An interesting read!

A thread on RHI Magnesita India Ltd and Refractory Industry in detail.

Why this sector? Refractory business is an indirect play on steel industry and capex cycle with less volatility

#refractories #RHIM #learningsatniveshaay

A thread on RHI Magnesita India Ltd and Refractory Industry in detail.

Why this sector? Refractory business is an indirect play on steel industry and capex cycle with less volatility

#refractories #RHIM #learningsatniveshaay

What led us to research this industry?

Revival in Indian Capex Cycle expected (Govt+Pvt) with favorable Govt. policies & reforms like PLI, NIP, Import Substitution, AMP, reduced corporate tax rate

Highlight of the #Budget2022 was also on reviving CAPEX cycle in India

Revival in Indian Capex Cycle expected (Govt+Pvt) with favorable Govt. policies & reforms like PLI, NIP, Import Substitution, AMP, reduced corporate tax rate

Highlight of the #Budget2022 was also on reviving CAPEX cycle in India

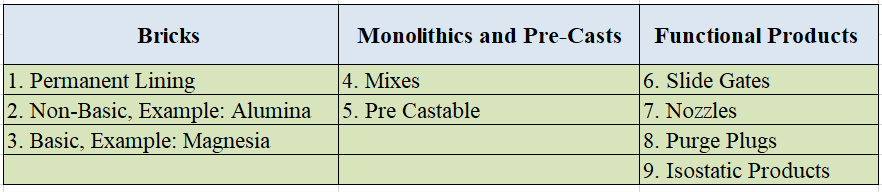

What are Refractories?

•Ceramic materials designed to withstand very high temps(>1200°C) without undergoing physical/ chemical changes while remaining in contact with molten slag/metal/gases.

•Critical product, yet forms 3% of COGS in steel mfg & < 1% in other applications.

•Ceramic materials designed to withstand very high temps(>1200°C) without undergoing physical/ chemical changes while remaining in contact with molten slag/metal/gases.

•Critical product, yet forms 3% of COGS in steel mfg & < 1% in other applications.

Refractories are characterized as Consumable(75%) or Investment Goods(25%) depending on the end user industry.

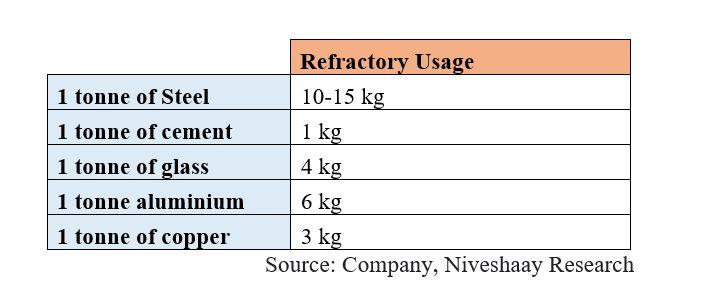

Application: 75% of refractory demand comes from Iron & Steel industry and remaining is from cement, glass, non ferrous & energy/environment/Chemicals.

#refractories

Application: 75% of refractory demand comes from Iron & Steel industry and remaining is from cement, glass, non ferrous & energy/environment/Chemicals.

#refractories

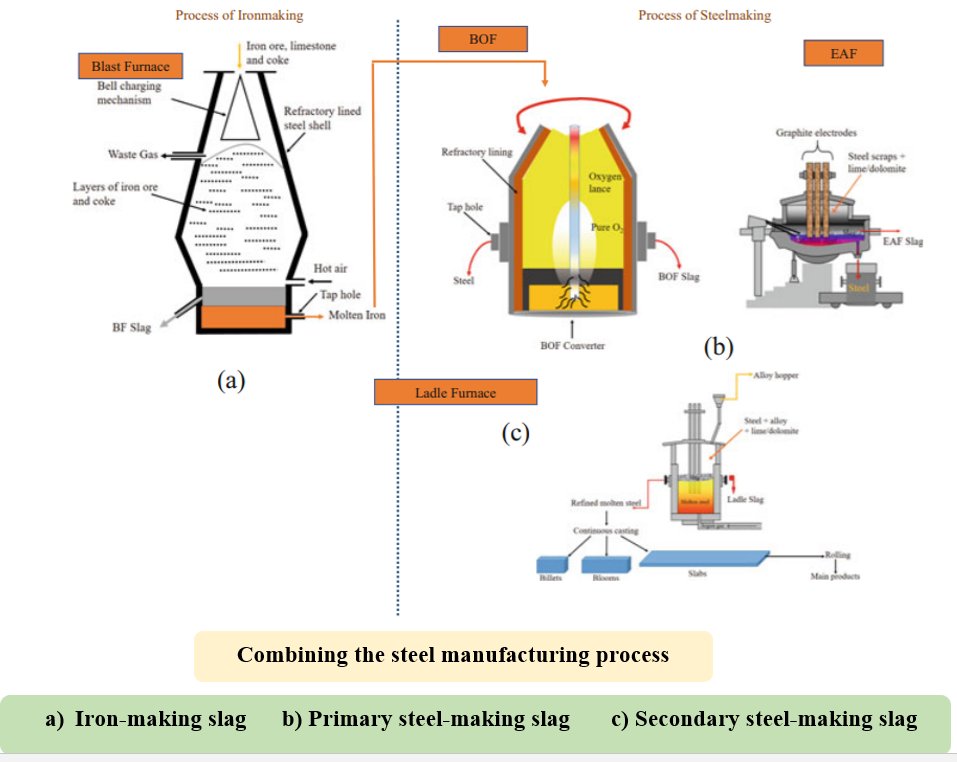

Methods of steel production:

i.Blast Oxygen Furnace (BOF)- Primary Steel Making

ii.Electric Arc Furnace (EAF)- Secondary Steel Making

i.Blast Oxygen Furnace (BOF)- Primary Steel Making

ii.Electric Arc Furnace (EAF)- Secondary Steel Making

Raw material used:

Brown Fused/White Fused Alumina

Magnesia

Silicon Carbide

Zirconia

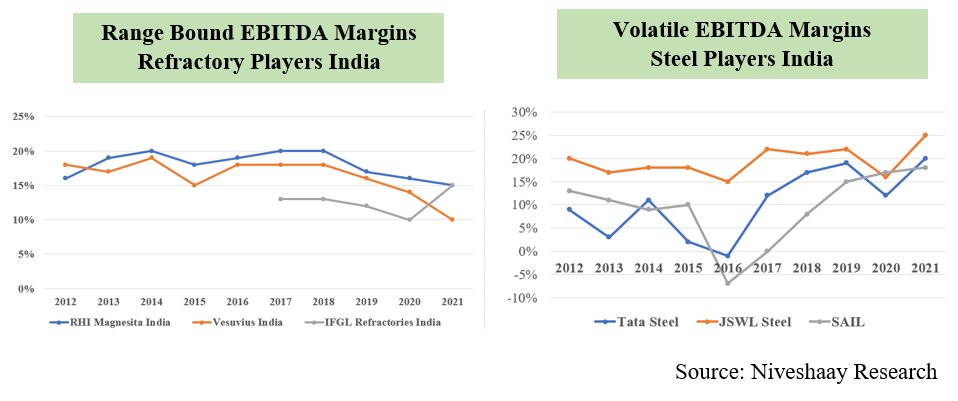

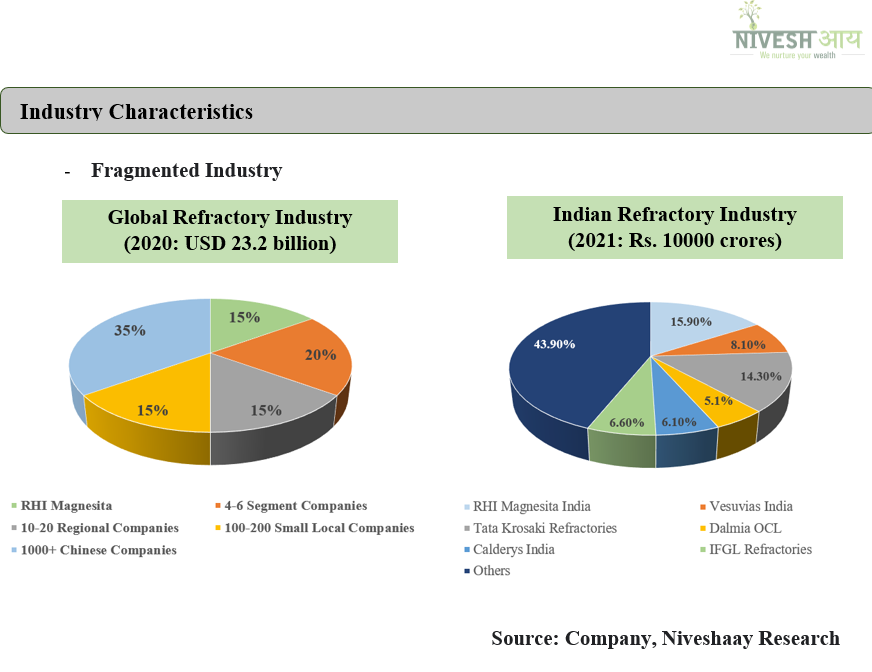

Understanding the Ref. Ind. in detail:

- Fragmented Ind.

- High Entry Barrier Bus.

- Consumable Product, less volatile over long term

- Consistent Growth in Ref. Bus. irresp. of steel cycle

Brown Fused/White Fused Alumina

Magnesia

Silicon Carbide

Zirconia

Understanding the Ref. Ind. in detail:

- Fragmented Ind.

- High Entry Barrier Bus.

- Consumable Product, less volatile over long term

- Consistent Growth in Ref. Bus. irresp. of steel cycle

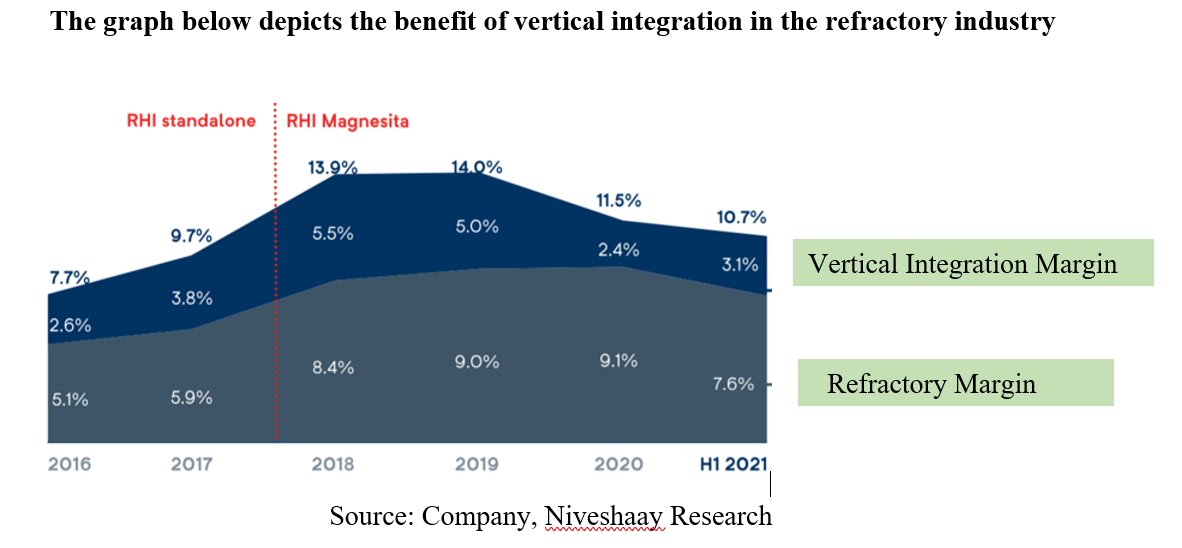

Supply Side Dynamics:

-Raw Material Security is challenging

-Benefit of Vertical Integration

-Recent Trends: Volatile Raw Material Prices,Shift to other countries for procuring raw material, Recycling of raw materials leading to cost savings

-Raw Material Security is challenging

-Benefit of Vertical Integration

-Recent Trends: Volatile Raw Material Prices,Shift to other countries for procuring raw material, Recycling of raw materials leading to cost savings

Why this ind. can do well, going forward

-Shortage of Raw Material can lead to consolidation in ind.

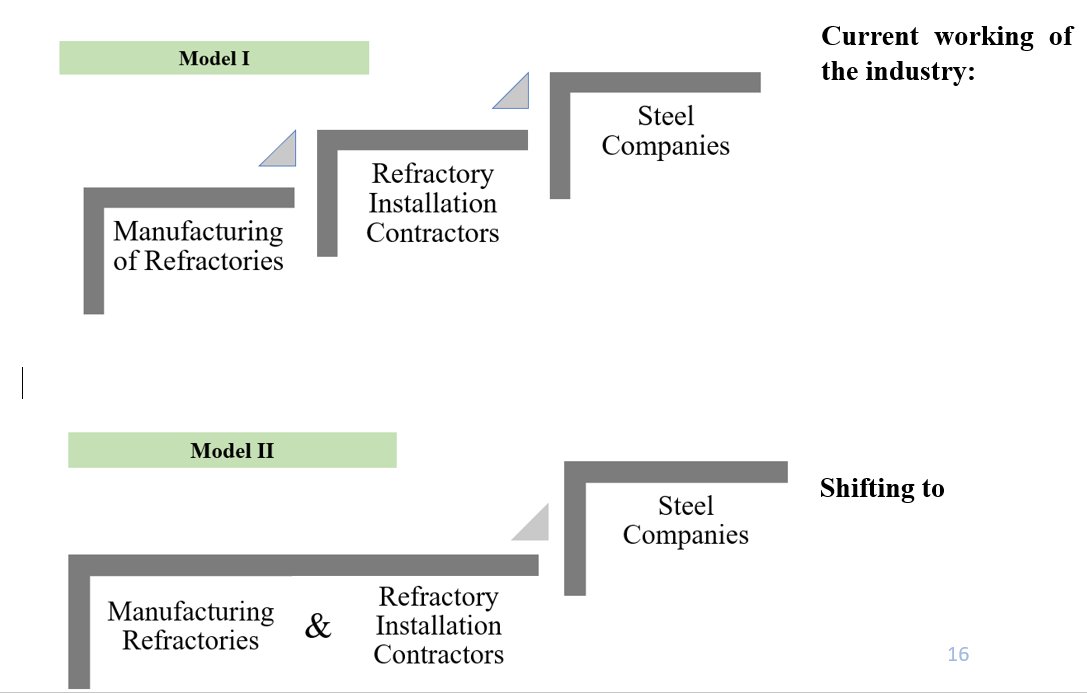

-Ind. is moving towards TRM services or complete business sol model

-Steel Prod. expected to remain high

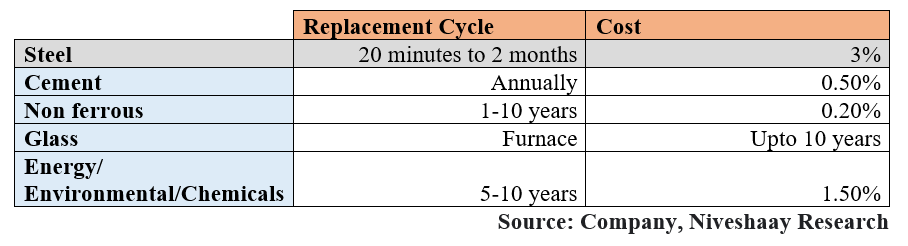

Refractory maintenance practice is imp. also leads to high vol consumption

-Shortage of Raw Material can lead to consolidation in ind.

-Ind. is moving towards TRM services or complete business sol model

-Steel Prod. expected to remain high

Refractory maintenance practice is imp. also leads to high vol consumption

Why RHI Magnesita India?

-Market Leader ~15.9% market share

-Direct beneficiary of expected consolidation

-TRM

-Superior Margins than peers & comparatively lower on cost curve

-Better capacity utilisation than competitors

-Better Product Mix

-CAPEX Plan (400 Cr. for next 3 yrs)

-Market Leader ~15.9% market share

-Direct beneficiary of expected consolidation

-TRM

-Superior Margins than peers & comparatively lower on cost curve

-Better capacity utilisation than competitors

-Better Product Mix

-CAPEX Plan (400 Cr. for next 3 yrs)

About company

- Incorporated in 2021 with merger of 3 RHI entities

Orient Refractories Ltd., RHI Clasil & RHI India Pvt Ltd.

Total installed capacity : 128000 tons PA

- Geography Wise Revenue: India 75% Exports 25%

- Key Risks:

1.Volatility in RM Prices

2.Downturn in Steel Ind

- Incorporated in 2021 with merger of 3 RHI entities

Orient Refractories Ltd., RHI Clasil & RHI India Pvt Ltd.

Total installed capacity : 128000 tons PA

- Geography Wise Revenue: India 75% Exports 25%

- Key Risks:

1.Volatility in RM Prices

2.Downturn in Steel Ind

Competitive scenario:

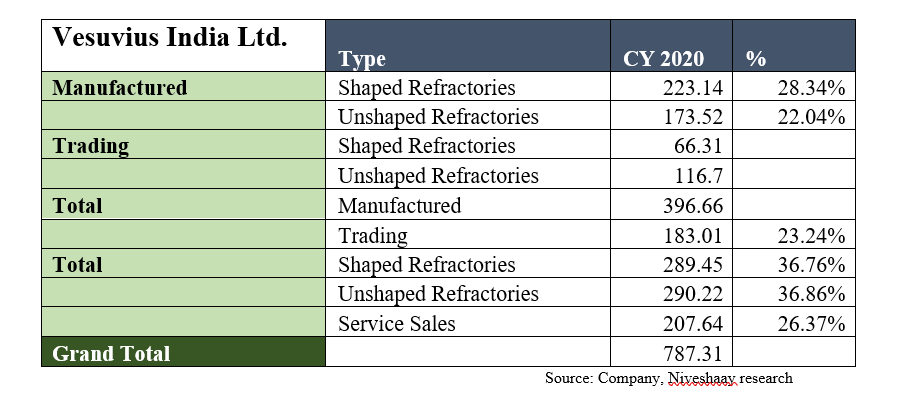

1. Vesuvius India Ltd.: RM import dependent, lost market share in last 5 yrs, installedd capacity - 275k tons

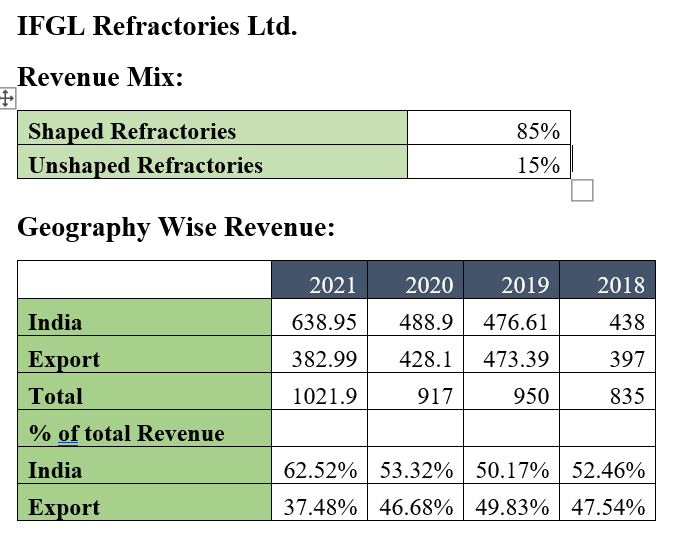

2. IFGL Ref. Ltd.: RM import dependent, Product: specialized flow control ref., Installed capacity 27Lakh pieces of shaped & 52K tons of unshaped

1. Vesuvius India Ltd.: RM import dependent, lost market share in last 5 yrs, installedd capacity - 275k tons

2. IFGL Ref. Ltd.: RM import dependent, Product: specialized flow control ref., Installed capacity 27Lakh pieces of shaped & 52K tons of unshaped

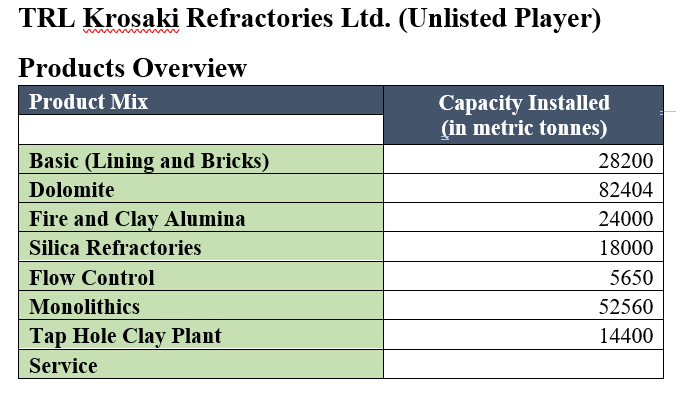

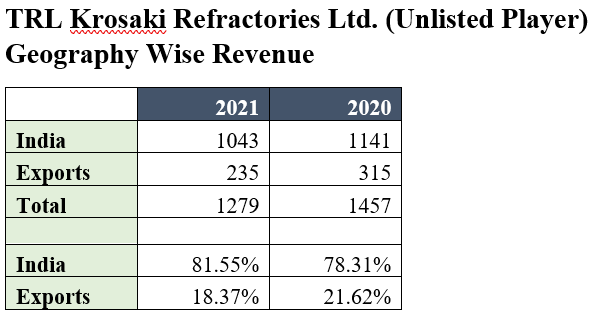

3. TRL Krosaki Refractories Ltd. (Unlisted Player)

4. Calderys India (Unlisted Player): more into unshaped refractories, RM import dependent, 40-45% of the total revenue comes from iron and steel industry.

4. Calderys India (Unlisted Player): more into unshaped refractories, RM import dependent, 40-45% of the total revenue comes from iron and steel industry.

Loading suggestions...