So, now there will be a rush of companies ready to pour their treasury cash into Bitcoin, right?

Right?

Well, this accounting barrier has been removed, yes, but FASB still must determine the timing and logistics around the new standard.

Plus, there are other considerations for companies, such as tax regs and investment risk profiles

While it is true that Bitcoin has fared well over the long term, especially when compared to many public stocks and bonds, the other truth is that it remains a volatile asset.

While it is true that Bitcoin has fared well over the long term, especially when compared to many public stocks and bonds, the other truth is that it remains a volatile asset.

And though experienced investors understand that volatility is attractive with an appreciating asset, the fact is that the professional upside for a CEO or CFO who invests a company’s hard-earned cash in an asset that may depreciate in value in the short term is limited.

Because most companies are widely held and not controlled by one majority holder (unlike Michael Saylor and MSTR), the *career risk* for those in charge is just too great for them to dive in and allocate their treasury cash to Bitcoin in lieu of straight cash or USTs.

Why?

USTs are widely understood, they're still generally considered *safe* in the institutional investment world

And so, this short-term thinking and worry over shareholder backlash prevents most company executives from stepping beyond their entrenched legacy finance thinking.

USTs are widely understood, they're still generally considered *safe* in the institutional investment world

And so, this short-term thinking and worry over shareholder backlash prevents most company executives from stepping beyond their entrenched legacy finance thinking.

That said, there will be more executives who recognize Bitcoin as hard money

Those who see how Bitcoin is a better long-term investment than bonds

Those who allocate a portion of their company’s treasury to #Bitcoin in lieu of debasing USTs or inflation-melting cash.

Those who see how Bitcoin is a better long-term investment than bonds

Those who allocate a portion of their company’s treasury to #Bitcoin in lieu of debasing USTs or inflation-melting cash.

And it is my belief that these will be the executives who outperform the rest over the long term

Providing their shareholders don’t remain shortsighted and focused on short term risks only, preventing management from expanding their vision.

Providing their shareholders don’t remain shortsighted and focused on short term risks only, preventing management from expanding their vision.

As they say, timing is everything

And the timing of this ruling coupled with the probability of a market recovery in the next year or so, could make some of these executives look like outright geniuses.

And the timing of this ruling coupled with the probability of a market recovery in the next year or so, could make some of these executives look like outright geniuses.

This thread is a summary of a recent 🧠Informationist Newsletter. If you enjoyed it, make sure to:

1. Follow @jameslavish to see more investment related content

2. Subscribe to The Informationist to learn one simplified concept weekly: jameslavish.substack.com

1. Follow @jameslavish to see more investment related content

2. Subscribe to The Informationist to learn one simplified concept weekly: jameslavish.substack.com

Loading suggestions...