High option premium before events like budget create illusion that we got high margin of safety.

IV crush bhi aata hai, theta decay bhi hota hai..lekin realise nahi hota due to delta moves.

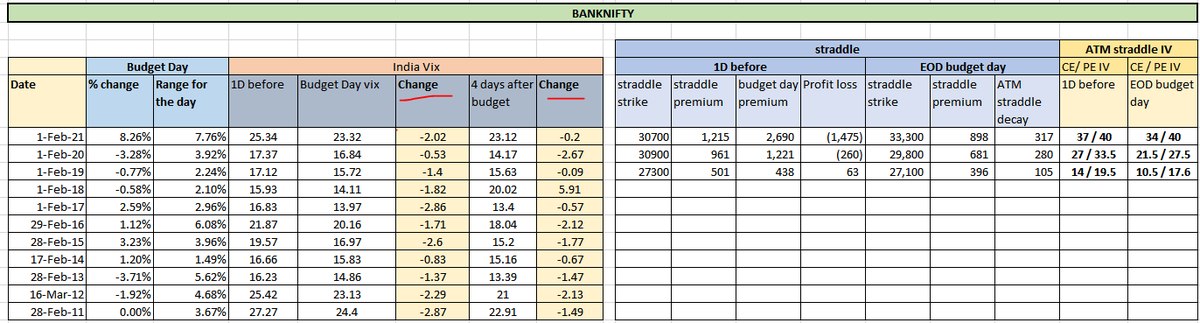

One more data points of how india vix and straddles IV behaved in past.

[1/n]

IV crush bhi aata hai, theta decay bhi hota hai..lekin realise nahi hota due to delta moves.

One more data points of how india vix and straddles IV behaved in past.

[1/n]

for simple calculation have compared straddles 1day before budget and at EOD of budget day

1⃣On an average vix falls by 2% on budget day and buy another 2% in next 4 days

2⃣in last 2 years realised decay on straddle was zero[without adjustment]

[2/n]

1⃣On an average vix falls by 2% on budget day and buy another 2% in next 4 days

2⃣in last 2 years realised decay on straddle was zero[without adjustment]

[2/n]

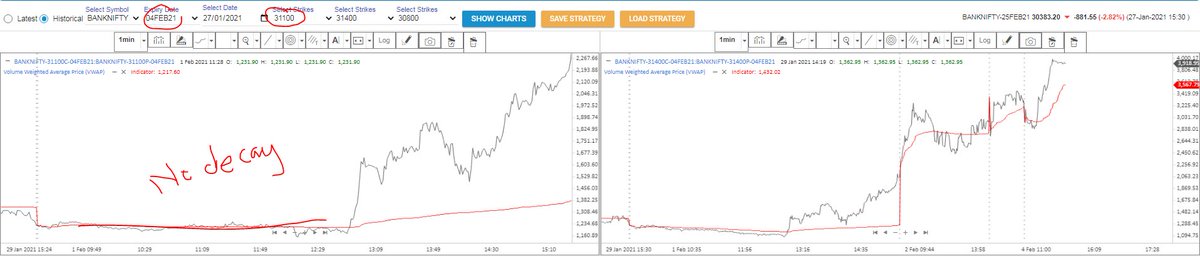

3⃣new traders faces two issues here [trending moves and mtm swing due to intraday volatility-which forces you to do wrong adjust.

Few tips

1⃣ Reduce trading size drastically

2⃣ wait for event to get over - see on straddle / strangle charts are we getting any decay?

[3/n]

Few tips

1⃣ Reduce trading size drastically

2⃣ wait for event to get over - see on straddle / strangle charts are we getting any decay?

[3/n]

3⃣ can move to monthly expiry so can move to farther strikes/higher prem on straddles[weekly has 1400 vs 2250 in monthly]

4⃣ can do strangles outside major support and resistance level and use rolling as adj.

5⃣ sell slight higher premium on call side [if u matching prem]

[4/n]

4⃣ can do strangles outside major support and resistance level and use rolling as adj.

5⃣ sell slight higher premium on call side [if u matching prem]

[4/n]

6⃣ use risk defined strategies like ironfly or strategies like double ratios

7⃣ define max risk for day & do straddle/strangle with 10-15% stop loss on combined premiums

8⃣ do any of above but never lose more then 1-2% of capital on such day

"Woh bulati Hai. Magar.......

[5/5]

7⃣ define max risk for day & do straddle/strangle with 10-15% stop loss on combined premiums

8⃣ do any of above but never lose more then 1-2% of capital on such day

"Woh bulati Hai. Magar.......

[5/5]

Loading suggestions...