Is DeFi dead?

TVL down, yields evaporating, depeg risk, protocol hacks, grave dancing on UST, and a terrible macro outlook.

A DeFi investor perspective.. 🧵

TVL down, yields evaporating, depeg risk, protocol hacks, grave dancing on UST, and a terrible macro outlook.

A DeFi investor perspective.. 🧵

Total Valued Locked (TVL) has dropped from over $240bn into January to around $110bn today (-55%).

In parallel, there has been a flight to safety towards USDC and DAI, where supply-side yields have collapsed to sub 2%. i.e. when yield is not paid in some BS farming token.

Even pushing further out on the risk curve, such as providing liquidity (being an LP) on the very active ETH/USDC pair on Uniswap v3 is projected to pay a yield of around 12%, with the very real risk of impermanent loss when extracting yield from a risky asset vs. a stablecoin.

And whilst the LUNA/UST failure was a function of the low reserves inherent to their algorithmic stablecoin, there have been numerous DeFi exploits that have also wiped out investor capital overnight as well.

Do I still believe that there is still an opportunity to sustainably extract yield in a risk-adjusted manner? short answer, yes - but you'll have to get a bit smarter in how you go about it.

Firstly, how sustainable is all this?

Well, DeFi yields are driven by 2 main factors:

1. Demand for leverage (margin)

2. Fees generated from network activity (transaction volume)

let's look at the trends for both

Well, DeFi yields are driven by 2 main factors:

1. Demand for leverage (margin)

2. Fees generated from network activity (transaction volume)

let's look at the trends for both

Retail demand for leverage is cyclical and highly correlated with price action. During more bullish market scenarios, retail traders are looking to lever up on risk/reward. Many have been liquidated during this violent move downwards.

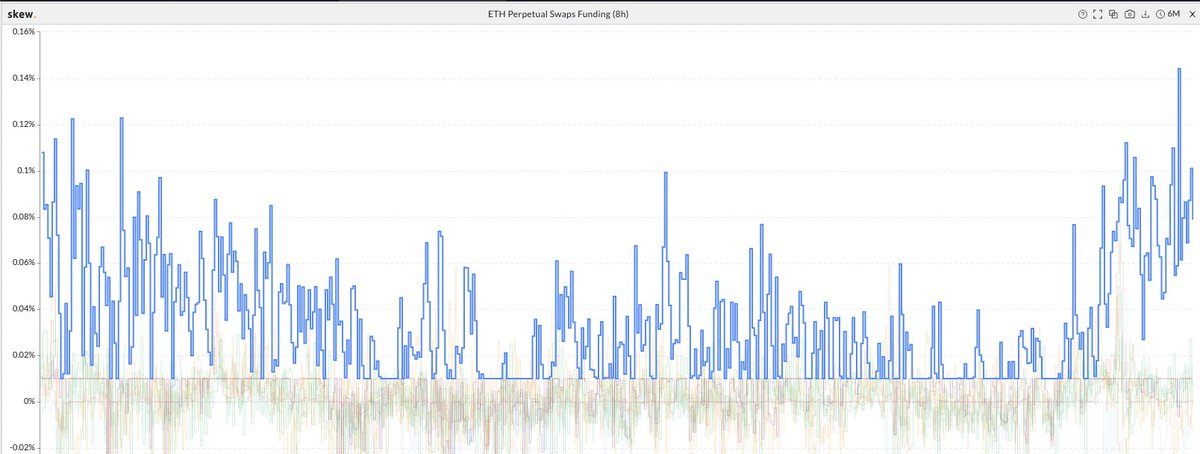

However, the better indicator of retail demand for leverage shows in the funding rate on perps which remains elevated. Having analyzed historical funding rates we can see that there is still considerable demand to remain exposed to both the long and short side of assets like $ETH

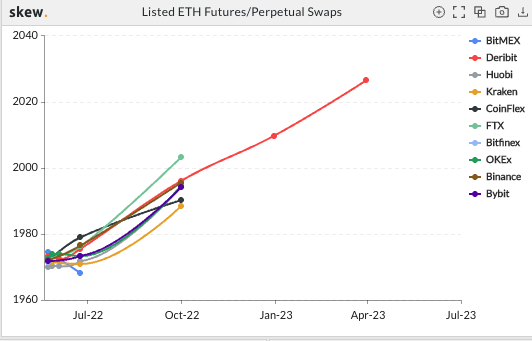

Meanwhile, there is steady demand from ‘smart money’ investors looking for leverage to apply market-neutral strats. For example, a common hedge fund trade is to borrow to buy $ETH, sell futures (which are higher than spot), and make a profit by holding the $ETH exposure to expiry

This spread is referred to as the “basis” and an upward sloping futures curve like this is called “contango”. It reflects broad institutional investor interest to have exposure to the crypto ecosystem. Contango has been persistent lately but can disappear anytime.

Demand for leverage aside, the more encouraging picture for a DeFi investor is from the fees generated by DeFi protocols. Here are the weekly fees generated by Curve Finance amidst the recent market volatility.

Those are record-breaking fees and re-affirm our view that we want to own productive assets like $CRV and $CVX in the long-term, and dollar cost average (DCA) at these low valuation multiples.

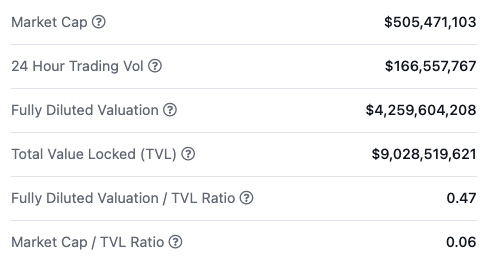

For example, Curve Finance ($CRV) is the dominant AMM for stablecoin swaps. CRV currently trades with a Market Cap / TVL Ratio of 0.06.

so if yield farming you'll want to dynamically adjust your allocation to both stable coin farming and blue-chip token farming depending on supply/demand outlook. Platforms like CRV offer counter-cyclical opportunities but take profits and don't lockup for long imo.

So with yields saturated, you'll mainly want to apply some low-risk innovation. One strategy that we have successfully implemented is called “Skew Farming”

Here we have developed our relationship with a leading VC-backed DeFi protocol (@TracerDAO) to build a strategy for market-neutral returns. Essentially this involves an arbitrage opportunity where we take both a long and a short position on an asset, but on different platforms.

Implemented in a bespoke manner, we could easily extend this to be a systematic strategy, coded up with signals and a trading API.

Other such strategies include a funding arbitrage strategy that we are working on together with the highly reputable @indexcoop

Other such strategies include a funding arbitrage strategy that we are working on together with the highly reputable @indexcoop

Lastly, we are increasing our exposure to DeFi protocols where there is a real-world use case.

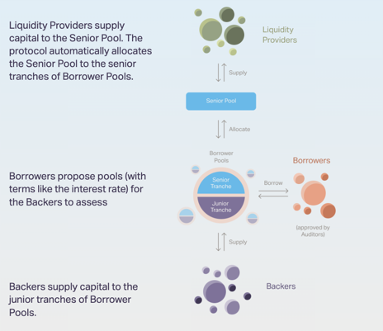

@goldfinch_fi allows real-world borrowers to take out a loan in their domestic currency. On the back end, liquidity providers like me make a crypto loan and earn 12-14% APY from high-quality borrowers. In the event of a default, this is absorbed by riskier junior tranches.

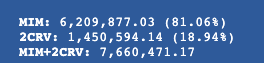

You could also play short term narratives like Tron and USDD and USN as long as you're sat by your laptop and can consistently monitor pool imbalances. Another example, MIM2CRV on Arbi using Beefy currently pays 23.60% APY but here's the curve pool

..but rotating capital even on an L2 can be really inefficient once you've factored in deposit, withdrawal and performance fees. Honestly I don't know many people who can be arsed for a few hundred/thousand dollars on millions of dollar deposit.

So in summary, your best bet is to get busy educating yourself on where all of this is going. If you have some coding skills, build some systematic strats and perhaps learn how to integrate them with a mempool explorer with added alfa.

And generally speaking, as ever - short euphoria and buy extreme fear. Take profits and enjoy the summer.

Loading suggestions...