This Thread will teach you how to perform a Discounted Cash Flow (DCF) Model 👇🏼

The DCF is a valuation method to estimate the value of future cashflows.

Because the “Time Value of Money” concept money is worth more today than in the future.

(Because you can earn interest on it)

That‘s why investors need to figure out what future cashflows are worth today.

Because the “Time Value of Money” concept money is worth more today than in the future.

(Because you can earn interest on it)

That‘s why investors need to figure out what future cashflows are worth today.

Step 1 - Forecasting

Since the future is unknown, you have to forecast future cash flows.

You do that based on historical data, own research, estimates, etc.

As for every single estimate made in the process of a DCF, the number 1 rule is to stay conservative.

Since the future is unknown, you have to forecast future cash flows.

You do that based on historical data, own research, estimates, etc.

As for every single estimate made in the process of a DCF, the number 1 rule is to stay conservative.

Step 2 - The Discount Rate

Next, you need to figure out the discount rate you’re using.

There are a couple of different ideas on the discount rate.

In academia and in banks, the WACC (Weighted average cost of capital) is used.

Buffett goes with a “long-term government” rate.

Next, you need to figure out the discount rate you’re using.

There are a couple of different ideas on the discount rate.

In academia and in banks, the WACC (Weighted average cost of capital) is used.

Buffett goes with a “long-term government” rate.

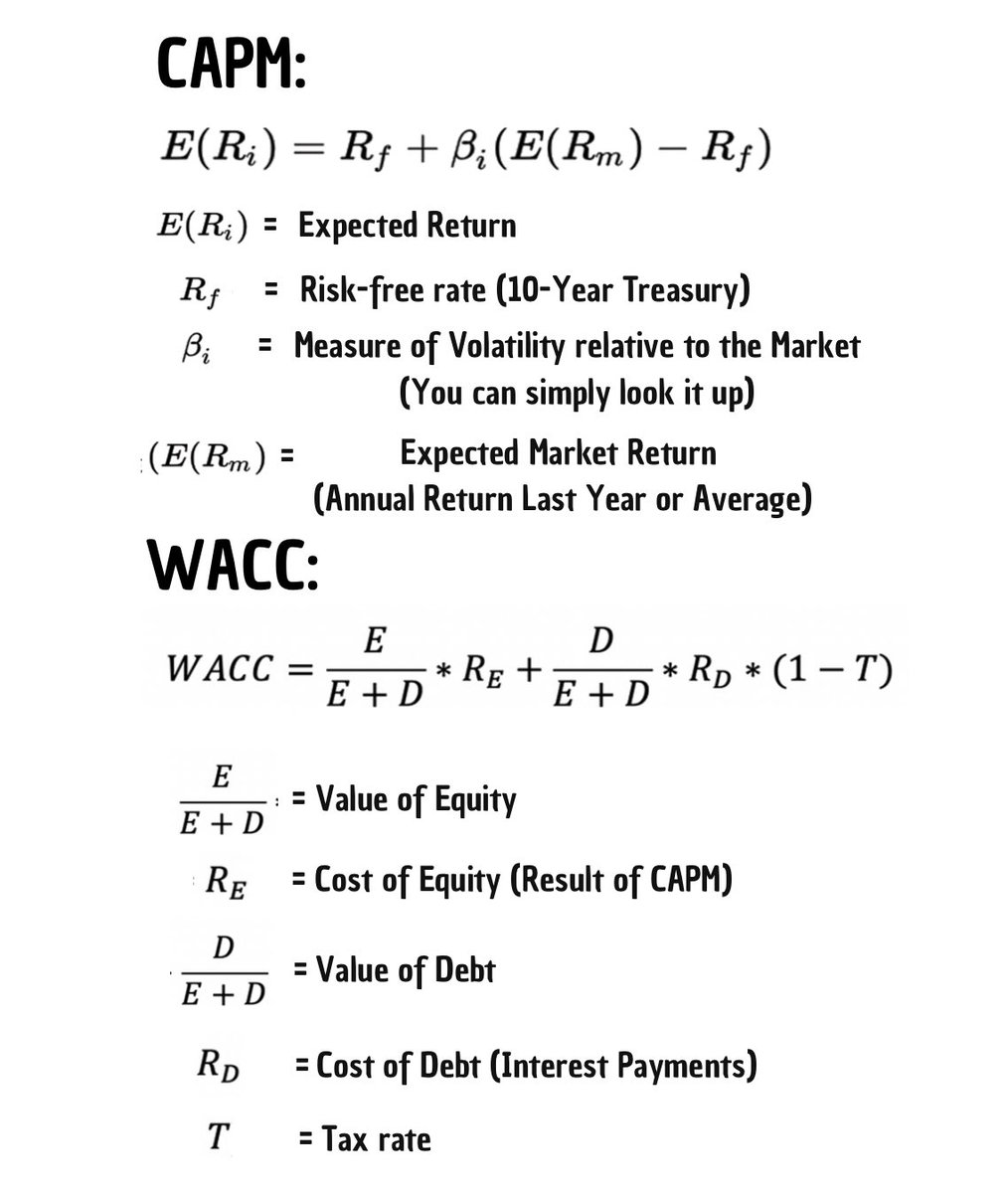

2.1 Weighted Average Cost of Capital

The WACC is more complicated, don’t be frustrated if you don’t fully understand it right away.

It measures how costly it is for a company to borrow money.

It focuses on both the company’s debt (bank loans, etc.) and equity (issued shares).

The WACC is more complicated, don’t be frustrated if you don’t fully understand it right away.

It measures how costly it is for a company to borrow money.

It focuses on both the company’s debt (bank loans, etc.) and equity (issued shares).

The cost of equity is calculated by a model called CAPM.

(Formula below)

If you have the cost of debt (interest payments) and cost of equity, you can calculate the WACC.

These formulas look more complicated than they are.

You can look all the numbers up and then fill them in.

(Formula below)

If you have the cost of debt (interest payments) and cost of equity, you can calculate the WACC.

These formulas look more complicated than they are.

You can look all the numbers up and then fill them in.

2.2 Long-Term Government Rate

What this means is simply to go with a “realistic” risk-free rate (10-Year gov. Bond).

Realistic means, based on historical rates and not too low.

Never use a rate below 6%.

Otherwise your valuation would be too sensitive to changes in rates.

What this means is simply to go with a “realistic” risk-free rate (10-Year gov. Bond).

Realistic means, based on historical rates and not too low.

Never use a rate below 6%.

Otherwise your valuation would be too sensitive to changes in rates.

A third, and the easiest option, is to go with your desired return.

If you aim for a 10% return, then use 10% as your interest rate.

Generally, the higher your discount rate, the higher your margin of safety.

At least from a valuation standpoint.

If you aim for a 10% return, then use 10% as your interest rate.

Generally, the higher your discount rate, the higher your margin of safety.

At least from a valuation standpoint.

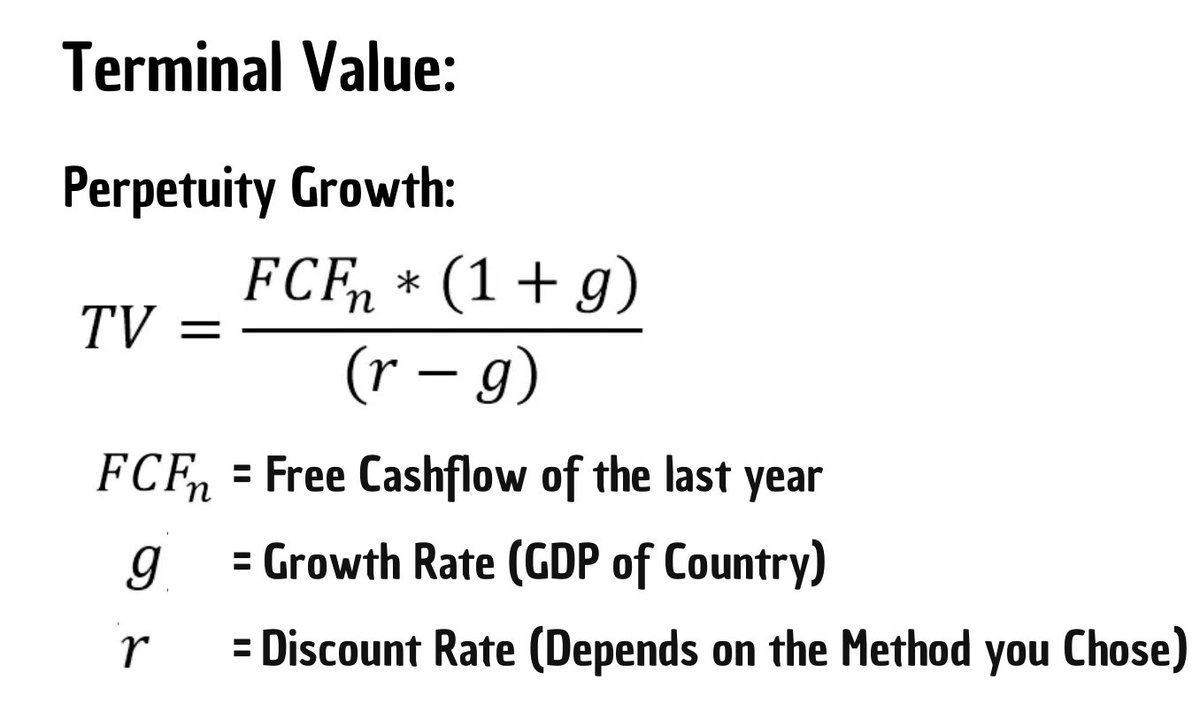

3. Terminal Value

The terminal value is the value of the business after your forecast period.

So let’s say you forecast 10 years of cash-flows (I wouldn’t go beyond that).

The company won’t just vanish after 10 years.

So to take that into account, you come up with the TV.

The terminal value is the value of the business after your forecast period.

So let’s say you forecast 10 years of cash-flows (I wouldn’t go beyond that).

The company won’t just vanish after 10 years.

So to take that into account, you come up with the TV.

Once again, there are two ways to determine the TV.

1. Perpetuity Growth

And

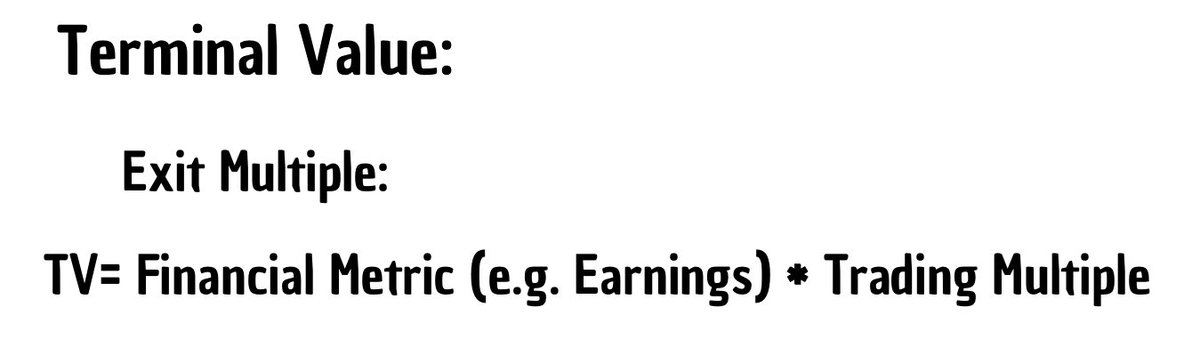

2. Exit Multiple

Before we get to them, remember to be conservative with your growth rates.

As you can imagine, the TV has a big impact on your DCF (After all, it’s growth to “infinity”).

1. Perpetuity Growth

And

2. Exit Multiple

Before we get to them, remember to be conservative with your growth rates.

As you can imagine, the TV has a big impact on your DCF (After all, it’s growth to “infinity”).

3.1 Perpetuity Growth

This method assumes that the cashflows will grow at a steady rate forever.

Accordingly low should be your estimated growth rate.

The standard is to go with the growth of the country’s GDP.

So if the country’s GDP grows by 2%, that’s your growth rate.

This method assumes that the cashflows will grow at a steady rate forever.

Accordingly low should be your estimated growth rate.

The standard is to go with the growth of the country’s GDP.

So if the country’s GDP grows by 2%, that’s your growth rate.

3.2 Exit Multiple

The second method is the simpler one once again.

You just assess a multiple for a financial metric, for example earnings.

You look at similar companies and then see for what multiple they trade.

The second method is the simpler one once again.

You just assess a multiple for a financial metric, for example earnings.

You look at similar companies and then see for what multiple they trade.

4. Discounting Cashflows and Terminal Value

Now you can start discounting cashflows and the TV.

The formula for the discount factor is down below.

The table below, is a Discount Factor Table.

Since the Discount factors don’t change, you can also just check them there.

Now you can start discounting cashflows and the TV.

The formula for the discount factor is down below.

The table below, is a Discount Factor Table.

Since the Discount factors don’t change, you can also just check them there.

Multiply the cashflows with the discount factor and you’re left with the discounted cashflows.

The Terminal Value gets discounted by multiplying it with the discount factor of the latest forecasted year.

For a 10-year period, multiply the TV with the discount factor of year 10.

The Terminal Value gets discounted by multiplying it with the discount factor of the latest forecasted year.

For a 10-year period, multiply the TV with the discount factor of year 10.

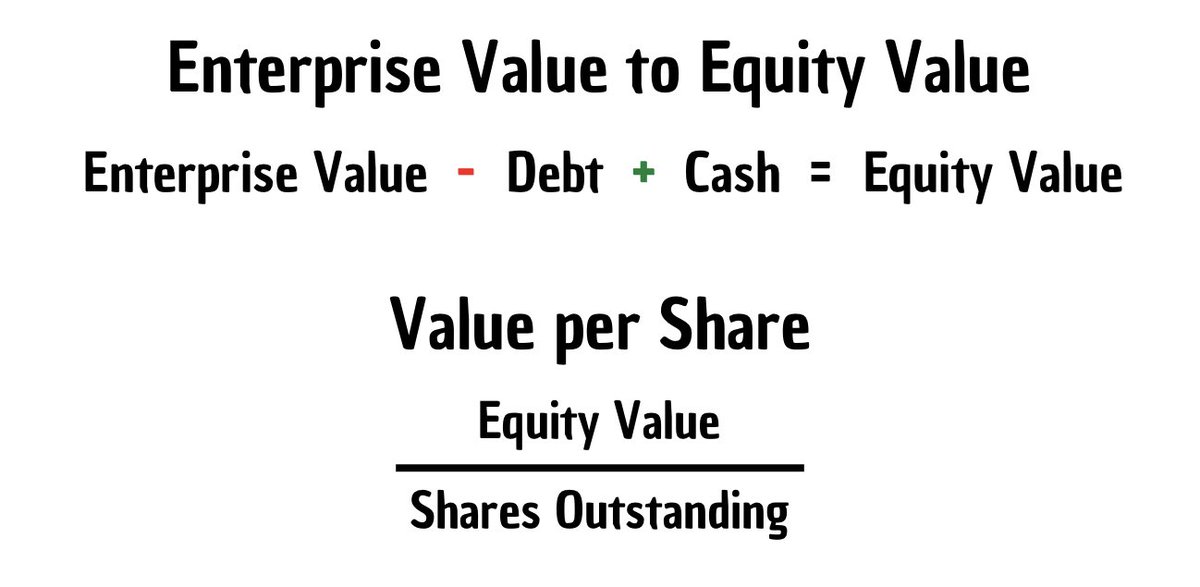

5. Equity Value

Now, we can add the discounted value of the cashflows and the TV.

The result is the Enterprise Value (EV).

EV is a more precise measure for the value of a company than market capitalization.

From the EV we can finally get to how much one share is worth today.

Now, we can add the discounted value of the cashflows and the TV.

The result is the Enterprise Value (EV).

EV is a more precise measure for the value of a company than market capitalization.

From the EV we can finally get to how much one share is worth today.

We do that by subtracting debt and adding cash (see formula below).

We get the Equity Value.

All that is then left to do, is to divide that Equity Value by the shares outstanding.

And voilà, you know how much a share of the company is worth today.

We get the Equity Value.

All that is then left to do, is to divide that Equity Value by the shares outstanding.

And voilà, you know how much a share of the company is worth today.

That’s it, you’re done!

I really hope you learned something and this was helpful.

If so, please Retweet and Like this Thread so that more people get to see it.

If it resonates well, I can post more of this type.

For more content on investing, follow me @MnkeDaniel

Cheers!

I really hope you learned something and this was helpful.

If so, please Retweet and Like this Thread so that more people get to see it.

If it resonates well, I can post more of this type.

For more content on investing, follow me @MnkeDaniel

Cheers!

جاري تحميل الاقتراحات...